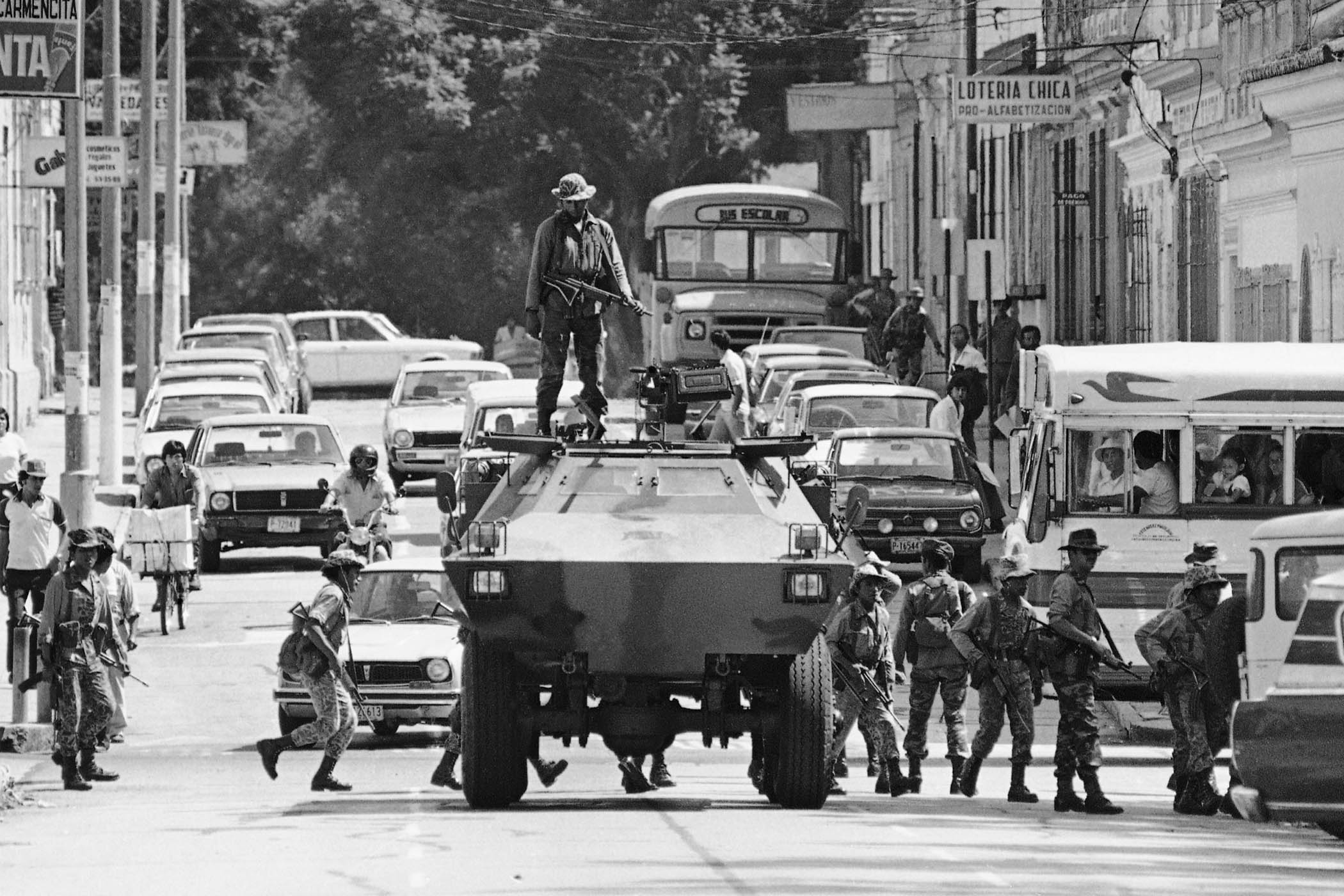

The article situates a reported special-forces attempt to seize Nicolás Maduro in Venezuela within a broader history of U.S.-backed regime change in Latin America, citing CIA operations in Guatemala (1954 Operation PBSuccess) and the Congo as precedents. It argues such interventions have historically produced prolonged instability, civil conflict and unpredictable consequences, signaling elevated geopolitical risk and potential regional instability that investors should treat as a downside risk to assets tied to Venezuela and nearby markets.

Market structure: A US-led regime-change operation raises demand for defense/ISR suppliers (Lockheed LMT, Raytheon RTX, GD) and creates flight-to-quality into USD, Treasuries and gold. Short-term oil price upside is probable if regional logistics or Venezuelan output is disrupted — a 5–15% spike in Brent within 2–6 weeks is plausible; Latin American equity/FX baskets (ILF, EWZ exposure) will suffer immediate capital outflows and widening CDS spreads. Cross-asset: expect FX stress in COP, MXN and BRL (-3–8% vs USD in 1–4 weeks), Treasuries to outperform equities, and elevated equity vol (VIX +5–12pts if escalation occurs). Risk assessment: Tail risks include expanded US military engagement, regional spillover (Colombia, Brazil), and comprehensive sanctions that freeze assets — low-probability but >5% market-impact events that would widen EM sovereign CDS by +200–500bp. Time horizons: immediate (days) for volatility and flight to safety; short-term (weeks–months) for oil and defense revenue recognition; long-term (quarters–years) for FDI withdrawal and structural risk premia in LatAm. Hidden dependencies: remittance flows, mining concessions and supply chains in neighboring countries could transmit shocks. Trade implications: Tactical longs in defense (ITA or 1–2% positions in LMT/GD/RTX) and short LatAm equity ETFs (ILF) are asymmetric; buy 30–90d Brent call spreads or XLE if Brent >$85 triggers further momentum. Hedging: purchase 30–60d VIX call spreads (25/40) sized 0.5–1% and add short-dated GLD puts only if gold < $1,900 holds. Rotate 3–6% of portfolio from EM ex-Brazil equities into US staples/utilities and 7–10y Treasuries (TLT) for 1–3 months. Contrarian angles: The market may overshoot defense and oil rallies; a rapid diplomatic de-escalation could cause a 10–20% snapback in beaten-down LatAm names — avoid fully one-sided shorts and use pairs/options. Historical parallels (2003 Iraq spike then mean-reversion) suggest layering with time-decaying hedges: sell premium after vol normalizes. Unintended consequences include sanctions pushing buyers to non-US suppliers, capping long-term upside for US defense exporters if procurement shifts away — size positions to 1–3% and re-assess at 30–60 day catalyst points.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40