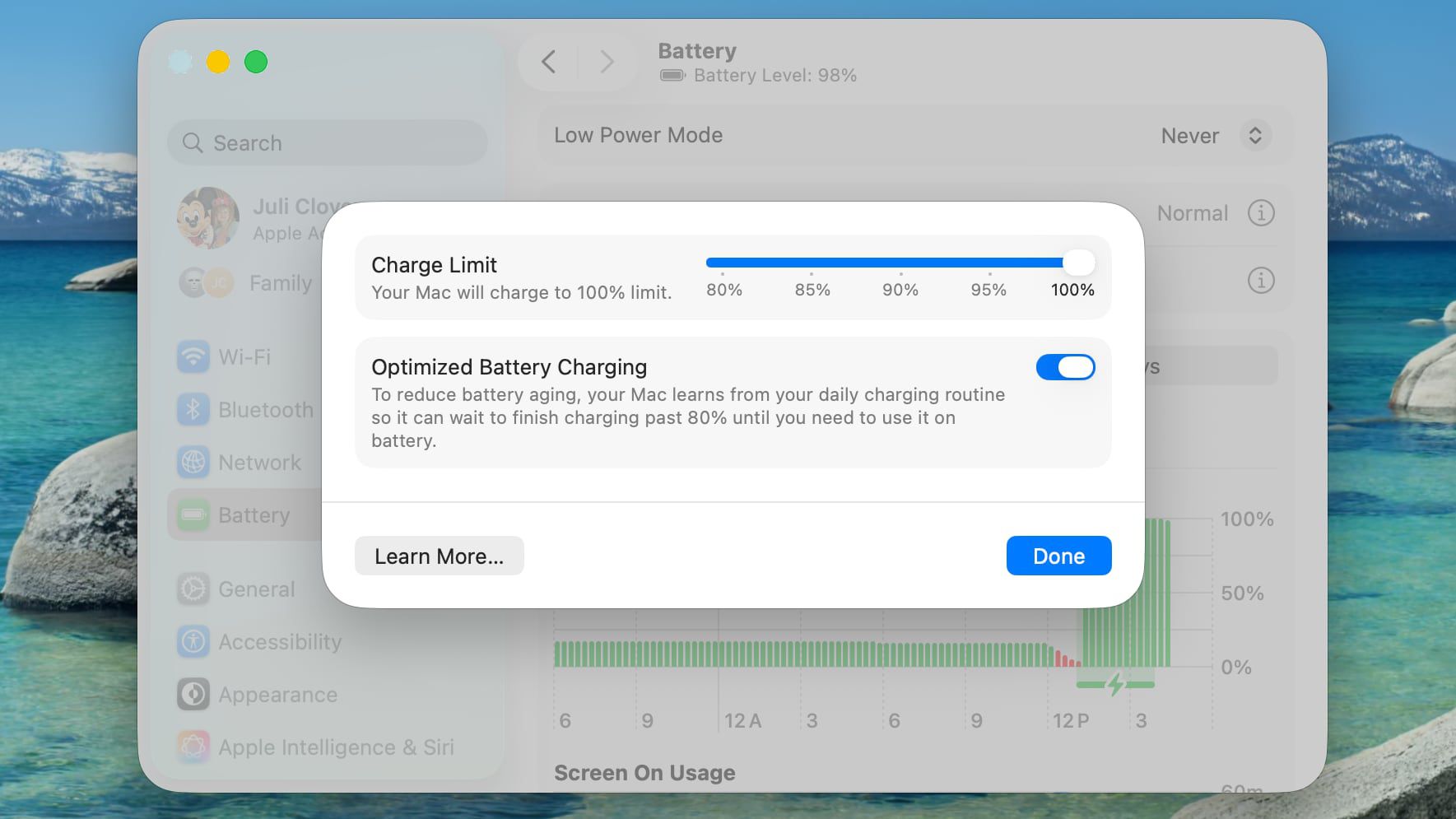

Apple's macOS Tahoe 26.4 beta introduces a Charge Limit feature that lets users hard-cap Mac charging at 80, 85, 90, 95 or 100 percent via a new slider in System Settings (Battery → Charging → i). The setting complements Optimized Battery Charging by preventing full charges to extend battery longevity, mirroring a capability introduced for iPhone with the iPhone 15 line; the change is a modest product-quality enhancement with limited near-term financial impact but could slightly improve device lifecycle and customer satisfaction.

Market structure: Apple (AAPL) is the direct beneficiary — incremental product polish that increases perceived device longevity and customer satisfaction, supporting Services/AFS revenue and brand retention. Peripheral winners include Apple Services and authorized-repair channels on quality/upsell; losers are marginal — small third‑party battery/replacement businesses and highly unit‑dependent component suppliers who rely on tight replacement cycles. Net impact on unit demand is likely modest but persistent: if average replacement cycles lengthen by ~6–12 months over 2–3 years, global device unit growth could be shaved by a few percent annually, pressuring smaller suppliers' volumes. Risk assessment: Near-term risk is low (days–weeks) — feature is incremental software; medium/long-term (months–years) the tail risks rise: regulatory (right‑to‑repair, forced parts access), software rollback/bug causing recalls, or a measurable drop in unit volumes that depresses supplier earnings. Hidden dependencies include service-revenue offsets (fewer replacements may raise Services per user) and potential margin compression for parts suppliers. Catalysts to watch: Apple March 4 event (9am ET), inventory signals for iPhone 16e/iPad Air over next 2–6 weeks, and Apple earnings/volume guidance in next two quarters. Trade implications: Tactical: overweight AAPL ahead of product cadence and inventory-driven scarcity — consider a 2% long position (target +8–12% in 3 months, stop‑loss 8%). Options: buy a 3‑month AAPL call spread (buy 10% OTM / sell 20% OTM) sized to 1–2% notional to capture event upside while capping premium. Relative play: pair long AAPL / short Global X Lithium & Battery Tech ETF (LIT) 1:0.5 weight as a hedge vs longer device life reducing marginal lithium demand over 6–12 months; trim if LIT rallies >15%. Contrarian angles: Consensus underestimates the long-run impact of extended lifecycles on commodity and small‑cap supplier earnings; the market is likely underpricing a 2–5% structural hit to component volumes over 2–4 years. Conversely, the reaction is probably overdone for Apple itself — better device longevity can lift lifetime ARPU and Services margins, offsetting unit pressure. Historical parallel: handset cycles lengthened in past mature markets, concentrating margins in platform owners (favors AAPL over minnows).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment