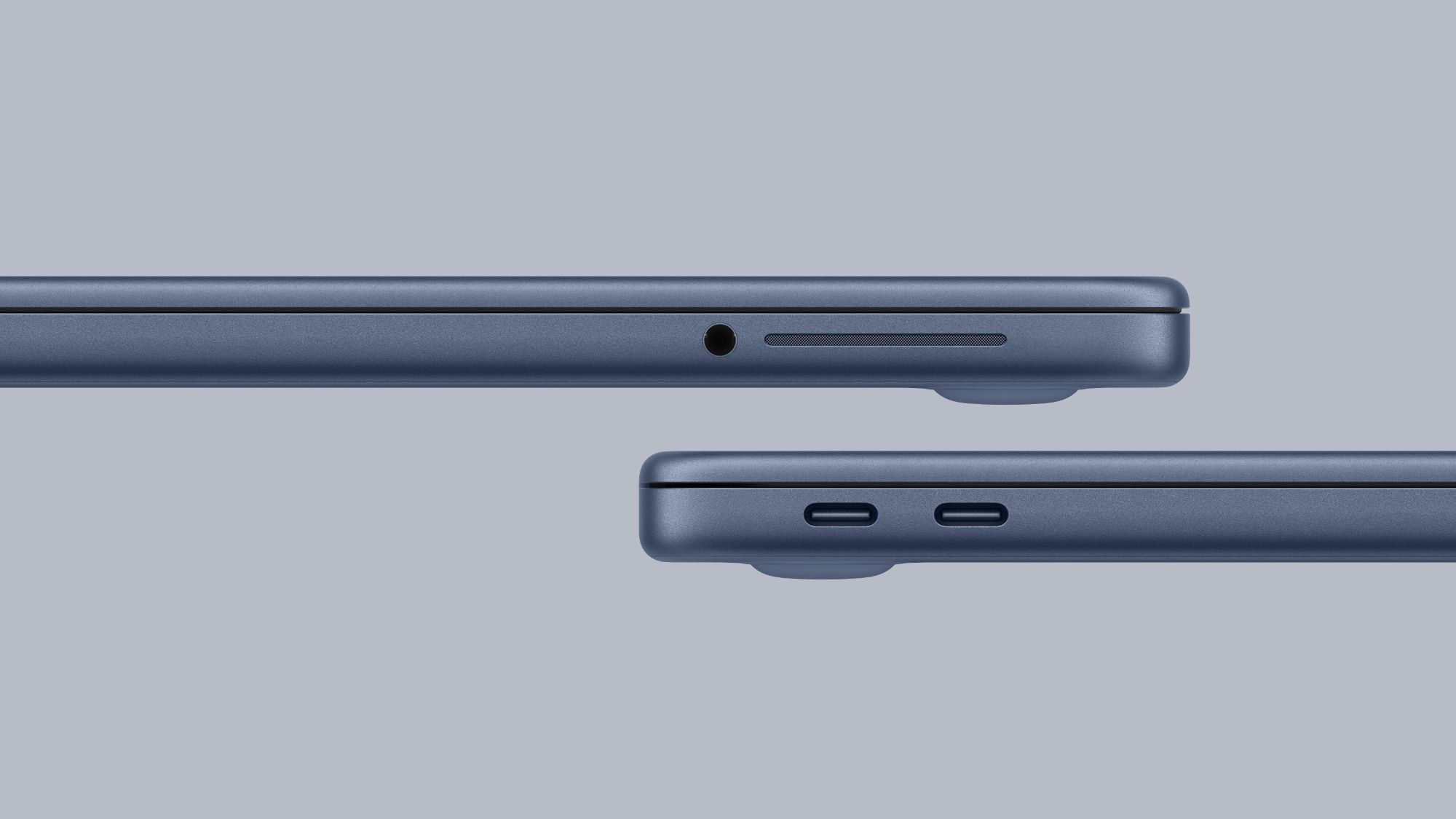

Apple's new low-cost MacBook Neo is available for pre-order at $599 ($499 for college students) and launches March 11; it uses the A18 Pro chip and is promoted as up to 50% faster than a competing Intel Core Ultra 5 PC for everyday tasks and up to 3x faster for on‑device AI workloads. The model has two physically identical USB‑C ports with different capabilities: the left port supports USB 3 speeds (up to 10 Gb/s) and external displays (one 4K@60Hz), while the right port is limited to USB 2 (480 Mb/s); macOS will alert users if they plug a display into the wrong port. The asymmetric port limitation is a minor usability compromise that could affect accessory demand, but the device's pricing and iPhone-chip strategy may influence Apple's competitive positioning in the low‑cost laptop segment.

Market structure: The MacBook Neo at $599 creates a new low-cost Mac tier that benefits AAPL (better share gains in education/consumer segments) and its foundry partners while pressuring traditional Windows OEMs and Intel (incumbent CPU vendor for cheap laptops). Expect modest share shifts: 3–7% of entry-level Windows laptop demand could reallocate to macOS in 12 months if sell-through matches channels, compressing PC OEM volumes and Intel client CPU revenue. Cross-asset: modest risk-on for equities if adoption surprises, slight downward pressure on Intel equity and modest IV compression in AAPL options post-launch; macro FX and commodity impacts are negligible short-term.

Risk assessment: Tail risks include supply constraints at TSMC for A18 Pro (production bottleneck), a product quality or returns spike driven by UX limits (e.g., asymmetric USB-C port), or regulatory pushback on vertically integrated modem/chip usage. Timeline: immediate (days) — preorder sentiment and retail traffic; short-term (weeks/months) — channel sell-through and margins reported in next quarterly cycle; long-term (4+ quarters) — platform migration and ASP mix impact. Hidden dependency: success hinges on A-series capacity allocation and accessory/ecosystem compatibility (hubs, displays).

Trade implications: Direct: bias overweight AAPL (2–3% portfolio) for a 3–12 month window to capture share shift and services upside; underweight/short INTC (~0.8–1%) as secular PC share loss accelerant. Options: implement a 3–6 month AAPL bull call spread sized to ~1% notional to control downside; buy 3–6 month INTC puts (10–15% OTM) as inexpensive asymmetric hedge. Entry: act within 7–21 days of launch and trim on +10–15% moves or after the next earnings report.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.10

Ticker Sentiment

Contrarian angles: Consensus may understate margin erosion — lower-price Macs can grow unit share but lower ASPs could mute gross-margin upside, so upside is demand-driven not margin-guaranteed. The port limitation/feature compromises could produce higher returns or NPS damage than headlines imply, transiently pressuring sentiment; alternatively, history (e.g., iPhone SE) shows lower-cost Apple SKUs can expand the base and raise lifetime revenue per user over 12–24 months. Monitor retail sell-through and return rates for early read-throughs.