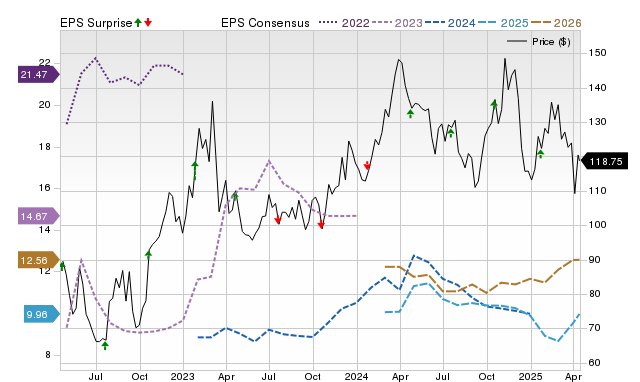

Steel Dynamics (STLD) is anticipated to report a significant year-over-year earnings decline of 25% to $2.04 per share for the quarter ending June 2025, despite a projected 0.8% revenue increase to $4.67 billion. While the consensus EPS estimate saw a slight 0.33% upward revision recently, the company's Zacks Earnings ESP of 0% combined with a Zacks Rank of #3 makes a definitive earnings beat prediction challenging. Although STLD has a history of beating EPS estimates in the past four quarters, the current analysis suggests it is not a compelling candidate for an earnings surprise, indicating potential volatility based on the actual results released around July 21.

Steel Dynamics (STLD) is approaching its Q2 2025 earnings release with a consensus forecast for a significant 25% year-over-year decline in earnings per share to $2.04. This sharp contraction in profitability is expected despite projected revenues remaining relatively flat, with a slight 0.8% increase to $4.67 billion, which points towards considerable margin pressure. While analyst consensus for EPS has seen a marginal upward revision of 0.33% in the last 30 days, predictive models suggest a low probability of a positive surprise. The company's Zacks Earnings ESP (Expected Surprise Prediction) is 0%, and it holds a Zacks Rank #3 (Hold), a combination that makes it difficult to conclusively anticipate an earnings beat. This neutral quantitative outlook is notable given STLD's consistent history of surpassing EPS estimates in each of the last four quarters, creating a conflict between past performance and current indicators. Consequently, the market's reaction will likely hinge less on the headline numbers and more on management's forward guidance and commentary on underlying business conditions.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment