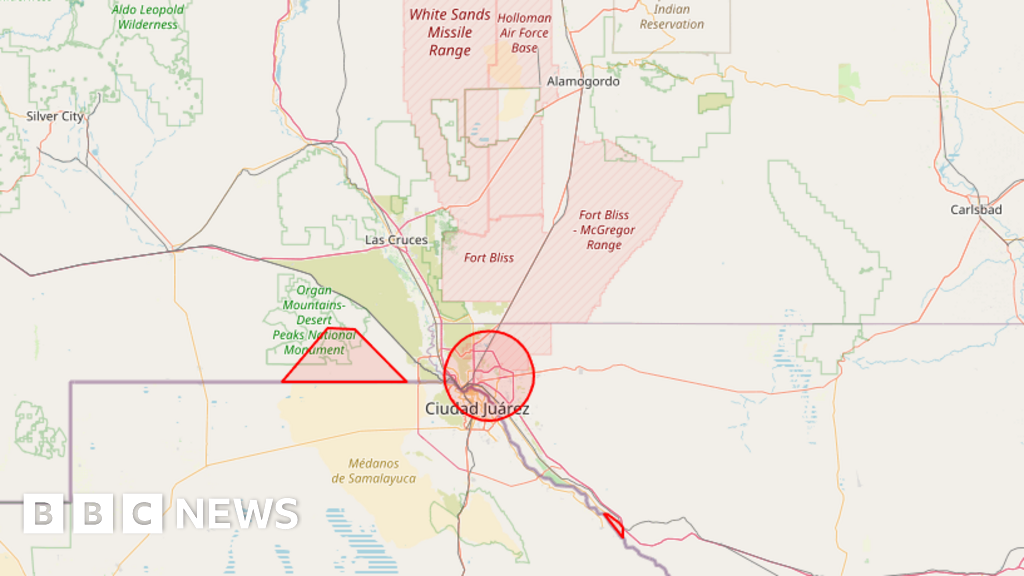

The FAA has closed airspace in a 10-mile radius around El Paso for 10 days — from Tuesday 11:30pm local (Wednesday 0630 GMT) through 20 February 11:30pm local (21 February 0630 GMT) — grounding all commercial, cargo and general aviation flights; the agency cited "special security reasons" while local authorities say they received no advance notice. The restriction covers parts of southern New Mexico (including San Teresa) and lies adjacent to Ciudad Juárez, Fort Bliss and White Sands Missile Range, creating short-term travel and cargo disruption risks and localized supply-chain effects; absent further escalation or broader regional implications, the event is unlikely to move broad financial markets.

Market structure: A 10-day, 10-mile airspace shutdown centered on El Paso disproportionately hurts regional passenger and cargo air operators serving El Paso (expect a near-term 5–10% local capacity shock) and benefits intermodal ground/freight carriers that can absorb diverted traffic. Expect short-lived upward pressure on regional trucking and rail volumes (UNP, CSX, KSU/CPKC) and marginal upside for FedEx/UPS as last-mile/cargo reroutes; macro asset moves should be small — expect a 3–10bp flattener in front-end Treasuries and a fleeting USD bid if perceived as security/geo-risk. Risk assessment: Tail risks include escalation into adjacent military activity or extended/rolling airspace restrictions that would move from a 10-day operational disruption to a multi-month logistics reallocation; probability low (<10%) but impact high for cross-border manufacturing in Ciudad Juárez (auto/medical). Immediate window (days): cancelled flights, higher short-term cargo premiums; short-term (weeks): routing costs +1–4% for affected shippers; long-term (quarters): capital reallocation to road/rail if closures repeat. Catalysts to watch: FAA/DoD briefings within 72h, Mexico border policy, and corporate 10-Q inventory/OTD revisions. Trade implications: Tactical longs — select rail/ground logistics (UNP, CSX) and parcel shippers (FDX, UPS) sized 0.5–2% each for 2–6 week re-rating as volumes reroute; tactical shorts — regional/short-haul airline exposure (AAL, LUV, SAVE) via 2–4 week puts given revenue disruption and capacity drag. Use 2–6 week call spreads on FDX/UPS to cap cost and 2–4 week ATM puts on AAL/LUV for directional downside; enter within 48–72 hours and trim into any FAA clarification or by Feb 21. Contrarian angles: The market may over-penalize big national carriers while underpricing localized manufacturing risk — small-cap auto suppliers and Mexico-adjacent subcontractors could see 5–15% earnings volatility if JIT lines are interrupted; historically, temporary airspace closures mean-revert in 3–10 days, so option premium decays quickly — favor short-dated structures and size positions to capture a 3–6% mispricing rather than multi-week outright directional exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25