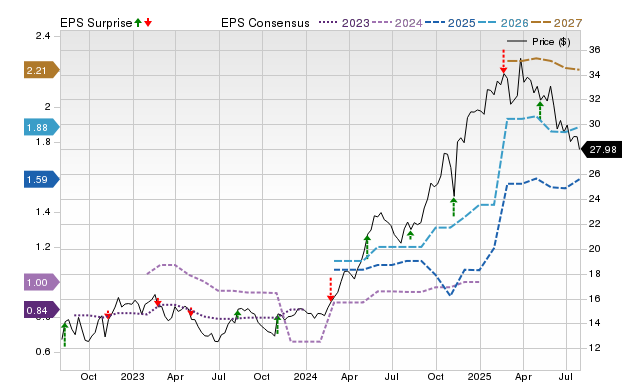

Primo Brands (PRMB) is projected to report significant growth for the June 2025 quarter, with consensus estimates forecasting EPS of $0.43 (+65.4% YoY) and revenues of $1.8 billion (+271.2% YoY) when results are released on August 7. Despite these robust top-line expectations, Zacks' analysis indicates a low probability of an earnings beat, evidenced by a negative Earnings ESP of -4.12% and a Zacks Rank of #3, suggesting recent bearish analyst sentiment on the company's earnings prospects. This makes PRMB an uncompelling candidate for an earnings surprise, prompting investors to consider broader fundamental factors beyond consensus growth.

Primo Brands (PRMB) is approaching its June 2025 earnings release with exceptionally strong consensus expectations, forecasting a 65.4% year-over-year increase in EPS to $0.43 and a 271.2% surge in revenue to $1.8 billion. Despite this robust growth outlook and a marginal 0.21% upward revision in the consensus EPS estimate over the last 30 days, leading indicators suggest a heightened risk of a negative surprise. The company's Zacks Earnings ESP (Expected Surprise Prediction) is -4.12%, indicating that the most recent analyst estimates are trending below the consensus, a bearish signal. This negative ESP, combined with a neutral Zacks Rank of #3 (Hold), makes it statistically difficult to predict an earnings beat. This cautious forward-looking indicator stands in contrast to PRMB's strong track record, having surpassed EPS estimates in three of the last four quarters, including a 20.83% beat in the prior period. The resulting picture is one of a high-growth narrative facing a potential near-term disappointment.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment