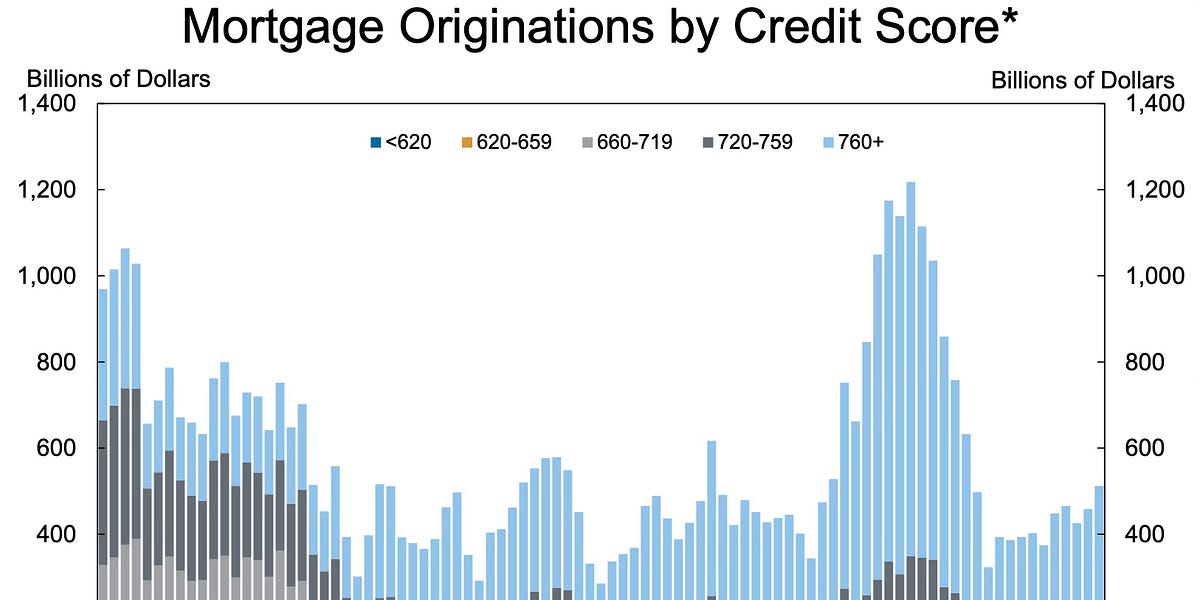

The Q3 NY Fed Report on Household Debt and Credit reveals a slight uptick in mortgage originations to $512 billion in 2025Q3, though credit quality saw a marginal decline with median and 10th percentile credit scores decreasing by 2 and 3 points, respectively. Despite this, underwriting standards remain robust compared to the pre-2008 bubble, with most new loans extended to high credit score borrowers. A notable concern is the increase in transition rates to 30-60 day and seriously delinquent (90+ days) mortgage statuses, now approaching pre-pandemic levels. Additionally, foreclosures, while still below pre-pandemic figures, have risen over the past three quarters, likely due to the expiration of the VA foreclosure moratorium.

The Q3 NY Fed Report indicates a slight increase in mortgage originations, reaching $512 billion in 2025Q3, up from $458 billion in the prior quarter. While the median credit score for new originations declined by 2 points and the 10th percentile by 3 points, overall underwriting standards remain robust. A significant majority of new loans are still extended to borrowers with credit scores above 760, contrasting sharply with the 2003-2006 bubble period. A notable concern emerges from rising delinquency rates. The transition rate from current to 30-60 days late increased in Q3, now approaching pre-pandemic levels. Furthermore, the transition to seriously delinquent (90+ days) status also saw an increase in Q3, warranting close monitoring by investors. Foreclosures have increased over the last three quarters, likely attributable to the expiration of the VA foreclosure moratorium. Despite this uptick, current foreclosure levels remain significantly below pre-pandemic figures and do not exhibit the localized concentration seen during the 2008 housing bust. The overall tone is cautious, reflecting mixed credit quality signals within a generally stable housing market.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.00