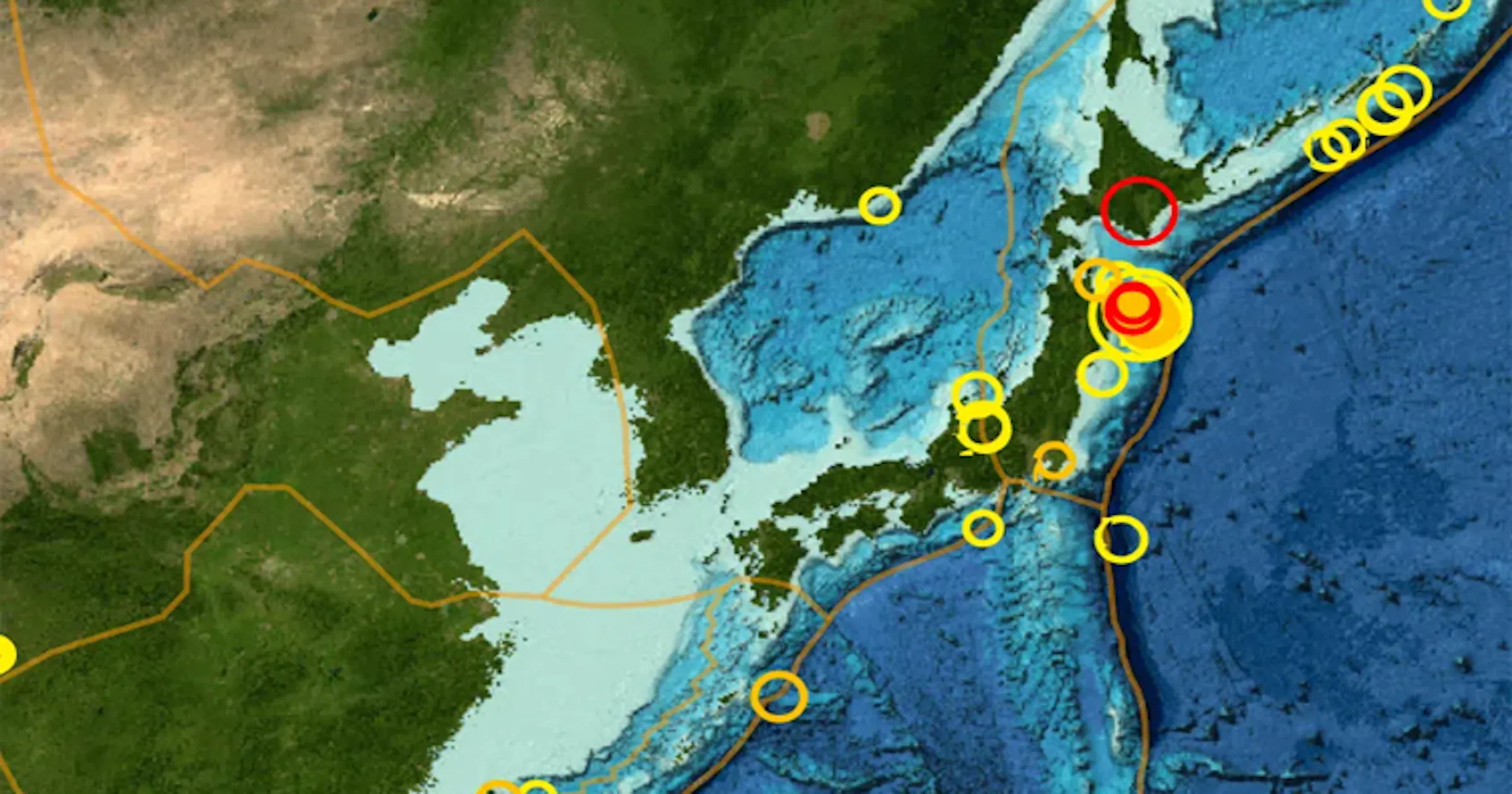

A 6.2-magnitude earthquake struck southern Hokkaido at 5:23 am local time at a depth of 83 km, with no tsunami alert issued and U.S. Geological Survey saying property damage and life threat were likely minimal. However, Japan's meteorological agency warned of elevated risks of falling rocks, landslides, and additional similar-sized quakes over the coming week. The event follows a 7.7 quake off northern Iwate less than a week ago that injured six people and triggered 80-cm tsunami waves.

This is more of a volatility event than a direct macro shock, but the market should still think through second-order infrastructure and logistics exposure. The immediate equity beneficiaries are likely to be the usual disaster-response complex: contractors with heavy earthmoving, inspection, temporary power, telecom repair, and rail/road remediation capability. Japan tends to mobilize quickly, so the biggest tradable edge is not the quake headline itself but the follow-through in procurement and outage remediation over the next 1-3 weeks.

The more interesting risk is not acute casualties; it is the clustering of seismic events raising the probability of precautionary shutdowns, rolling transport delays, and localized supply interruptions across northern Japan. Even when physical damage is limited, inspection-induced downtime can hit automotive, industrial, and electronics supply chains because Japanese manufacturers are high-utilization and low-inventory. That creates a short-duration but potentially high-beta earnings hit for firms with just-in-time exposure, especially if insurers, logistics operators, and port/rail capacity get temporarily constrained.

A second-order effect is sentiment: repeated quakes can keep domestic households more cautious, delaying discretionary spend and travel bookings in affected regions for several weeks. The contrarian point is that the market may overprice a “Japan disaster” narrative when the more probable outcome is a series of manageable disruptions rather than a systemwide economic hit. That argues for fading any broad Japan equity underperformance after the initial shock, while remaining tactically bearish on names with direct exposure to industrial downtime and maintenance bottlenecks.

The key catalyst window is the next 7-10 days, when aftershock risk remains elevated and local authorities may tighten transport or access restrictions. If no material damage emerges, the trade should mean-revert quickly; if seismic activity persists, the downside moves from headline-driven to operational, which is when supply-chain-sensitive names can de-rate faster than the index.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.35