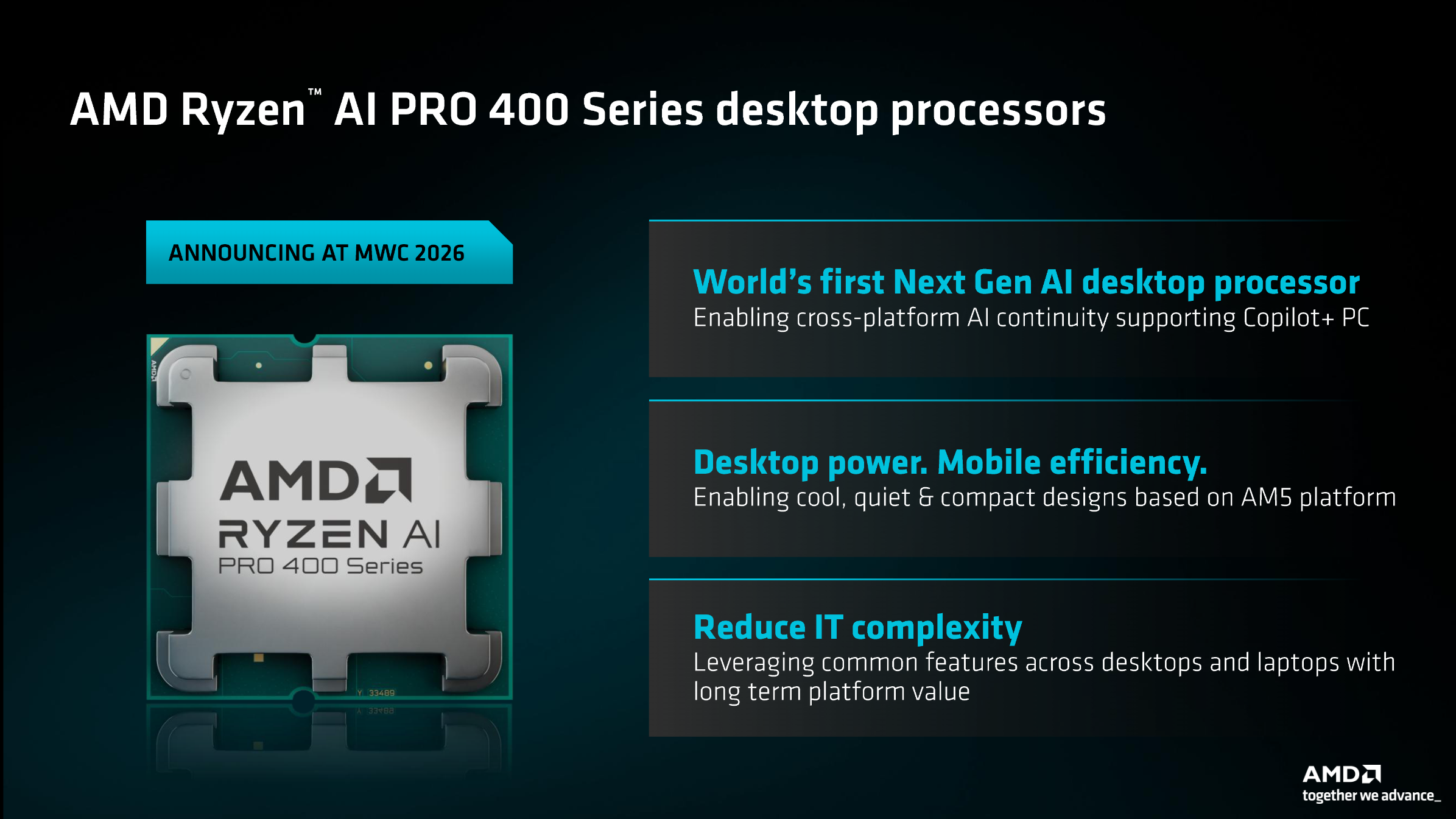

AMD detailed its Ryzen AI 400 desktop APUs—three processor designs delivered as six SKUs with 65W and 35W (E) variants—including the Ryzen AI 7 450G (8 cores/16 threads, 2.0 GHz base, 5.1 GHz boost, 24MB cache, Radeon 860M with 8 RDNA 3.5 CUs, 50 TOPS NPU) and two six-core Ryzen AI 5 parts (440G/435G with Radeon 840M, 50 TOPS). The silicon mirrors the mobile Ryzen AI 400 lineup, fits AM5, carries Microsoft Copilot+ certification, and will be available only in OEM and PRO commercial designs (Q2 2026 target) with 200+ commercial designs and partners including Acer, Asus, Dell, HP and Lenovo.

Market structure: AMD (AMD) gains a differentiated foothold in OEM AI PCs by shipping Zen5 APUs with a 50 TOPS NPU and Copilot+ certification — this targets thin-desktop and enterprise refresh cycles rather than DIY retail. OEM partners (DELL, HPQ, Lenovo, Acer, ASUS) are likely winners if designs hit >200 SKUs as promised; low-end discrete GPU makers may see modest displacement in volume but not high-margin GPU revenue. The requirement of 16GB+ RAM and OEM configuration control suggests downstream ASP lift for systems (mid-single-digit percent) rather than direct silicon price pressure.

Risk assessment: Key tail risks include Microsoft altering Copilot+ specs, OEM uptake falling below 50 commercial designs by end-Q3 2026, or benchmark performance proving substantially behind Intel/NVIDIA alternatives — any of which could compress AMD trade multiples by 10–20% on sentiment. Near-term (days–weeks) volatility should be linked to partner design announcements; short-term (months) outcome hinges on Q2 2026 OEM availability; long-term (≥12 months) depends on AMD expanding to 12-core Gorgon Point and higher-NPU SKUs. Hidden dependencies: RAM supply/pricing and OEM channel inventory dynamics will materially affect system ASPs and unit uptake.

Trade implications: Favor asymmetric exposure to AMD via options and modest equity sized to catalyst cadence: OEM design-win releases (Mar–Jun 2026) and Q2 2026 commercial availability. Microsoft (MSFT) is a strategic beneficiary via Copilot ecosystem; consider tilting cloud/AI exposure toward MSFT over pure-play hardware vendors. Short-duration trades vs Intel (INTC) or low-end GPU vendors could capture near-term share reallocation if benchmarks show AMD parity.

Contrarian angle: Consensus treats this as incremental OEM news — the underappreciated call is that OEM-only rollout forces channel scarcity, which could tighten system ASPs and lift AMD's OEM margins by 3–5% if partners prioritize Copilot-certified SKUs. Conversely, if AMD delays higher-NPU desktop SKUs into 2027, investors pricing immediate disruption are likely overoptimistic; a disciplined trigger-based approach is warranted rather than buy-and-hold.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.10

Ticker Sentiment