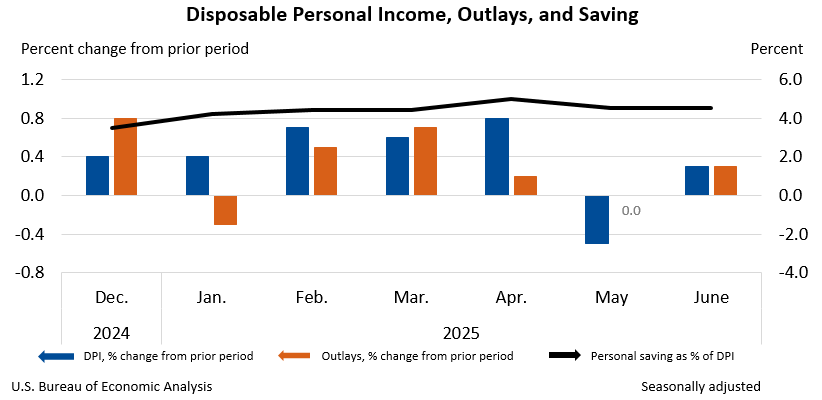

U.S. personal income, disposable personal income, and personal consumption expenditures each increased by 0.3% in June 2025, signaling modest economic growth. The personal saving rate stood at 4.5%. Notably, the PCE price index rose 0.3% monthly, while the annual rate reached 2.6% (headline) and 2.8% (core), indicating persistent inflation above the Federal Reserve's 2% target despite the moderate pace of spending.

The June 2025 Personal Income and Outlays report indicates a US economy characterized by modest nominal growth but persistent inflationary pressures that are eroding real gains. While personal income and personal consumption expenditures (PCE) both rose by 0.3% in current dollars, the inflation-adjusted figures reveal a more strained consumer: real disposable personal income was flat at 0.0%, and real PCE grew by a marginal 0.1%. This suggests that nearly all nominal income growth was absorbed by rising prices. The key concern for markets is the inflation data, with the core PCE price index, the Federal Reserve's preferred gauge, increasing 0.3% month-over-month and 2.8% year-over-year. This annual rate remains significantly above the Fed's 2% target, signaling that underlying price pressures are not abating as quickly as desired. Furthermore, the source of income growth, led by government social benefits and government wages rather than robust private sector salary increases, points to a potential vulnerability in the foundation of consumer financial health. The personal saving rate of 4.5% provides a limited cushion, indicating consumers are not aggressively drawing down savings to fund consumption.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.05