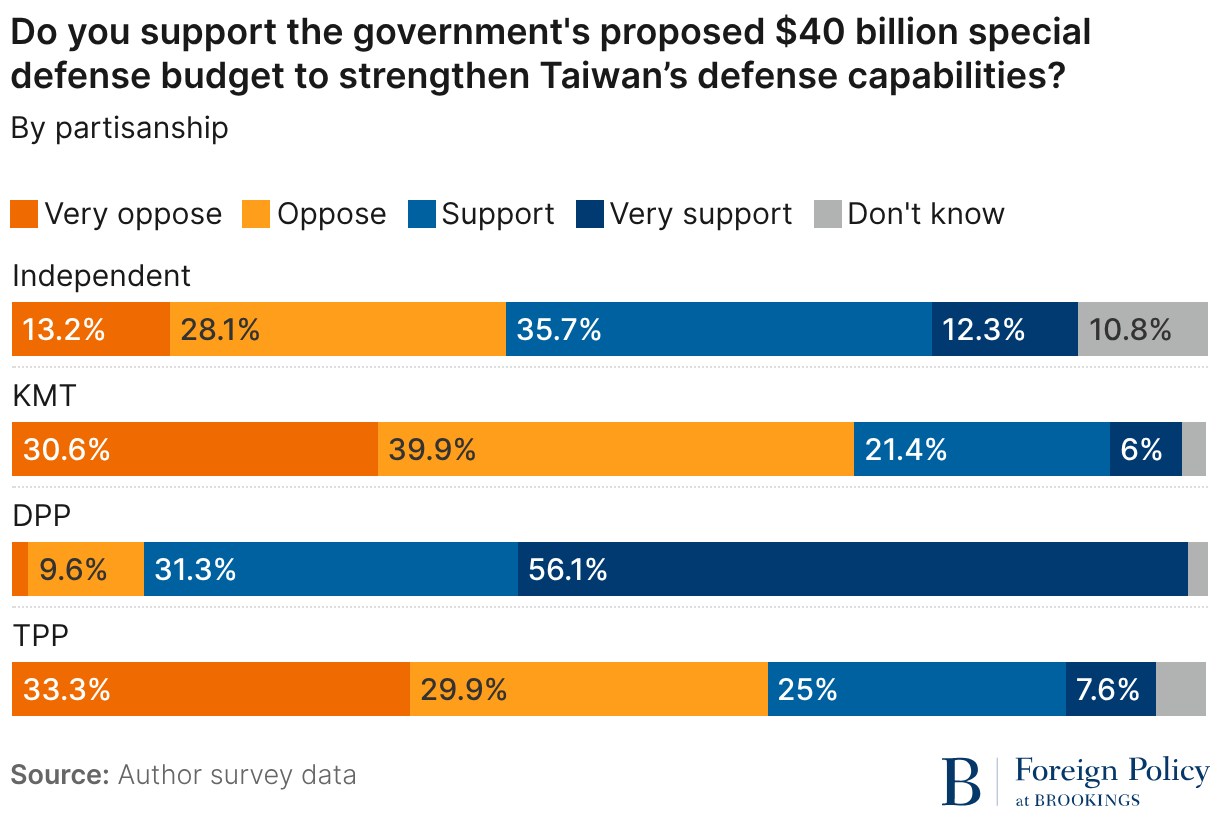

Taiwanese opinion is sharply divided on President Lai Ching-te’s proposed $40 billion defense budget, with 54% overall support but 87% of DPP voters backing it versus only 27.4% of KMT voters. The survey also finds only 24% of Taiwanese view the U.S. as a trustworthy ally, while roughly 40% think Washington would be unlikely to aid Taiwan in a conflict and concern is widespread that U.S. involvement in the Middle East could weaken support for Taiwan. Attitudes toward Trump are mostly negative, and trust in the U.S. has declined over Trump’s second term despite some stabilization in the latest survey.

The equity implication is not a clean pro-defense or anti-China trade; it is a referendum on KMT credibility as a governing alternative. The more important signal is that the party’s base is internally split on the core national-security narrative, which raises the odds that KMT leadership will oscillate between hardline rhetoric and tactical moderation. That makes KMT policy execution noisier, and any attempt to capitalize on cross-Strait fatigue risks being diluted by intra-party factionalism rather than by DPP strength.

For markets, the second-order effect is that Taiwan’s defense-industrial and industrial-policy beneficiaries may still gain even when headline budgets get watered down. Investors should focus on programs that survive legislative compromise: munitions, drones, command-and-control, and maintenance/upgrade cycles rather than platform-heavy, long-lead procurements. The real tailwind is not budget quantum but the normalization of multi-year replenishment, which is more durable for domestic industrial capacity and select U.S. export suppliers than a single one-off spending vote.

The more interesting contrarian read is that skepticism toward Washington is now broad but not yet fully translated into pro-China policy preferences. That means the market is likely underpricing hedging behavior: more willingness to diversify supply chains, hold higher inventory, and pay for contingency logistics across Taiwan corporates, but without a full strategic rerating away from U.S.-linked assets. The key risk is a deterioration in perceived U.S. reliability over the next 6-12 months, which would matter more than the defense-budget headline because it would directly alter capital allocation, procurement timing, and alliance-risk premia.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.05

Ticker Sentiment