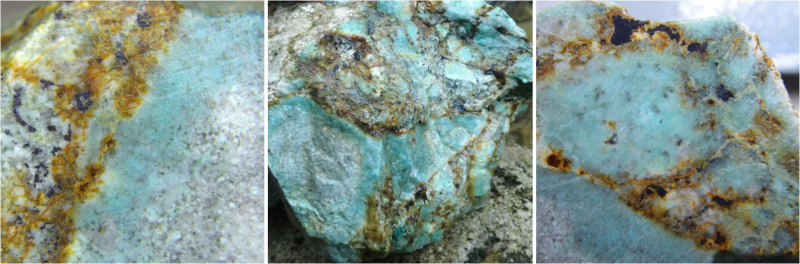

Andina Copper has restarted and advanced its 2025–2026 exploration campaign at the Cobrasco project in Chocó, Colombia, completing roughly 2,275 m of diamond drilling to date (continuation of CDH003 to 774.8 m plus CDH004 at 900.25 m and CDH005 ~700–900 m) and expects assays shortly. Historic drilling by Rugby returned long porphyry-style intervals including CDH001: 808 m @ 0.42% Cu, CDH002: 754 m @ 0.46% Cu and CDH003: 144.6 m @ 0.69% Cu with higher-grade internal zones; surface sampling in Cobrasco East yielded stream anomalies up to 245 ppm Cu and float up to 0.71% Cu. Ongoing geophysical (AirMT, IP) and drone LiDAR surveys aim to vector additional targets, making imminent assay releases and follow-up drilling the primary near-term catalysts for the company’s equity.

Market structure: A positive assay campaign at Cobrasco materially benefits Andina Copper (PMMCF) and local Colombian service providers (drillers, geophysics) by rerating a small-cap explorer; large producers (FCX, SCCO) see little immediate supply impact because any deposit build-out is multiyear and likely <0.5–1.0% of annual global copper supply. Copper price sensitivity will be to confirmation of long, consistent grades (e.g., >0.4% Cu over hundreds of metres); a confirmed porphyry-style system could lift junior explorer valuations and implied vol in miner equities/options for 3–12 months. Cross-asset: modest tightening in EM credit spreads for Colombia is possible on a sustained sector rally; short-dated copper options and miner equity vol will rise around assay and geophysics releases. Risk assessment: Key tail risks are social/permitting conflict in Chocó, metallurgical/recovery failure, and equity dilution (typical for juniors) — each can collapse value >70%. Time horizons: immediate (days) — assays; short (weeks–months) — AirMT/IP results, financing; long (years) — resource definition and permitting. Hidden dependencies: float samples in Cobrasco East must be tied to in-situ sources (geochronology required) or upside is speculative; positive assays will almost certainly trigger a financing round that will dilute existing shareholders. Trade implications: Tactical speculative allocation (small size) ahead of assays is justified; use strict risk controls (stop-loss, sizing). If assays confirm sustained >0.5% Cu over >200 m, increase exposure and consider levering via copper call spreads on larger names (FCX) or direct LME/HG call options for a cleaner play on metal price. Avoid levering into development risk; prefer buying equity now only as a discovery binary and hedge metal-price exposure with options. Contrarian angles: The market can overreact positively to initial high-grade intersections — historical parallels (early porphyry juniors) show volatile 2–6x pops followed by 30–70% drawdowns on dilution or negative metallurgy. Consensus misses the probability of non-economic continuity at depth; therefore scale into wins and scale out first 30–50% of gains. Unintended consequence: extensive LiDAR/geophysics may accelerate environmental scrutiny and community pushback, delaying development and compressing IRR.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment