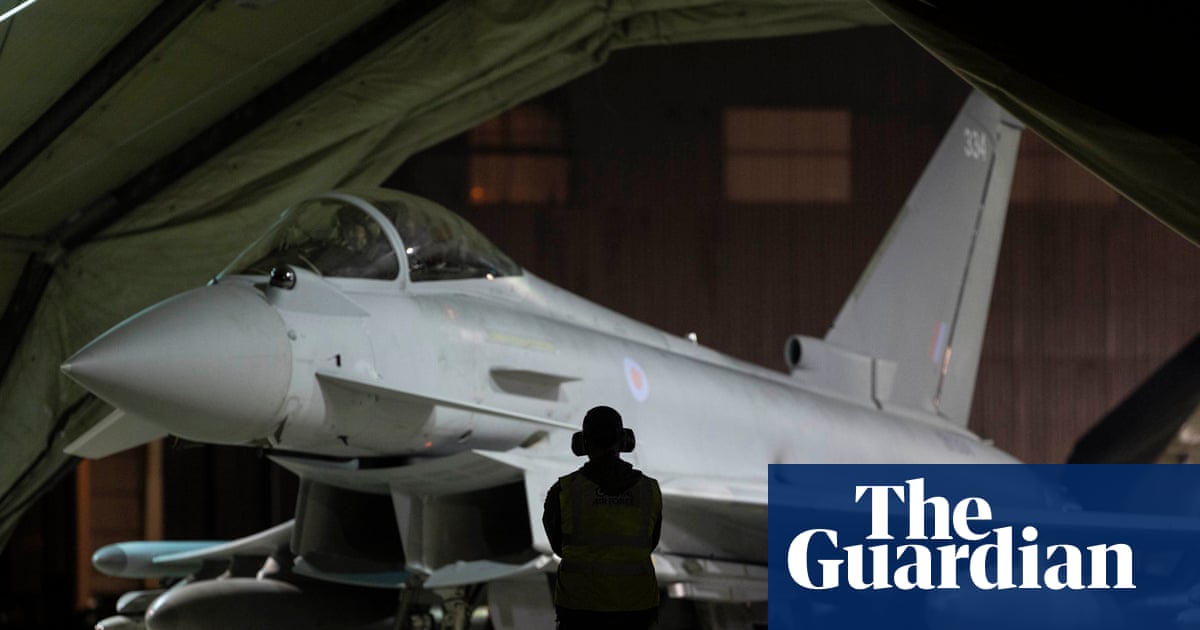

Britain is preparing to deploy RAF Typhoons from Qatar to patrol the Strait of Hormuz as part of a multinational mission aimed at keeping the waterway open after the Iran war ends. The UK is also considering mine-hunting drones and specialist divers, but no final decision has been made on a warship deployment. The plan underscores heightened geopolitical risk around a critical energy and shipping route, with the mission’s scope and US participation still unclear.

The market should read this less as an imminent military escalation and more as an attempt to reprice the probability distribution for post-war shipping security. The first-order beneficiary is not defense primes in the abstract, but any asset whose cash flows are levered to a faster normalization of Gulf insurance premia, convoy economics, and port throughput; the second-order loser is the floating storage / tanker stack that benefits from dislocation and rerouting. If the plan evolves into a credible multinational escort regime, the trade is mechanically bearish for volatility in freight rates and bullish for regional logistics capacity utilization.

The more interesting angle is that the UK is signaling airpower-heavy reassurance because naval capacity is constrained; that subtly shifts the marginal utility of allied basing, maintenance, munitions, and ISR rather than hull count. That favors aerospace supply chains, counter-drone systems, and mission support contractors over pure surface-combat shipbuilders. It also suggests the UK is trying to preserve optionality with minimal deployed capital, which reduces the odds of a large fiscal overhang but increases dependence on high-tempo readiness and spare parts—an area where bottlenecks can create short-lived pricing power.

For energy, the key second-order effect is not a sustained supply shock, but the removal of the geopolitical risk premium if the Strait can be protected after a ceasefire. In that scenario Brent can retrace 5-10% quickly even if fundamentals stay tight, because positioning is likely long protection and underweight volatility decay. The tail risk is the opposite: if mine-clearing is delayed or the mission appears unserious, tanker insurance and prompt crude diffs can gap wider within days, while the broader impact on equities stays contained unless it spills into a renewed blockade narrative.

The contrarian view is that the headline is directionally stabilizing and therefore mildly bearish for many of the “war trade” winners. Markets may be overestimating how much incremental naval presence matters once the shooting stops, while underestimating how fast freight and insurance normalize when diplomacy gets a credible enforcement backstop. The cleaner trade is to fade residual panic premium rather than chase defense beta outright.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.10

Ticker Sentiment