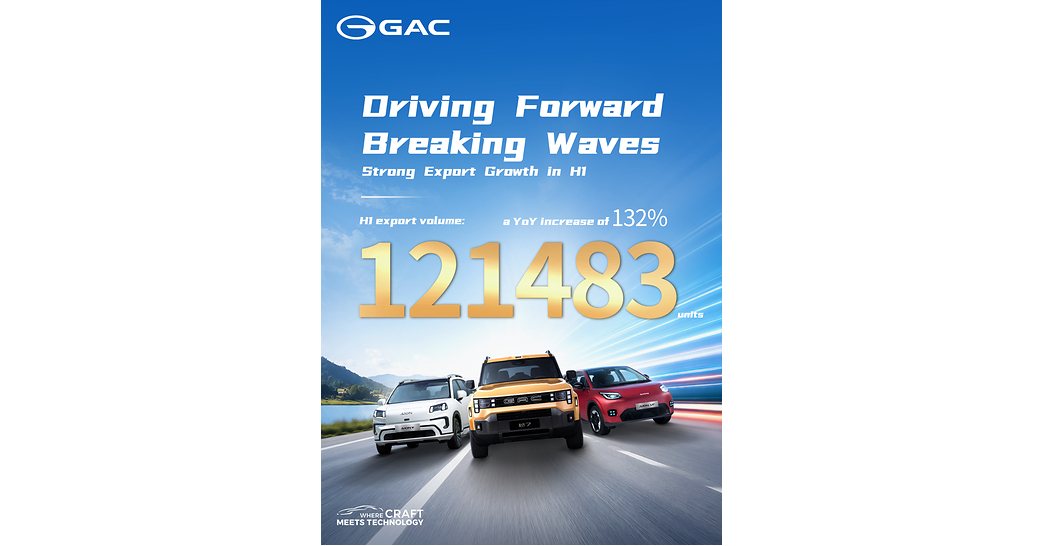

GAC meldet für H1 2026 starkes weltweites Absatzwachstum: Die Auslandsverkäufe (Großhandel/Einzelhandel) haben sich gegenüber dem Vorjahr „mehr als verdoppelt“, während die Gesamtexporte auf 121.483 Fahrzeuge stiegen—nahezu das Vorjahres-Exportvolumen—bei +132% YoY. In Lateinamerika erzielte u. a. Brasilien im Juni +24% YoY und Kolumbien +21% YoY; in Asien verzeichneten u. a. Singapur +30% YoY und Thailand +15% YoY. Insgesamt werden mehrere lokale Marktführerschaften genannt (z. B. AION-Modelle in den Top-10 der BEV-Neuzulassungen in Mexiko sowie Elektro-Taxis).

The market implication is less about this quarter’s P&L and more about proof that a Chinese OEM can build a repeatable overseas distribution engine in price-sensitive markets. If GAC is genuinely converting to retail pull-through rather than simply stuffing dealers, that raises the probability of a multi-year share capture cycle across Latin America and Southeast Asia, where incumbents are most exposed on entry-level EVs and taxis. The second-order winner set extends to China-based battery, parts, and logistics suppliers with better plant utilization, while the losers are legacy Japanese/Korean mass-market OEMs and local assemblers that rely on slow product refreshes and higher brand equity. The main risk is that headline growth can be distorted by low base effects, promotional financing, and inventory builds ahead of policy changes. Over the next 1-3 months, the key catalysts are sequential retail share, dealer inventory days, and gross margin: volume without margin would argue this is a channel-expansion story, not a durable earnings story. Over 6-18 months, the thesis only works if GAC can localize service, spare parts, and financing; otherwise the growth is vulnerable to FX swings, tariff responses, and political noise in markets like Mexico, Brazil, and parts of the Middle East/Africa. Consensus is likely underestimating how quickly Chinese automakers can move from "export curiosity" to structural share in emerging markets, but the move is still unproven at scale. That makes GAC more interesting as a relative-value re-rating candidate than as a pure momentum name. The contrarian risk is that once competitors cut prices, the volume surge normalizes quickly and margins compress before the market credits the channel gains.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.55