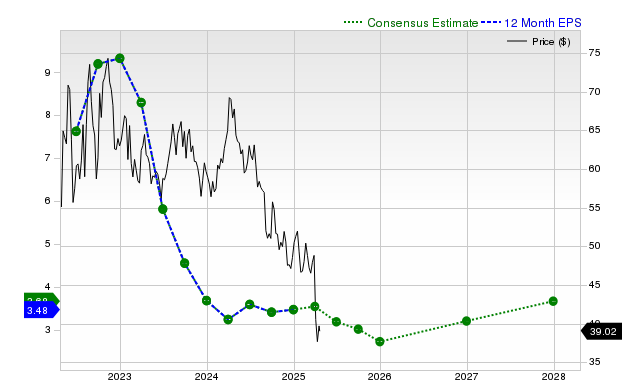

Occidental Petroleum faces meaningful near‑term earnings pressure: Zacks' consensus expects Q EPS of $0.42 (‑47.5% YoY) with the 30‑day estimate down 18.4%; the current fiscal year EPS consensus is $2.22 (‑35.8% YoY) and next fiscal year $1.50 (‑32.4%). Revenue estimates show declines as well (current quarter consensus $6.24B, ‑8.7% YoY; last reported quarter revenue $6.72B, ‑6.1% YoY), although the most recent quarter produced an EPS beat ($0.64 vs $1.00 a year ago; EPS surprise +33.3%). Zacks assigns a Rank #3 (Hold) and a Value Style Score of A, signaling the stock may trade at a discount to peers but is expected to perform in line with the broader market.

Market structure: Occidental (OXY) is a high-beta beneficiary of any sustained oil rally — material upside if WTI > $75/bbl for 30+ days — while weaker near-term earnings and revenue guidance (consensus FY EPS -35.8%) compress prices for cyclicals and higher-leverage E&Ps. Integrated majors (XOM, CVX) see relative pressure on free-cash-flow multiples if OXY’s valuation discount narrows, but they retain structural pricing power via downstream margins. Cross-asset: a rally in oil would tighten energy credit spreads (supporting corporate bonds), lift commodity FX for CAD/NOK, and raise options IV in energy names by 25-50% over current baselines. Risk assessment: Tail risks include a >30% oil shock to the downside within 6 months (macro recession), regulatory carbon/tax actions that raise capex costs, or an OXY covenant/debt re-pricing event given legacy leverage — any would gap spreads by 200–400bps. Time horizons: expect knee-jerk moves in days around earnings/estimates, directional repositioning over 1–3 months as oil price signals change, and credit/deleveraging outcomes over 6–24 months. Hidden dependencies: hedge book, asset sales pace, and capital-allocation choices (debt paydown vs buybacks) dominate upside capture. Trade implications: Tactical overweight energy via OXY but size and protection matter; volatility makes options advantageous. Pair trades (long OXY / short XOM) isolate commodity beta vs capital-allocation alpha. Income strategies (covered calls) work if you expect range-bound moves; directional call buys reward an oil-driven re-rating. Contrarian angles: Consensus places too much weight on near-term EPS downgrades and not enough on potential FCF upside if WTI sustains >$80 and OXY keeps cost structure intact — valuation (Zacks Value A) implies mispricing. The market may be under-pricing balance-sheet repair optionality; conversely, if management prioritizes buybacks over deleveraging, downside is underappreciated. Watch for historical rebound patterns (2016–2018 energy snapbacks) as a playbook, but require concrete catalysts (30-day WTI > $75 or two consecutive quarters of EPS beats).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.25

Ticker Sentiment