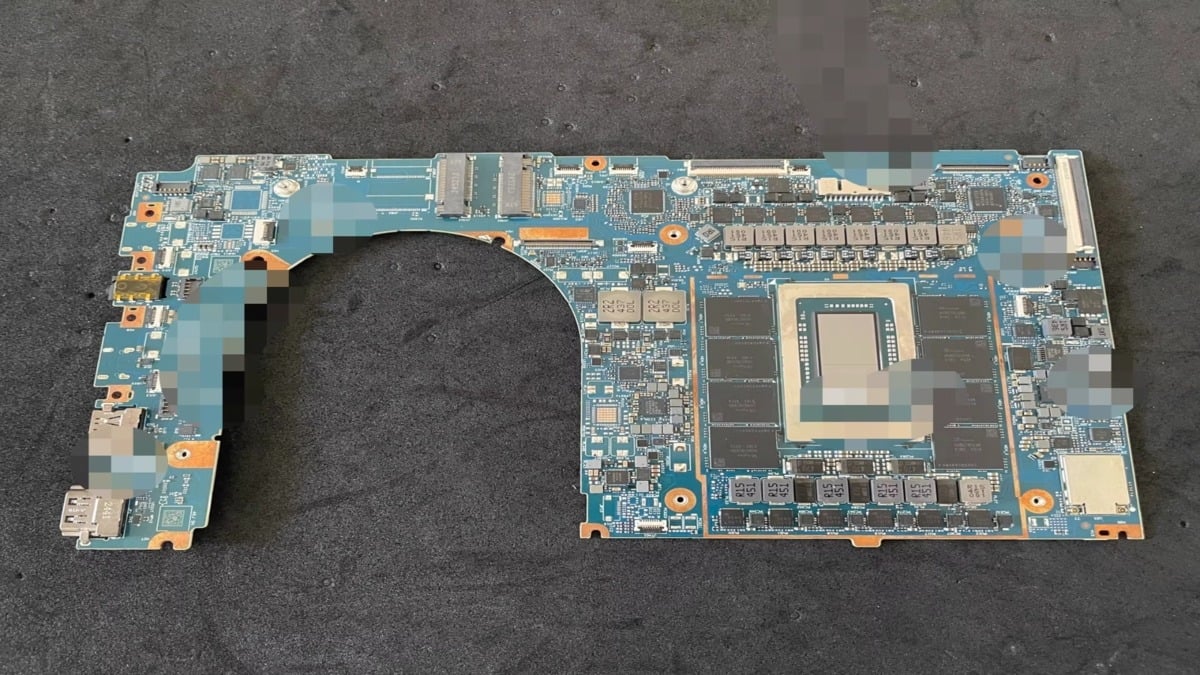

An engineering board leak suggests NVIDIA's N1 SoC is in final validation ahead of Computex 2026, featuring up to 6,144 CUDA cores, 20 Arm cores (Cortex-X925 + Cortex-A725 in two clusters), a 256-bit memory interface supporting 128GB LPDDR5X-8533 (~273 GB/s), and a pictured price of 9,999 RMB (~$1,400) for the 128GB configuration. The N1/N1X is a MediaTek CPU + NVIDIA Blackwell GPU 'superchip' using GB10 silicon fused via TSMC CoWoS and is positioned as an AI-first WoA solution; gaming and legacy x86 performance will depend on Microsoft's Prism AVX/AVX2 emulation and may face kernel anti-cheat and optimization hurdles. If confirmed at Computex, the chips could shift expectations for high-end Windows-on-Arm devices and exert pricing/competitive pressure in workstations, although high-memory SKUs will likely remain premium.

This product ripple is less about a single device and more about reordering margin pools across multiple layers: IP royalty capture (CPU/GPU firmware and middleware), advanced packaging throughput, and high-bandwidth memory SKU mix. Expect near-term ASP expansion for devices that prioritize integrated high-capacity LPDDR stacks, which can lift supplier revenue disproportionately even if unit demand grows modestly. From a competitive angle, incumbents that rely on raw x86 performance will face a two-front pressure: software translation and specialized on-device AI acceleration that shifts workload economics away from raw CPU cycles. That makes middleware (OS translation, anti-cheat/kernel adapters) and specialized silicon packaging winners — they control the go/no-go gates for OEM adoption and can extract rents via integration services or prioritized capacity. Key tail risks are software maturity and thermal/battery trade-offs; if emulation and kernel interactions remain brittle, OEM acceptance and enterprise procurement stalls. Operationally, the highest-leverage bottleneck is advanced packaging capacity and memory supply for premium SKUs — either can introduce 6–12 month delivery slippage that materially reduces upside from an otherwise strong product unveiling. For positioning, the asymmetric payoff is in optionality around adoption rather than a pure hardware call: capture upside from a successful early ramp while limiting exposure to the two main reversal triggers (software friction and packaging/memory supply). That argues for short-dated directional optionality into the reveal window, paired with longer-duration exposure to foundry/packaging beneficiaries if yields and OEM designs validate.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.18

Ticker Sentiment