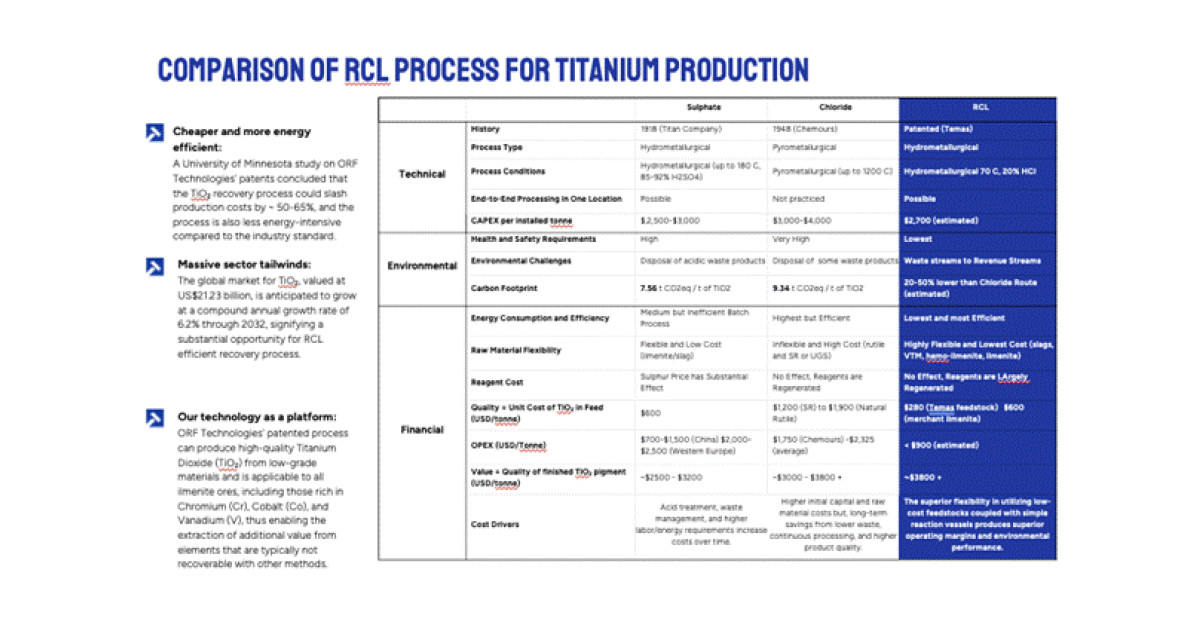

Temas initiated a process patent filing for chromium extraction using its Regenerative Chloride Leach (RCL) technology (“Chloride-based process for Chromium extraction”) with a July 10, 2026 priority date. The company frames the move as expanding its RCL licensing moat beyond titanium and vanadium, building on previously filed vanadium IP and supported by metallurgical testwork; it also highlights that RCL claims up to 65% lower processing costs and a reduced environmental footprint. Overall, this is incremental positive for Temas’ critical-minerals technology platform, but it is unlikely to be immediate earnings- or market-moving beyond modest investor sentiment.

This is a narrative-extension event, not an earnings event. A new patent filing only matters if it translates into third-party validation, licensing terms, or a lower-cost processing route that can be financed at scale; until then, TMASF remains mostly a story stock with dilution risk. The near-term market reaction should be driven by retail/OTC optionality, but the economic value is still heavily discounted because process IP is difficult to monetize without a credible partner and repeatable metallurgical results.

The second-order winner, if the platform works, is not Temas’ own ore inventory but stranded or complex ore owners that need a lower-capex route to monetize marginal feed. That can pull business away from conventional toll processors and incumbent metallurgical flow-sheet vendors over a 6-18 month horizon, especially where ESG permitting or energy costs are bottlenecks. The counterpoint: patents around extraction chemistry often look broader on paper than they are in practice, so the real competitive moat will be measured by recoveries, reagent consumption, and impurity rejection—not the number of filings.

The main risk is that this becomes a financing catalyst rather than a commercial catalyst: more IP claims can increase the equity story, but if no partner signs, the company may need to raise capital before revenue arrives. Watch for a reversal if there is no disclosed third-party test data or licensing framework within 1-2 quarters, or if a future raise lands at a discount. If chromium/stainless demand weakens, the willingness of miners to pay for processing innovation also drops, which would undercut the licensing thesis faster than the patent narrative can compensate.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment