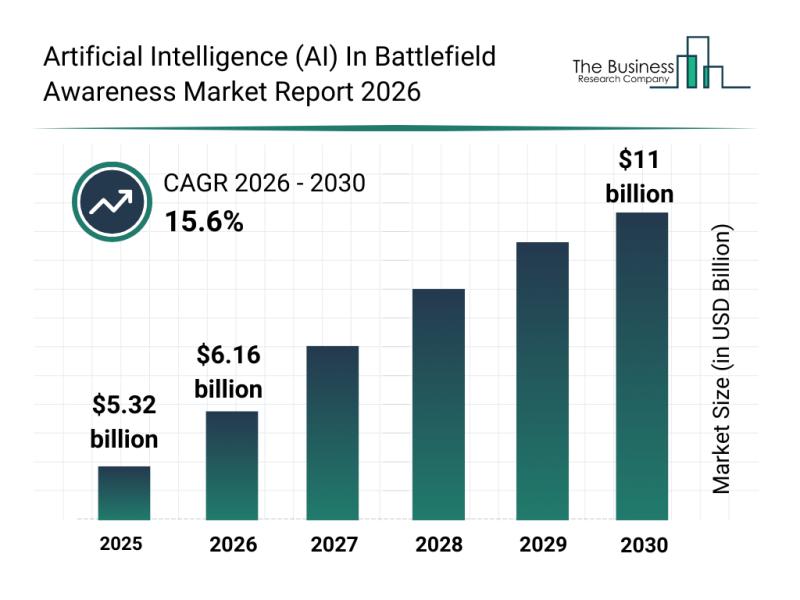

The AI in battlefield awareness market is projected to reach $11 billion by 2030, implying a 15.6% CAGR over the forecast period. Growth is being driven by predictive threat analysis, AI-enabled autonomous vehicles and drones, cloud-based battlefield management, and multi-sensor fusion for real-time situational awareness. NATO's undisclosed purchase of an AI-powered military system from Palantir and Leonardo DRS's launch of the Artificial Intelligence Processor underscore rising defense demand, but the article is largely a sector outlook rather than a direct market-moving event.

This is less a broad “AI defense” story than an inflection in command-and-control software budgets. The near-term winners are the firms that can sit at the center of sensor ingestion, model orchestration, and decision workflow integration; that favors platform incumbents and specialized software vendors over pure hardware primes. The second-order effect is margin expansion for software-heavy defense franchises as the budget shifts from one-time platform procurement toward recurring data, integration, and sustainment contracts. The biggest underappreciated beneficiary is the vendor that becomes the default interoperability layer across allied systems. NATO-style purchases and coalition warfare imply the buyer is optimizing for secure fusion across heterogeneous assets, which structurally advantanges firms with existing government trust, data rights, and deployment speed. That also raises the bar for smaller hardware names: if their devices are not open-architecture and API-native, they risk being commoditized as sensor suppliers while value accrues upstream to the software stack. For the rest of the defense group, the market is likely overestimating immediate revenue and underestimating long-cycle certification friction. Battlefield AI adoption will be lumpy: pilots convert to production over quarters to years, but once embedded, switching costs are high and follow-on services can outgrow initial licenses. The key risk is procurement delay or adverse publicity around model errors/autonomy, which could slow adoption temporarily without changing the long-run budget trend. The contrarian view is that the current enthusiasm may be too narrow. The real monetization may not be in “AI” branding but in the unsexy infrastructure beneath it—secure cloud, edge compute, rugged processors, and integration services—so some of the best risk/reward sits in picks-and-shovels names rather than headline software platforms. If battlefield AI becomes a feature rather than a standalone product, the valuation premium could migrate from vision-level software to the suppliers that make deployment reliable in contested environments.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment