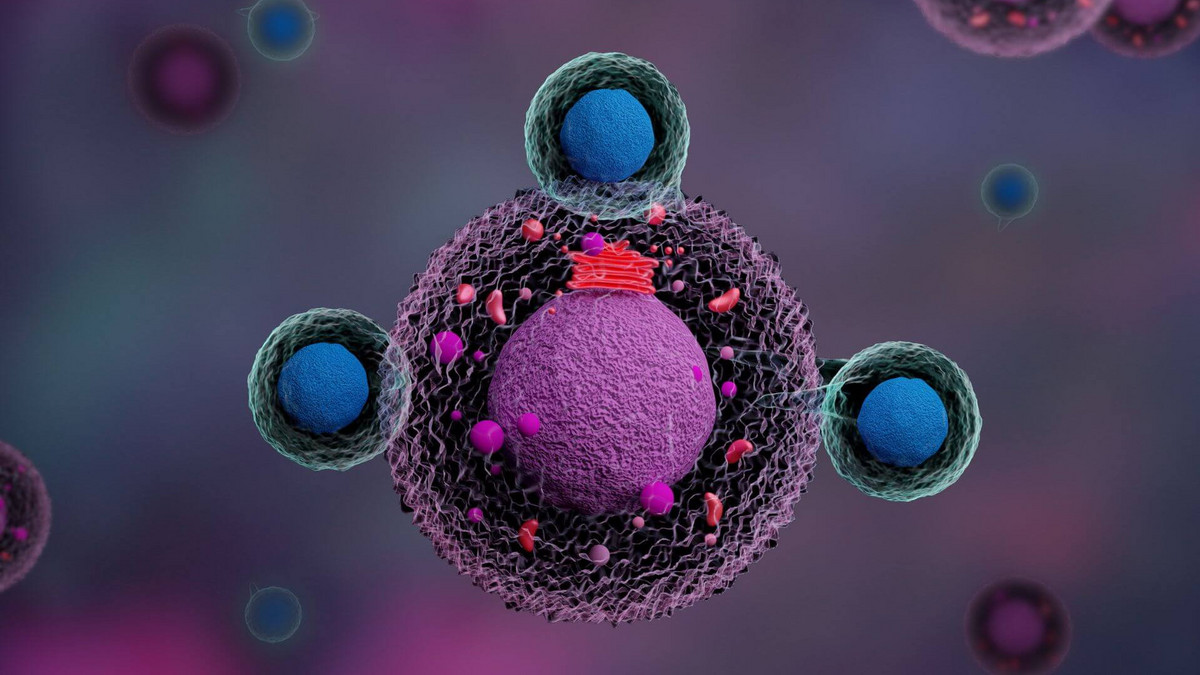

Hôpital Maisonneuve-Rosemont treated the first Canadian patient with allogeneic CAR-T therapy in the Phase 1 Resolution clinical trial, marking an innovative step in autoimmune disease treatment. The trial targets severe refractory lupus, myositis, and scleroderma, and Canada has only one participating site. The news is clinically encouraging but remains early-stage and unlikely to have near-term market impact.

This is a meaningful signal for the cell-therapy platform, but the market is likely to underprice how much the innovation changes operational bottlenecks rather than just therapeutic optionality. Allogeneic manufacturing compresses the delivery cycle from a bespoke, patient-dependent process into a semi-inventory model, which is strategically important because speed and batch readiness are what ultimately determine whether these therapies scale beyond elite centers. That shifts value toward firms with real-world expertise in donor-cell engineering, cryopreservation, logistics, and contamination control—not just the underlying clinical indication. The first-order beneficiaries are likely to be enabling-platform names across cell processing, closed-system manufacturing, and cold-chain logistics, even if they are not named in the article. The second-order effect is competitive: autologous CAR-T franchises face a subtle narrative headwind if allogeneic programs prove safer and operationally simpler in autoimmune disease, because the addressable market is larger but reimbursement will only expand if treatment can be deployed without multi-week wait times. A successful signal in lupus or scleroderma would also pull capital toward adjacent allogeneic programs in oncology and immune reset therapies, potentially re-rating the whole ex vivo cell-engineering stack over 6-18 months. The main risk is clinical, not market, and that matters for timing. Phase 1 is a proof-of-mechanism window, so near-term enthusiasm can overshoot on a single-patient or small-cohort readout, while the real gating items are durability, relapse, and infection risk over 3-12 months. If efficacy is modest or immunosuppression requirements remain heavy, the allogeneic angle becomes an operational curiosity rather than a platform shift. The contrarian view is that the narrative may be too centered on novelty and not enough on reimbursement friction. Even if the therapy works, autoimmune indications are far larger but far less concentrated than oncology, so payer adoption may be slower unless the therapy clearly reduces hospitalizations and chronic immunosuppressant spend. That creates a longer commercialization curve than the early optimism implies, which should cap multiple expansion in the absence of strong safety and durability data.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35