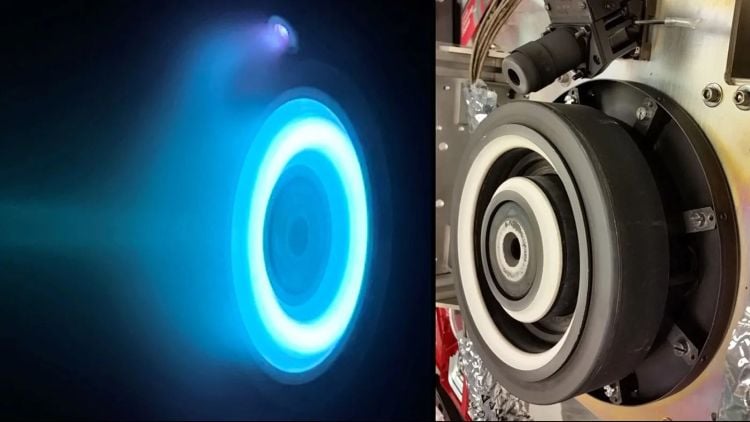

NASA tested a next-generation electric propulsion system at 120 kilowatts, a new U.S. record and roughly 25 times the power of the Psyche spacecraft's electric thrusters. The system is aimed at future human Mars missions and could reduce fuel use by up to 90%, but a crewed Mars transit would still require 2 to 4 megawatts and more than 23,000 hours of operation. The article is largely a technology milestone with long-dated implications rather than an immediate market catalyst.

This is less a near-term aerospace trade than a validation event for a very long-duration infrastructure cycle. The important second-order signal is that deep-space propulsion is shifting from “exotic science project” to an engineering scaling problem, which tends to favor suppliers of power electronics, thermal management, radiation-hard controls, and high-spec materials long before it benefits any prime contractor revenue line. The first monetizable winners are likely not launch names but the picks-and-shovels layer: components that can tolerate extreme heat, high-voltage conversion, and long-life duty cycles.

The bottleneck is now power density, not theoretical efficiency. That creates a multi-year pull-through for nuclear microreactors, high-reliability solar arrays, advanced batteries, and space-grade semiconductors, because 2–4 MW-class systems imply an entire ecosystem of generation, storage, and fault-tolerant control. If this program keeps progressing, the market may begin to price a modest but durable TAM expansion for space infrastructure suppliers, while traditional chemical propulsion vendors face a slow share-of-wallet loss in deep-space missions rather than an abrupt demand cliff.

The contrarian view is that the commerciality timeline is probably too optimistic and the current enthusiasm should fade after the headline cycle. Human Mars transport is a decades problem, and the near-term procurement budget likely remains dominated by legacy systems, ISR, launch cadence, and LEO infrastructure. That means the right expression is not to chase pure-play Mars narratives, but to own enabling technologies that also win on Earth across grid, defense, and industrial applications.

Catalyst-wise, expect incremental rather than binary upside: additional ground-test milestones, higher-power demonstrations, and eventual contracts tied to lunar logistics or cislunar power. Any slip in thermal durability, contamination control from the propellant chemistry, or cost overruns in power generation could push the payoff horizon out by 3–5 years, which would compress enthusiasm in the most speculative names. The risk/reward is best where the technology has dual-use demand and where space upside is a free option rather than the core thesis.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35