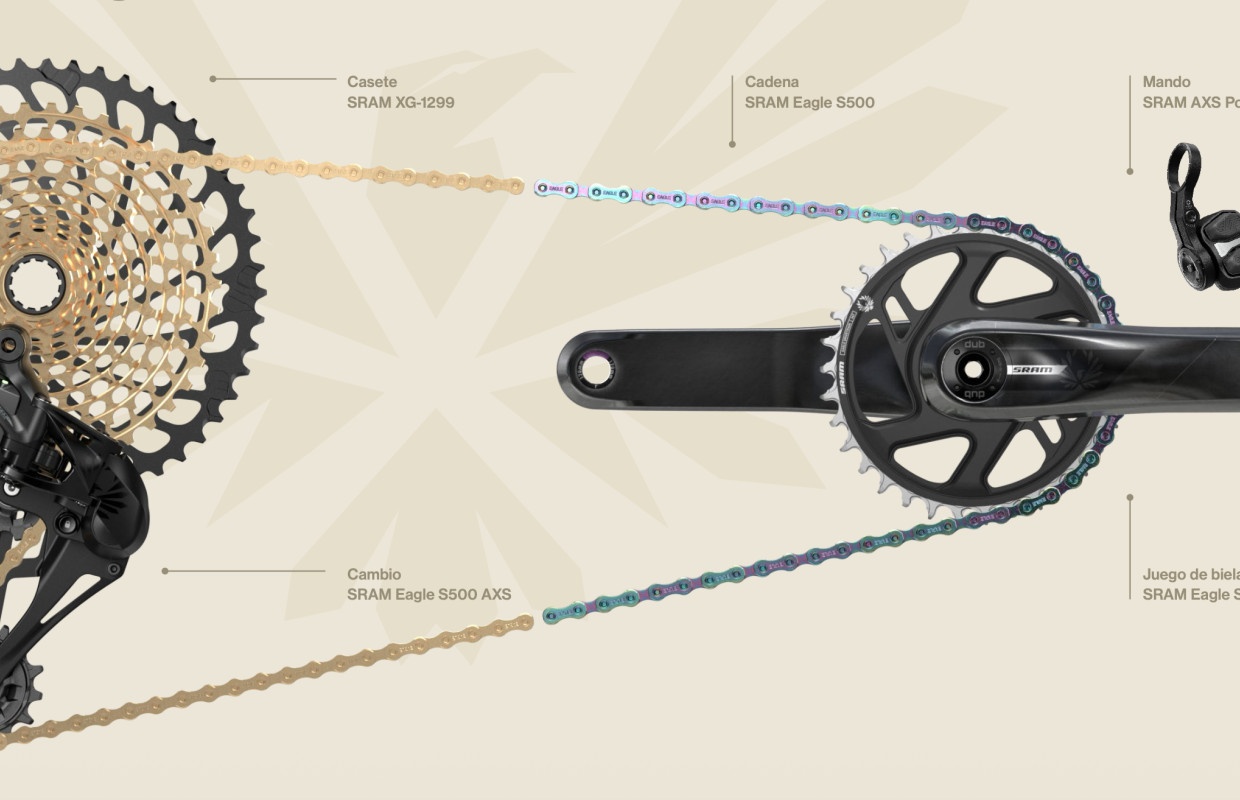

SRAM is restructuring its Eagle lineup into three tiers—S100, S200, and S500 AXS—while introducing a new Half Mount rear-derailleur attachment aimed at improving durability and compatibility. The update adds broader compatibility across the Eagle ecosystem, new crank lengths down to 155 mm, and lower-cost entry pricing starting at €75 for a rear derailleur and €35 for a chain or shifter. The news is constructive for SRAM’s product portfolio but is likely to have limited near-term market impact.

This is a classic monetization-and-tiering move: the company is collapsing SKU sprawl while pushing the ecosystem toward higher-margin attachment points. The important second-order effect is not just pricing power, but channel efficiency — fewer confusing options should reduce dealer inventory risk, improve sell-through, and make upgrade conversations easier at the point of sale. That matters because cycling demand is soft; in a slow market, simplification can protect share even if it does not generate immediate unit growth.

The most relevant competitive implication is that the entry-level and mid-tier mechanical market is being reframed around durability and compatibility rather than pure specification chasing. That can pressure Shimano at the value end if SRAM’s messaging converts into fewer warranty claims and lower service friction, especially in e-MTB where ride abuse is high and maintenance sensitivity is acute. The half-mount concept is also strategically smart: it borrows the anti-flex benefits of more premium architectures without forcing a full platform overhaul, which lowers adoption friction for OEMs that are not ready to standardize on Transmission.

Near term, this should be modestly favorable for mix, but the upside is capped because the new lineup likely cannibalizes some higher-end mechanical demand before it expands total ecosystem share. The bigger catalyst is OEM spec-in over the next 2-3 build cycles; if the new mount becomes a de facto standard on UDH frames, it can create a multi-quarter replacement tail in derailleurs, cassettes, chains, and shifters. The main risk is that the market treats this as incremental rather than transformative, in which case margin expansion may be slower than bulls expect.

The contrarian view is that the simplification itself signals maturity, not acceleration: when a company narrows the catalog, it is often optimizing the base rather than opening a new demand frontier. If UDH adoption plateaus or OEMs stick with existing inventory, the revenue lift could be limited to mix, with little unit growth. So the right read is selective bullishness on ecosystem stickiness, not broad-based top-line enthusiasm.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment