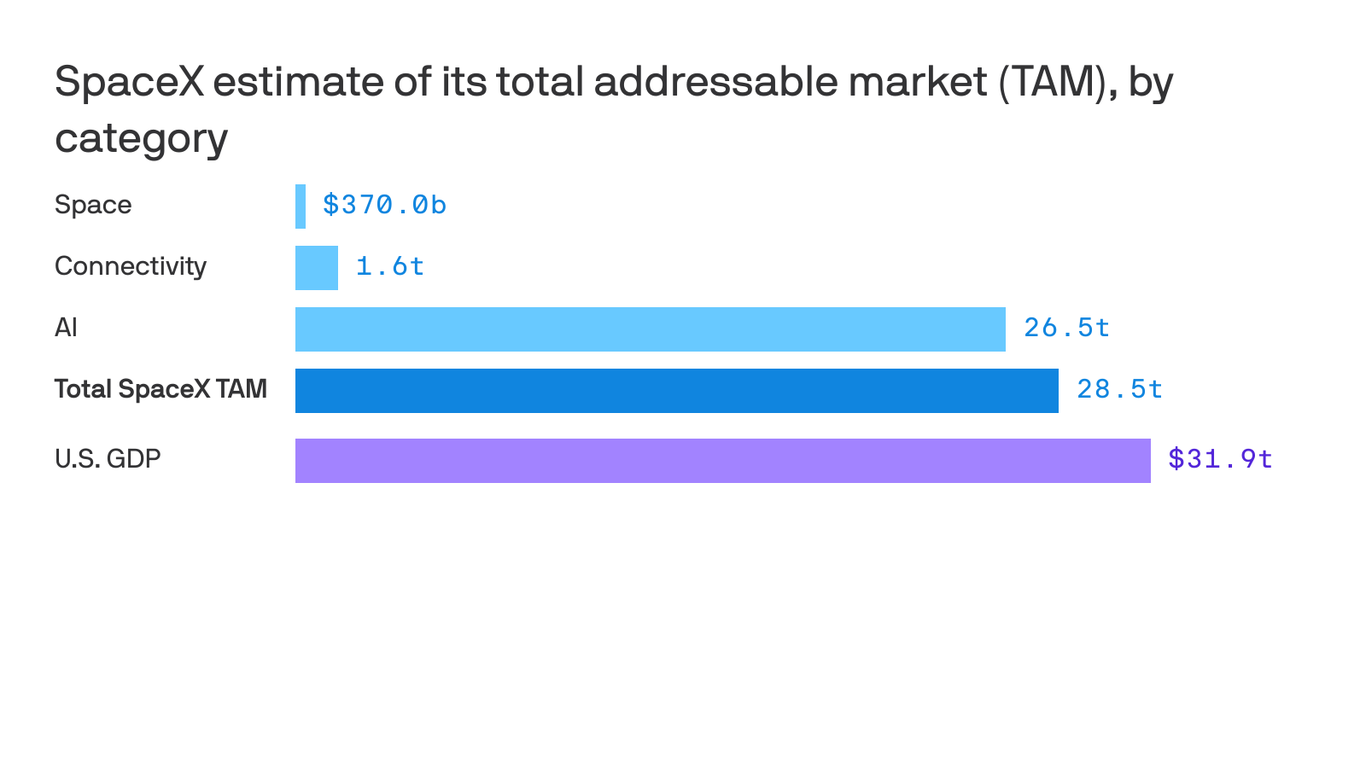

SpaceX disclosed a $28.5 trillion total addressable market in its prospectus, including an estimated $26.5 trillion AI opportunity and additional space and connectivity markets. The filing is highly optimistic and likely designed to frame long-term growth potential rather than near-term fundamentals, with commentary in the article calling the estimate 'farcical.' The news is more notable for sentiment and IPO positioning than for immediate market impact.

The market is treating this as a disclosure oddity, but the more important signal is strategic: SpaceX is using an extreme TAM narrative to justify a capital allocation regime that can absorb massive upfront spend in exchange for option value. That has second-order implications for adjacent winners: any capital-light infrastructure tied to launch, satellite distribution, edge AI inference, and enterprise connectivity should see a higher scarcity premium if investors start to believe the addressable spend is being pulled forward rather than merely advertised. The key competitive dynamic is not whether the headline TAM is credible, but whether it changes financing conditions across the private-market stack. If SpaceX can sustain the perception that it owns the default platform for orbital connectivity and AI-enabled infrastructure, smaller satellite and aerospace peers may face a higher hurdle rate for capital and customer acquisition, especially in the next 12-24 months when buyers prefer the perceived survivability of the category leader. That is mildly negative for lower-quality public comps and for venture-backed second-tier names that rely on narrative to bridge to scale. The contrarian read is that the exaggerated TAM itself may be bearish for the stock in the short run if it invites skepticism around governance and disclosure discipline, but that skepticism can coexist with long-duration upside if the company keeps converting frontier rhetoric into real revenue. The best setup is to fade the most promotional second-order beneficiaries and own the infrastructure pick-and-shovel winners, not to short the platform outright. The strongest reversal catalyst would be any evidence that the market is smaller, more regulated, or more capital intensive than implied, which would compress private-market multiples over the next 6-18 months rather than days.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

neutral

Sentiment Score

0.15

Ticker Sentiment