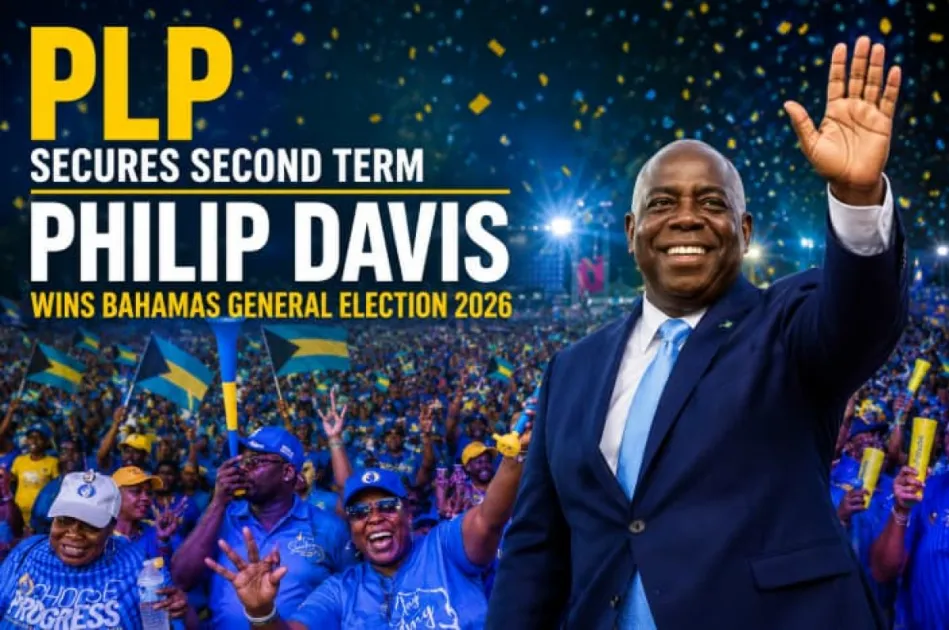

Prime Minister Philip Davis and the Progressive Liberal Party won a second consecutive term in The Bahamas, securing more than 30 parliamentary seats versus 8 for the opposition FNM. Davis becomes the first Bahamian prime minister in over 30 years to win re-election for a second straight administration, and he says the mandate will be used to grow the economy, improve safety, and ease pressure on families. The snap election was called early to avoid disruption during hurricane season.

The immediate market read is not policy change but policy continuity, which matters because it lowers the probability of a near-term fiscal wobble in a tourism- and services-led economy that is highly sensitive to confidence. The bigger second-order effect is on execution risk: a strong mandate should improve the government’s ability to push through port, airport, housing, and public safety spending without the coalition friction that often delays capex in small EMs. That tends to be mildly supportive for local banks, construction contractors, and any external suppliers tied to infrastructure and hospitality upgrades.

The key overhang is not politics per se, but weather. Calling an early election to avoid hurricane-season disruption underscores that the real macro tail risk for the next 3-5 months is storm exposure, not parliamentary instability. In practice, that means any “post-election relief rally” in domestic risk assets could fade fast if storm tracks turn adverse; for this market, a single major hurricane can overwhelm the signal from the election and reverse sentiment in days.

Contrarian angle: the result may be more bearish for reform optionality than headline-positive for stability. A decisive majority reduces the odds of policy concession-making, which can slow reform momentum once the electoral premium is priced out. The consensus will likely overvalue the symbolic continuity and undervalue the mundane but important issue of policy delivery capacity; in small economies, execution is what moves credit spreads and FDI, not speeches.

For the region, the main beneficiary is likely the domestic demand complex rather than sovereign risk itself: if administration continuity translates into faster permitting and public works, the near-term winners are contractors, materials, and banks with local loan growth exposure. But the trade should be sized around storm risk and timing, because the base case is a 1-2 quarter confidence uplift, while the tail case is an exogenous weather shock that makes the election irrelevant.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.15