Nvidia has reached a $5 trillion market capitalization, fueled by its AI semiconductor leadership and projected revenue growth exceeding $200 billion by 2026, underscored by a $100 billion partnership with OpenAI. However, the company faces increasing margin pressure due to higher manufacturing costs from new facilities and rising competition from major customers developing in-house AI chips, which could lead to price erosion and further compress its recently declining gross and operating margins. Despite strong revenue forecasts, these profitability headwinds, combined with a high trailing P/E ratio of 54.5x, suggest potential earnings growth challenges, leading to a cautious outlook for investors ahead of its Q3 earnings report.

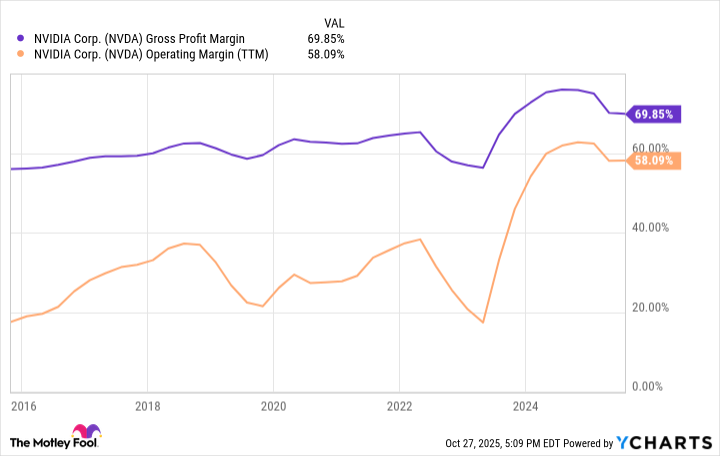

Nvidia has achieved an extraordinary $5 trillion market capitalization, becoming the world's largest company, driven by its pivotal role in the artificial intelligence (AI) revolution. The company's annual revenue has surged to $165 billion, marking a 1,000% increase over the past five years, with projections indicating growth to over $200 billion by 2026, supported by a $100 billion investment and customer relationship deal with OpenAI. This robust top-line expansion is further bolstered by an estimated $550 billion in data center capital expenditures next year, suggesting continued strong demand for its chips. Despite robust revenue forecasts, Nvidia faces increasing pressure on its profitability, with gross margin slipping to 70% and operating margin to 58% over the last twelve months, down from record highs. These declines are partly attributed to higher manufacturing costs associated with chips from Taiwan Semiconductor's Arizona facilities, which may be passed on to Nvidia, impacting its gross margins. The competitive landscape is intensifying as major customers like Amazon and Alphabet develop their own custom AI chips (Trainium and TPUs), potentially leading to price erosion for Nvidia's premium products. This increased competition could further compress operating margins, possibly returning them to historical levels of 30%-40%. With a trailing price-to-earnings (P/E) ratio of 54.5x, Nvidia is the most expensive megacap technology stock excluding Tesla, implying high future earnings growth expectations that may be challenged by margin compression.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately negative

Sentiment Score

-0.50

Ticker Sentiment