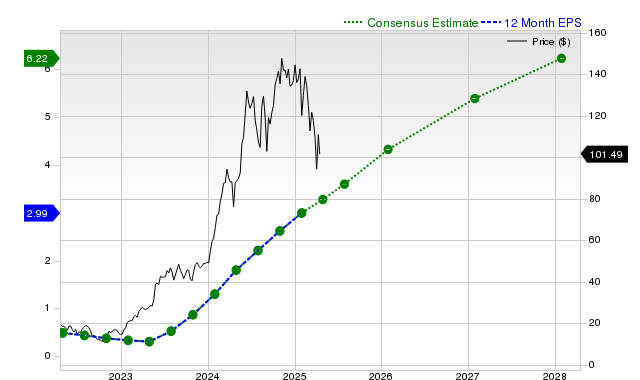

NVIDIA (NVDA) has recently underperformed the S&P 500 and its industry, but strong upward revisions in consensus earnings estimates for the current quarter and next fiscal year, projecting EPS growth of over 50% and 38% respectively, have led to a Zacks Rank #2 (Buy). Despite a premium valuation indicated by a Zacks Value Style Score of 'D', the company's consistent revenue and EPS beats, alongside robust revenue growth forecasts exceeding 30% annually, suggest potential near-term market outperformance.

Despite recent underperformance where its shares returned -2.7% over the past month against the S&P 500's +3.4% gain, NVIDIA's fundamental outlook appears robust based on analyst revisions. Sell-side analysts have significantly increased earnings estimates, with the current quarter EPS forecast at $1.23, a +51.9% year-over-year increase, and the consensus estimate having risen +5.8% in the last 30 days. This positive revision trend extends to the full fiscal years, with current year EPS expected to grow +48.5% and the next fiscal year by +38.9%. This earnings momentum is supported by strong revenue projections, including a +55.5% year-over-year growth forecast for the current quarter and over 30% growth anticipated for the next fiscal year. While the company has a strong history of beating consensus, having surpassed revenue estimates for four consecutive quarters, its valuation remains a key consideration. The stock holds a Zacks Value Style Score of 'D', indicating it trades at a premium relative to its peers. Nevertheless, the powerful upward trend in earnings estimates has earned it a Zacks Rank #2 (Buy), suggesting a potential for near-term market outperformance.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.75

Ticker Sentiment