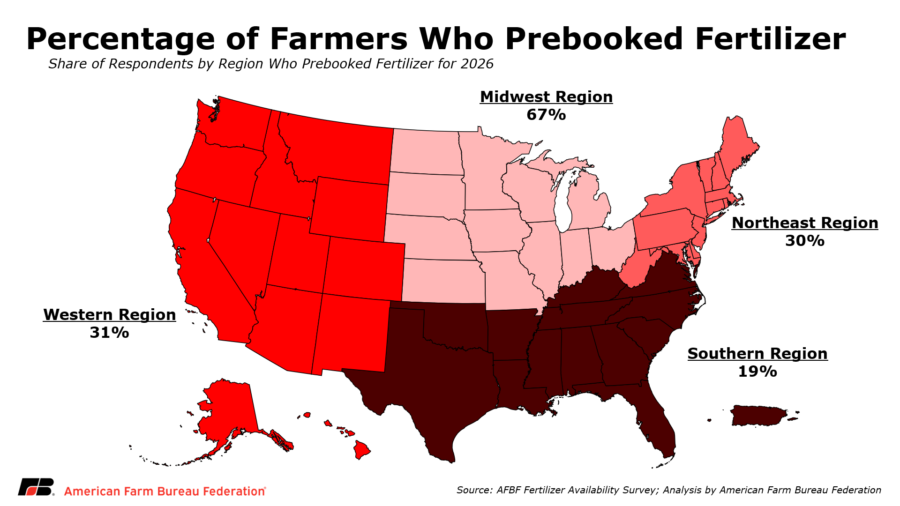

Farm input costs are surging as Middle East disruptions and the Strait of Hormuz closure push nitrogen fertilizer prices up more than 30%, urea up 47% since end-February, and farm diesel up 46%. More than 90% of surveyed farmers said their financial condition has worsened or stayed the same, and over half cannot afford all needed fertilizer, raising risk to 2026 yields and acreage decisions. The article suggests broader pressure on agriculture margins and potential support for additional farm aid.

The immediate market read is not “farm stress” but a second-order inflation impulse through two bottlenecks that are unusually sticky: nitrogen-derived fertilizer and diesel. That combination hits input costs, transport, and irrigation simultaneously, which means the pain shows up in margins before it shows up in acreage — and that lag makes the next two USDA data prints the key catalyst window. If supply disruptions persist for even one more purchasing cycle, the market will start pricing not just higher 2025 costs but lower 2026 application intensity, which is a more durable demand shock to ag inputs.

The relative loser set is broader than crop growers: fertilizer distributors with low inventory flexibility, rail/truck logistics tied to Midwest movement, and agrochemical/input resellers that cannot pass through costs in real time are exposed to working-capital compression. By contrast, integrated energy names and LNG-linked gas producers gain an indirect tailwind because nitrogen economics are gas-sensitive; any sustained gas bid raises replacement costs just as farmers lose affordability. A less obvious beneficiary is grain merchandisers if the market begins discounting yield risk and acreage reshuffling, because volatility in basis and origination typically improves trading opportunities even as physical volumes weaken.

The contrarian risk is that the move in fertilizer is already doing policy work: farmers are rationing now, so spot demand may roll over before the full price spike is visible in downstream margins. That creates a “bad news is known” setup over the next 4-8 weeks if Middle East flows normalize or if inventory coverage proves better than feared. The larger tail risk is an earnings reset in 2026 rather than an immediate crop failure — reduced nutrient application would hit yields with a delay, so the market may underprice the duration of the shock until summer acreage and later yield reports confirm it.

For a tradeable expression, I would bias toward long energy over agriculture inputs: the energy leg benefits immediately from the geopolitical premium, while ag input beneficiaries face political and inventory-reversal risk. The cleanest short-term opportunity is a paired short in fertilizer-sensitive ag names against an energy basket, with the thesis that margin pressure arrives faster than any offset from higher commodity prices. Keep duration short until the next USDA and acreage data because resolution in shipping lanes could unwind the trade quickly, but if disruptions persist into the summer, the setup becomes a multi-month earnings downdraft for fertilizer demand.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.62