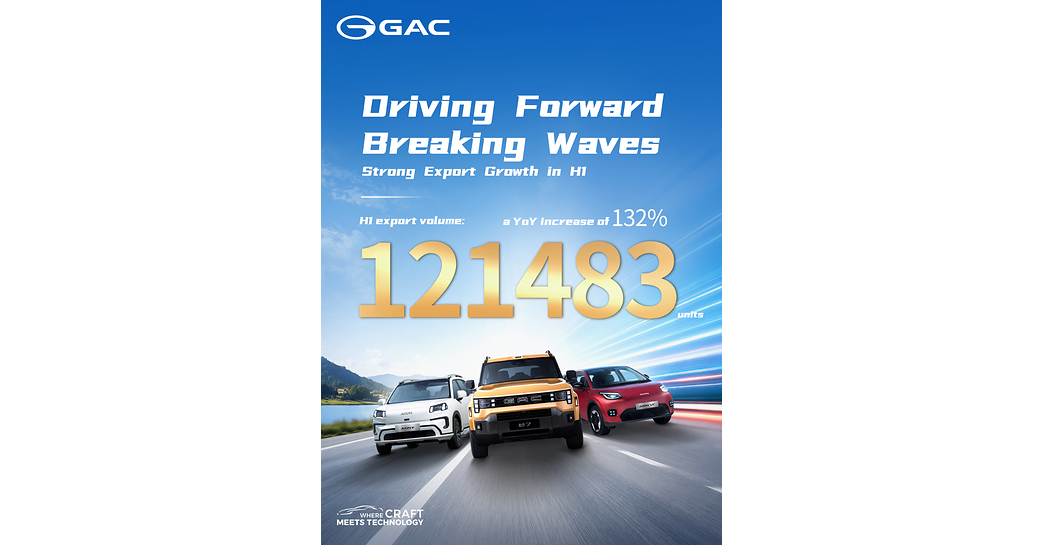

GAC reportó un salto fuerte en el 1S2026: las exportaciones totales llegaron a 121,483 unidades, casi igualando el volumen anual previo, con +132% interanual. En América, destacó Brasil con ventas de junio +1,129% m/m y +24% a/a, mientras que Colombia subió +804% m/m y +21% a/a. En Asia-Pacífico, Hong Kong superó 11% de cuota acumulada (ene-may) y Singapur creció +77% m/m y +30% a/a, reflejando tracción multi-país en BEVs.

The key read-through is not the volume print itself, but that this is evidence Chinese OEMs are using emerging markets as a pressure valve for excess EV capacity. That tends to help firms with the best cost curve and weakest domestic absorption first, while pressuring local incumbents in entry-level BEV, taxi, and fleet channels across Latin America and Southeast Asia. The more important second-order effect is channel economics: when growth is this fast, the market should question whether it is end-demand or dealer stocking, because the latter boosts reported sales without durable margin support. For investors, the main bull case is fixed-cost leverage if export mix is still underpenetrated: overseas units can matter more to earnings than to revenue if they sit on higher ASPs and better utilization at the factory. But that only works if logistics, warranty, and working-capital drag do not absorb the spread; in many overseas rollouts, receivables and inventory build before cash conversion turns. The near-term catalyst is the next results release: look for gross margin, DSO, and operating cash flow rather than top-line growth. Contrarian view: the market may be over-reading a low-base growth story as a structural share-grab. Emerging-market EV demand is still financing-sensitive and policy-fragile, so a tightening of import duties, FX pressure, or fleet subsidy rollback could reverse momentum within 1-3 quarters. If GAC can sustain overseas unit growth while improving cash conversion and service-part attach rates over 6-18 months, the signal is real; if not, this is likely a cyclical inventory push that fades once the initial channel fill is complete.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.40