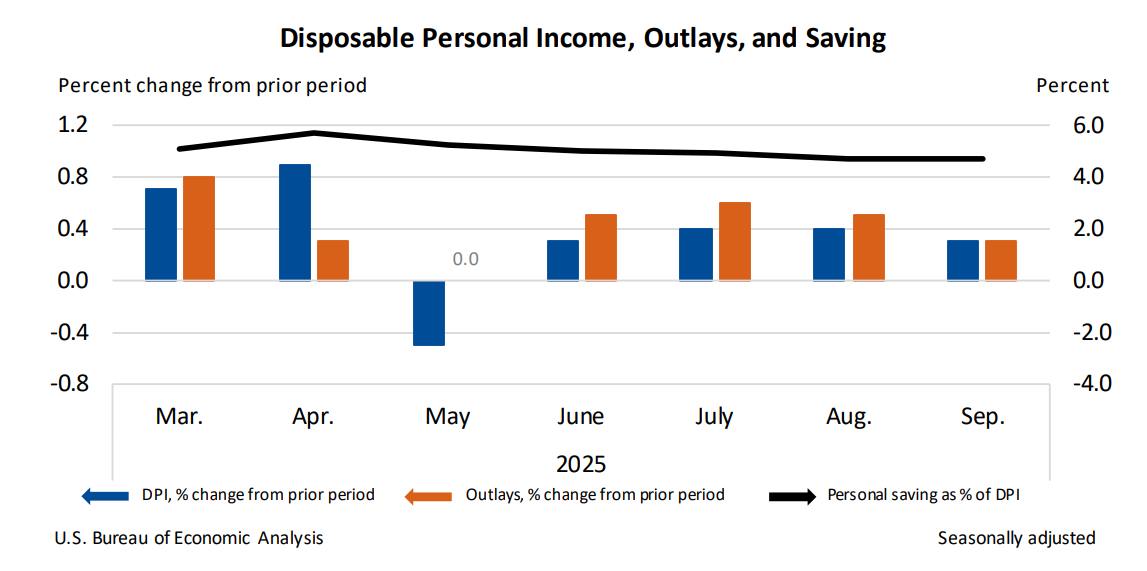

September personal income rose $94.5 billion (0.4% m/m) while disposable personal income increased $75.9 billion (0.3%) and PCE rose $65.1 billion (0.3%), driven largely by a $63.0 billion increase in services. The PCE price index climbed 0.3% m/m and 2.8% y/y (core PCE +0.2% m/m, +2.8% y/y); real PCE was flat and the personal saving rate was 4.7%. Wages and supplements were key contributors (private wages +$41.2B, government wages +$7.1B, supplements +$10.7B) and dividend income increased $19.8B; BEA noted revisions for July–August and will update monthly data with the Q3 GDP release on Dec. 23, 2025.

Market structure: The data show services-led consumption (services +$63B vs goods +$2.1B) and a modest real DPI increase (+0.1%), signaling winners in travel, leisure, dining and service-heavy consumer discretionary chains (relative margin expansion) while goods retailers and discretionary durable manufacturers face demand headwinds and margin pressure. Higher dividend receipts (+$19.8B) and rising compensation (+$41.2B private wages) boost household asset income — positive for banks and asset managers — but the 4.7% saving rate leaves limited buffer if incomes slow. Cross-asset: 2.8% YoY core PCE keeps inflation risk non-trivial, supporting shorter-duration yields and TIPS; USD strength is likely to persist on sticky inflation while commodity sensitivity is muted because inflation is services-driven. Risk assessment: Tail risks include a persistent-services inflation shock forcing Fed hikes (probability ~15% over 3 months if core PCE >2.8% for consecutive releases) or a consumer retrenchment/recession if savings dips below 4.0% and real PCE turns negative. Immediate (days): market repricing around Fed comments; short-term (weeks–months): holiday services demand could amplify trends; long-term (quarters): wage-driven inflation could compress corporate margins. Hidden dependencies: dividend increase may reflect buyback timing, not sustainable cash-flow growth; corporate payroll seasonality can distort one-off consumption beats. Trade implications: Favor overweight in service-oriented consumer discretionary and financials while underweight goods retail. Tactical allocation: buy short-dated call spreads on resilient service names rather than broad buys, add TIPS duration as insurance, and use pair trades to isolate demand-shift exposure. Use strict triggers: reduce equity risk if core PCE >2.8% for two prints or savings rate <4.0%. Contrarian angles: The market may overprice a permanent hawkish Fed reaction; services inflation can roll over faster if labor demand softens — creating a 3–6 month window to re-enter long-duration Treasuries (TLT) and cut hedges. Historical analog: 2010–2012 services-inflation episodes faded without deep rate cycles; unintended consequence of an aggressive tightening would be hitting bank credit and dividend sustainability, creating short opportunities in weaker regional banks.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.10