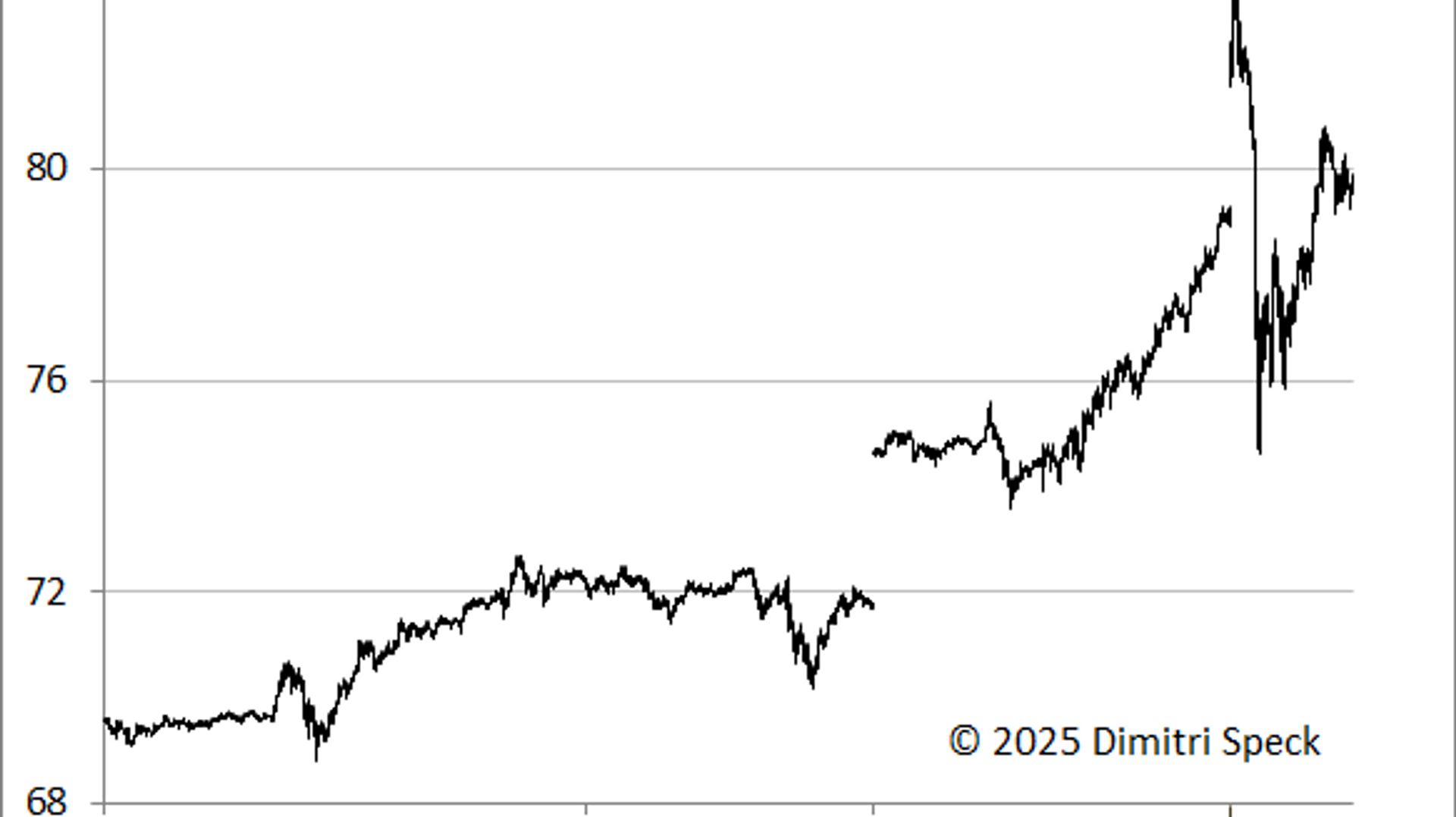

Silver was one of 2025's top performers, gaining 148% in USD (118% in EUR) and finishing the year at $71.50/oz after a December surge of 25%; intra-year highs reached ~$84/oz (and ~$89/oz in China). A near 10% drop on Dec 29 within just over an hour during thin early-Australian futures trading—accompanied by unusually high volume—raises strong suspicions of deliberate price suppression similar to past manipulations; coupled with tight physical availability (elevated lease rates), heavy Chinese demand and continued central-bank purchases, the piece signals heightened upside potential for precious metals but elevated short-term volatility and regulatory/legal risk.

Market structure: The late‑Dec flash decline highlights asymmetry between physical tightness and paper liquidity — winners are physical holders, SIVR/SLV owners and silver‑levered miners (PAAS, HL, AG) who gain operational gearing; losers are short‑term futures sellers, leveraged paper shorts and exposed bullion banks (JPM, DB) facing legal/regulatory tail risk. Higher lease rates and China premiums signal a real physical squeeze; production response is slow (12–36 months), so price signals will be persistent if demand continues. Risk assessment: Immediate (days) risk = intraday flash crashes and margin‑call cascades; short term (weeks–months) risk = regulatory/intervention events (exchange halts, probe announcements) that can remove liquidity; long term (quarters–years) bias = structural upside driven by high global debt and central bank gold purchases, pushing investors into precious metals. Hidden dependencies include Chinese retail and industrial demand, COMEX registered inventory trends and lease rates; monitor these as leading indicators. Trade implications: Favor asymmetric, defined‑risk longs: physical via SIVR, and selective miners (PAAS, HL, WPM) sized to 1–3% NAV with protective puts or call‑spreads to limit drawdown. Options are preferable near‑term (buy 3–6 month 25‑delta calls or defined call spreads around $75–$100 silver strikes) to capture volatility and limit tail losses; avoid naked shorting of bullion banks — prefer event hedges (puts) if holding bank exposure. Contrarian angles: Consensus focuses on manipulation and fear of a repeat 2011 collapse — it underestimates current physical shortages and Chinese buy-side depth; suppression may be tactical, not structural. If COMEX inventories continue to fall and Chinese premiums persist, silver could re-test $100+ within 12–24 months; conversely, short‑term liquidation can open high‑conviction entry points for medium/long investors.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

0.05

Ticker Sentiment