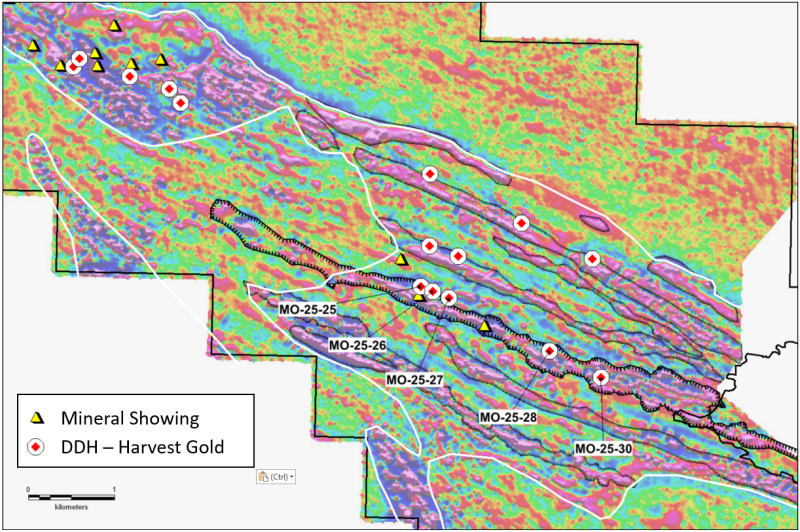

Harvest Gold reported high-grade exploration results from the central Mosseau Property, hitting 105.0 g/t Au over 1.15 m (MO-25-25) including visible gold, with associated 4.3 g/t Ag and 464 ppm Cu and a surrounding lower-grade halo (0.32 g/t Au over 6.9 m). Other notable intersections include MO-25-26 (0.50 g/t Au over 16.35 m, incl. 1.85 g/t over 1.5 m with 700 ppm Cu) and MO-25-27 (0.76 g/t over 5.85 m, incl. 2.11 g/t over 1.0 m with 466 ppm Cu); the Kiask River corridor is traceable for ~3 km, up to 16 m wide and shallowly tested to ~100 m, with follow-up drilling planned. Results are subject to true-width determination, historical-data caveats and standard QA/QC; positive assays could materially re-rate the junior explorer but remain early-stage exploration news.

Market Structure: Harvest Gold (HVG/HVGDF) is the direct beneficiary—news of a 105 g/t visible-gold intercept inside a 3 km shallow, 10+ km-traceable corridor should re-rate a junior explorer’s optionality, attract financings, service contractors and nearby prospectors; impact on global gold supply or majors (GFI) is immaterial. Pricing power shifts are idiosyncratic: expect HVGDF volatility and localized capital flows into Canadian juniors, modest supportive pressure on spot gold (basis points) and CAD, negligible effect on sovereign bonds. Risk Assessment: Key tail risks are nugget-effect grade variability (high coefficient of variation), metallurgy/permitting setbacks, Indigenous/land access challenge, and mandatory dilutive financings; low-probability/high-impact outcomes include a failed metallurgy test or an adverse consultation ruling that stalls project (6–24 months). Time horizons: immediate (days) = news-driven spike and volume; short-term (weeks–months) = assay follow-ups and financing terms reveal; long-term (12–36 months) = resource delineation, metallurgy, JV/M&A decisions. Catalysts: next 10 hole assays, a maiden resource, metallurgy labs, and any JV/LOI with a major (e.g., GFI) will rapidly re-price valuation. Trade Implications: Tactical long in HVGDF as a high-risk spec play, hedged and size-limited; volatility will compress once follow-up assays confirm continuity. Use options where liquid: buy 3–6 month call spreads to cap premium; if options are illiquid, use small cash positions (2–3% portfolio) with a 40% stop and a 100% + target within 6–12 months contingent on resource progress. Consider a pair: long HVGDF (3% notional) vs short VIORF (1–2% notional) to isolate company-specific upside vs regional legacy risk. Contrarian Angles: The market may over-react to a single visible-gold intercept—expect mean reversion if subsequent holes average <0.3 g/t over meaningful widths; conversely the market may under-price the 10+ km corridor potential if continuity proves real, creating outsized M&A optionality. Watch for dilution: >C$5–10M financing rounds at sub-$0.10-equivalent share prices would materially change upside; set clear stop-triggers tied to assay averages and announced financing terms.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment