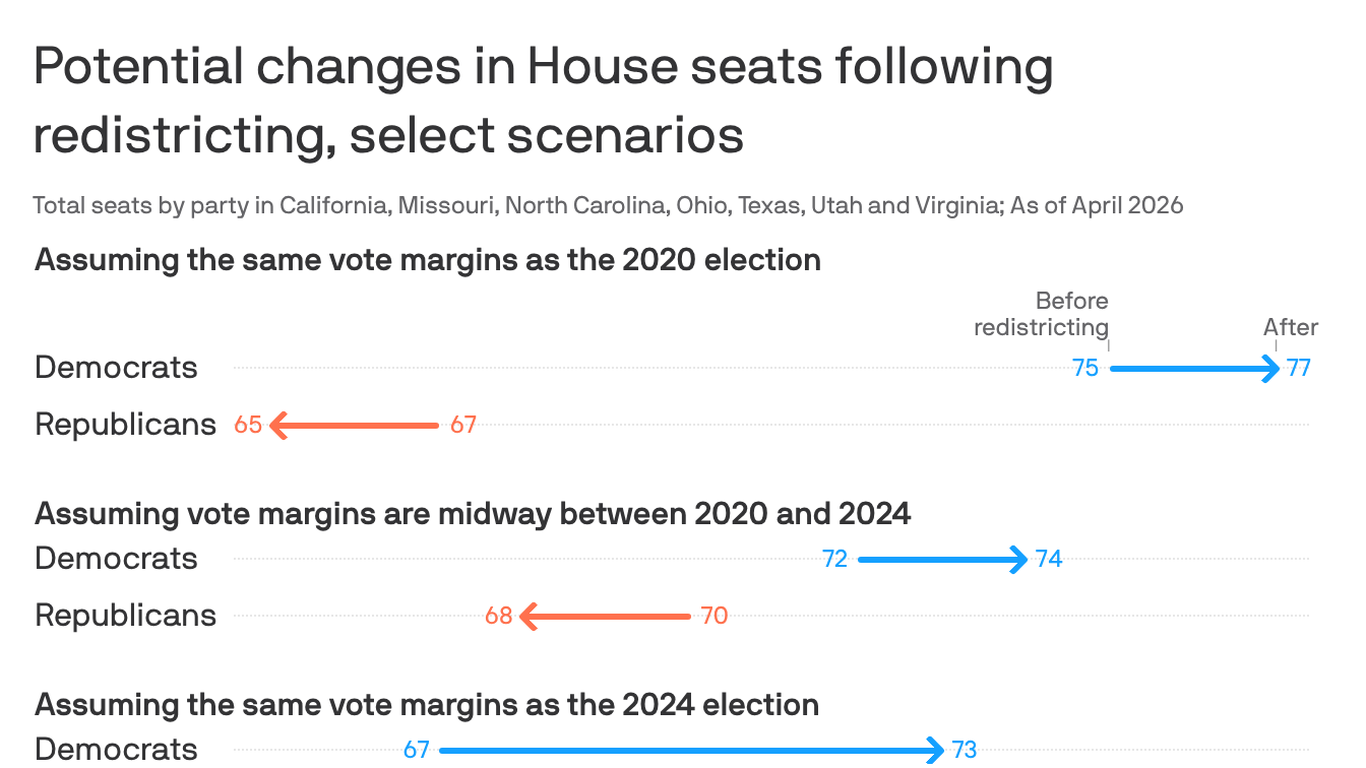

Republicans are now favored in fewer House seats after the mid-decade redistricting push, with Axios estimating Harris would have carried six more seats under the new maps based on 2024 results. Virginia's new map could shift the delegation from 6–5 to 10–1 for Democrats, while Florida remains the last major battleground and the Supreme Court could affect challenges to racially discriminatory maps. The article is politically significant but has limited direct market impact.

The market implication is not the headline partisan shift itself, but the growing probability that House composition becomes structurally less predictable in the next two cycles. That raises the value of campaign-related microcaps, ballot-access infrastructure, and any businesses with high exposure to state-level political contracting, because more competitive seats increase spend intensity and shorten planning cycles. The second-order effect is that incumbents in both parties will tilt further toward hard-base fundraising, which tends to accelerate digital ad, donor CRM, and polling demand into the next 12–18 months.

The bigger risk is legislative volatility, not the immediate map math. If courts narrow challenges to discriminatory maps, the practical window for redistricting closes quickly, which would lock in the current advantage set and reduce the odds of a late-cycle reversal; if courts delay or strike down key maps, the seat outlook can swing materially before filing deadlines. That means the catalyst path is binary and time-sensitive over days to weeks, while the portfolio-level impact is more durable over the 2026 cycle than the 2024/2025 news flow.

Consensus is likely underestimating how little of this translates into clean, tradable alpha for the broad market. The more likely mispricing is in local TV, political media, and data vendors where investors assume redistricting automatically means more ad dollars everywhere; in reality, a more polarized map can concentrate spend in a smaller set of districts while starving the rest. Conversely, if the map changes fail to produce enough genuinely competitive seats, the incremental spending impulse may be overestimated and reverse after the current news cycle fades.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.10