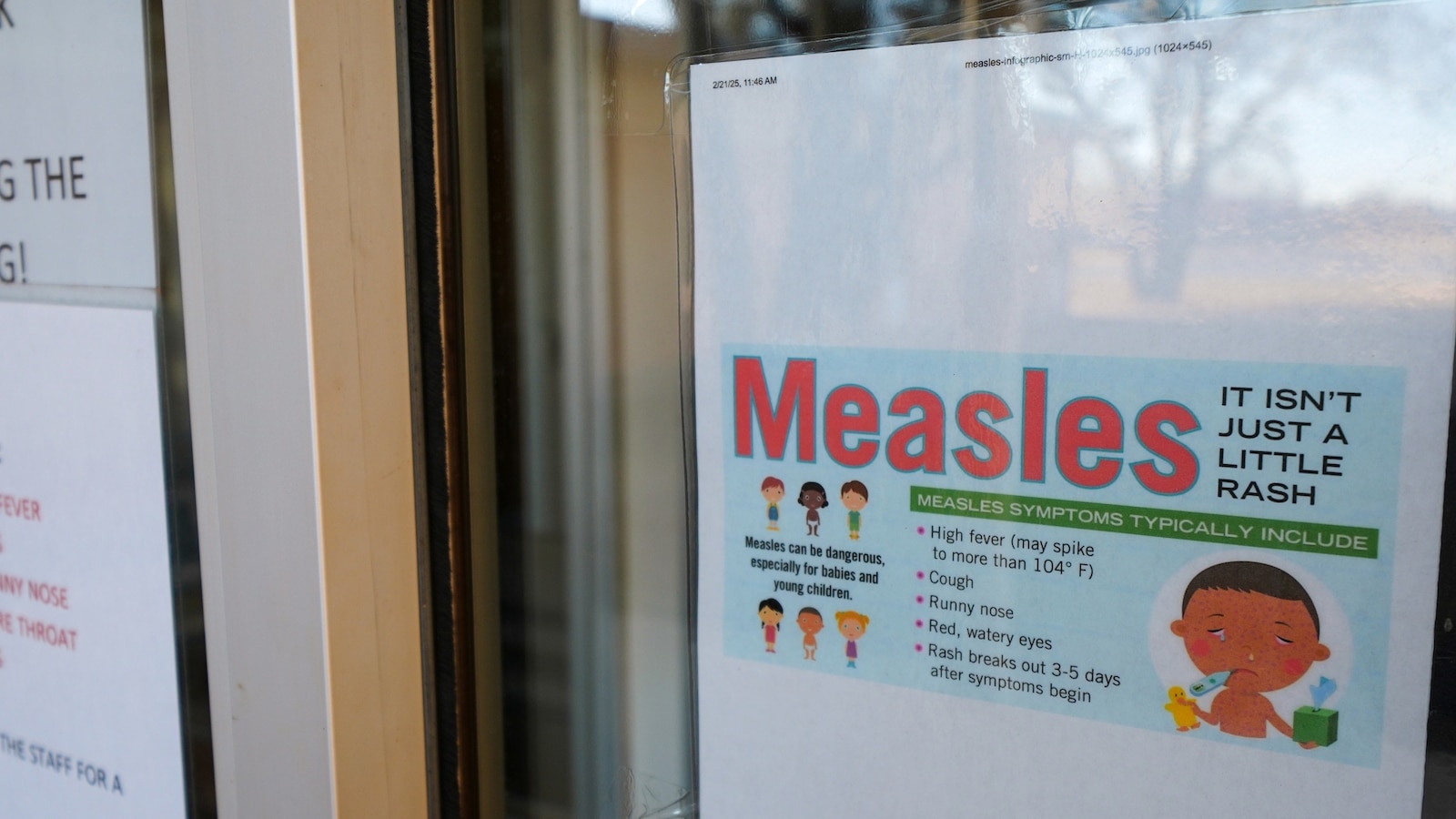

South Carolina reported 124 new measles cases since last Friday, bringing the local outbreak total to 434 with over 400 people in quarantine and most cases concentrated in Spartanburg County. The report underscores a broader U.S. resurgence—last year saw 2,144 cases (the highest since 1992) and nearly 50 outbreaks—with three deaths in 2025; CDC data show 93% of 2025 cases were among unvaccinated or vaccination-unknown individuals and kindergarten MMR coverage fell to 92.5% in 2024–25 from 95.2 in 2019–20. The CDC recommends two MMR doses (93% efficacy for one dose, 97% for two), signaling potential for continued public-health interventions, localized disruptions and possible demand for vaccination and containment resources.

Market structure: Winners are vaccine producers and downstream distributors — principally Merck (MRK) as the primary U.S. MMR supplier, Pfizer (PFE)/Sanofi (SNY) if they pivot supply, and retail clinic operators CVS (CVS) and Walgreens (WBA) that capture administration revenue. Losers are localized consumer-facing businesses (regional leisure, daycare operators) and insurers facing higher short-term claim frequency; expect low-to-mid single-digit percentage revenue tailwinds for vaccine makers if procurement ramps over 3–12 months. Competitive dynamics: if Merck faces capacity constraints it gains pricing power and order visibility from state contracts; new entrants face regulatory/cold-chain barriers so share shifts will be sticky over quarters, not days. Risk assessment: Tail risks include a significant supply-chain disruption (vial/ASL shortages) or litigation from adverse events, each capable of moving MRK ±10–20% intrayear. Immediate (days) impacts are localized market sentiment and clinic volumes; short-term (weeks–months) risks center on state mandates and emergency funding, long-term (quarters–years) is public-health policy reversal or entrenched anti-vax pockets reducing addressable market. Hidden dependencies: demand is driven by state K–12 mandate changes and school-exemption policies; a single large state procurement (>500k doses) materially changes revenue cadence for suppliers. Trade implications: Tactical long on MRK (1–2% portfolio weight) for 3–12 months to capture procurement/order visibility, paired with a 6-month call spread to limit downside. Overweight CVS/WBA (0.5–1% each) to play clinic administration; consider IQV (IQV) 3–6 month call spreads (0.5% position) for testing/contract services upside. Hedging: buy a small (1% portfolio notional) put spread on travel exposure via JETS or CCL to protect against short-term demand softness. Contrarian angles: Consensus underrates persistent policy-driven demand — if multiple states adopt school vaccine mandates in next 60–90 days, upside for MRK/CVS is underpriced. Conversely, the market may overreact to headline case counts, overstating national travel impact; leisure shorts should be small and time-boxed. Historical parallel: 2019–2020 measles clusters produced multi-quarter order uplifts for vaccine makers without sustained pharma multiples expansion, so prioritize event-driven, short-dated plays over permanent re-rating bets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.30