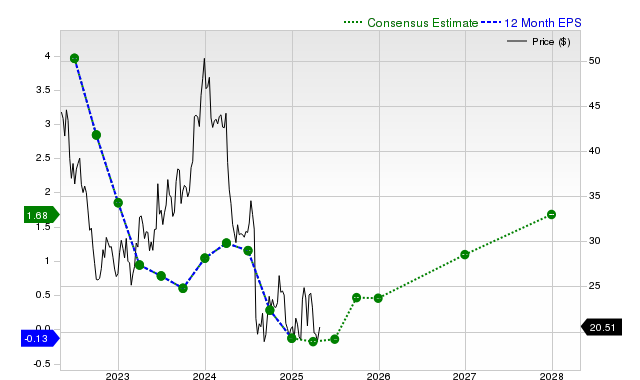

Intel (INTC) shares have seen a significant 16.3% gain over the past month, outperforming both the S&P 500 and the broader semiconductor industry. However, despite recent quarterly revenue and EPS beats, the company faces notable downward revisions in consensus earnings estimates across the current and next fiscal years, with current quarter EPS estimates declining 9.2% in the last 30 days. This negative trend in analyst sentiment, coupled with a Zacks Value Style Score of 'D' indicating a premium valuation relative to peers, has led Zacks to assign Intel a Rank #4 (Sell), suggesting potential near-term underperformance.

Despite Intel's (INTC) significant stock price appreciation of 16.3% over the past month, which outpaced both the S&P 500 and the semiconductor sector, a deeper look at its fundamentals reveals considerable headwinds. Analyst consensus earnings estimates are trending downwards, having been revised lower by 9.2% for the current quarter and by 4.0% for the current fiscal year within the last 30 days. This negative sentiment is underpinned by projections of a 7.5% year-over-year revenue decline for the current quarter and a 4.3% decline for the full fiscal year. While the company has a recent history of beating consensus estimates, notably with a 1200% EPS surprise in the last reported quarter, the persistent negative revisions have resulted in a Zacks Rank of #4 (Sell). Furthermore, the stock's valuation appears stretched, as indicated by a Zacks Value Style Score of 'D', suggesting it is trading at a premium to its peers despite the deteriorating near-term outlook.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.30

Ticker Sentiment