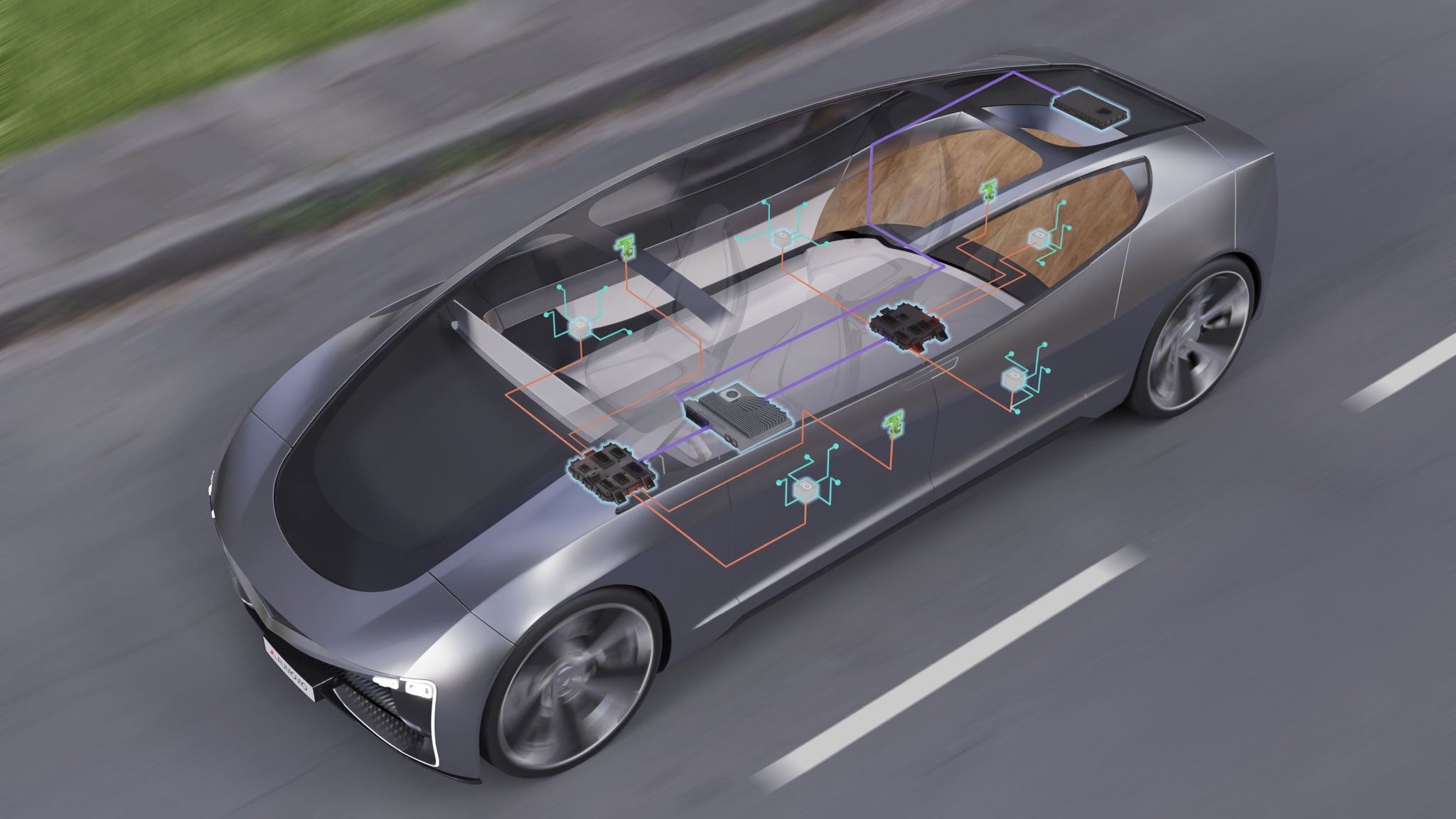

CES 2026 is expected to spotlight autonomous driving, robotics and semiconductor technology, with vendors showcasing new software-defined vehicle concepts; Aumovio plans to present a “software-defined vehicle architecture concept.” The coverage highlights industry emphasis on vehicle software stacks and chipmakers’ roles (including Qualcomm) rather than concrete financial disclosures, indicating strategic technology direction for auto and semiconductor suppliers but limited near-term market-moving news.

Market structure: CES focus on software-defined vehicles (SDV), robotics and chips concentrates pricing power with semiconductor IP and foundry-linked players (QCOM, NVDA, TSM, ASML) and software/Tier‑1 integrators (APTIV, MBLY). Legacy dealers and commodity OEM suppliers face margin erosion as value migrates to software stacks and AD/AI compute; expect OEMs that secure long‑term silicon/SoC contracts to gain 200–500bp of gross margin over 3–5 years. Tight foundry capacity signals 5–15% higher ASPs for advanced nodes in the next 12–24 months, pushing semi equipment and fab stocks outperforming autos and parts retailing. Risk assessment: Tail risks include regulatory slowdowns on AD deployment, a major AV safety incident causing multi-quarter demand shocks, or a TSMC yield/concentration event that raises lead times >6 months; each could halve expected incremental revenue for chip vendors in the short term. Immediate (days–weeks): CES press flow and QoQ guidance updates; short (3–9 months): supply deals and capex announcements; long (3–5 years): structural SDV adoption and recurring software revenues dependent on ARM/5G/OS licensing and sovereign policy. Hidden dependencies: foundry sloting, EDA/IP licensing (ARM), and 5G network rollout for V2X latency targets. Trade implications: Direct: establish a 2–3% long on QCOM (capture SDV/licensing upside) and a 1–2% long on NVDA or TSM (AI compute exposure); add 0.5–1% long ASML for equipment leverage. Pair: long QCOM vs short STLA (1–2%) to play software value capture vs dealer/value erosion. Options: buy 3–6 month QCOM call spreads sized 0.5–1% portfolio risk to hedge execution (prefer spreads to outright calls); overweight semiconductors and software, underweight auto retail and commodity parts for next 6–12 months. Entry: scale into positions within 2–6 weeks post‑CES announcements; exit or re-evaluate on material OEM contract wins/losses or QCOM quarterly guidance (next 90 days). Contrarian angles: Consensus underestimates execution risk and the likelihood of verticalization—OEMs may in‑source software or form exclusives, compressing supplier multiples; conversely, the market may underprice recurring software/SaaS revenue (20–30% incremental margin) that could re‑rate select names. Historical parallel: smartphone SoC consolidation benefited Qualcomm after a multi‑quarter trough—if QCOM trades down >8% on short‑term noise, add to 3–4% weight. Unintended consequence: rapid SDV rollouts could trigger regulatory retrofits and warranty costs, creating 6–12 month volatility spikes—prefer equity exposure over leveraged long-dated volatility bets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment