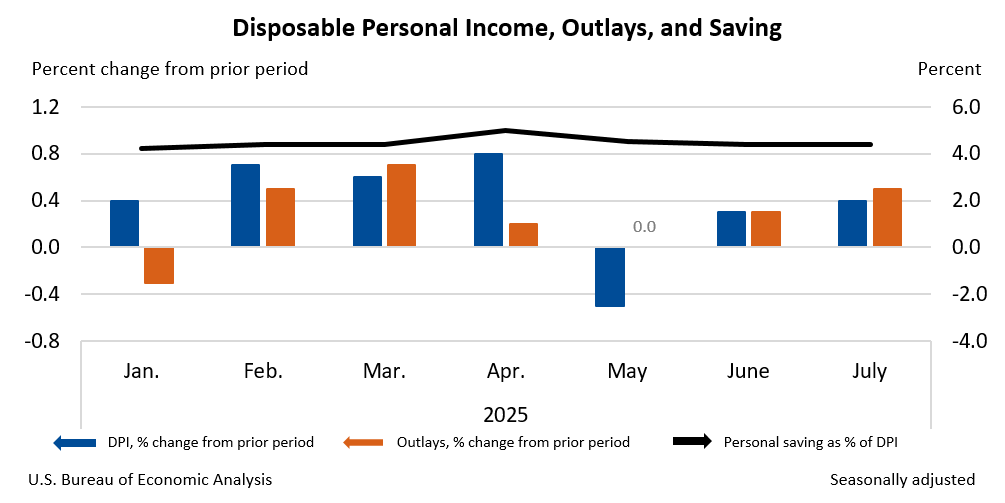

U.S. personal income increased 0.4% in July, primarily driven by higher compensation, while personal consumption expenditures (PCE) rose 0.5%, reflecting broad-based spending growth across both goods and services. The PCE price index advanced 0.2% monthly and 2.6% year-over-year, with the core PCE (excluding food and energy) rising 0.3% monthly and 2.9% annually. These figures indicate continued consumer demand and persistent inflationary pressures that remain above the Federal Reserve's target.

The July 2025 personal income and outlays report indicates a resilient U.S. consumer but with persistent inflationary undercurrents that complicate the outlook for monetary policy. Personal income grew by a solid 0.4%, driven primarily by robust wage and salary growth, yet this was outpaced by a 0.5% increase in personal consumption expenditures (PCE). This divergence, which translates to a 0.3% rise in real PCE, signals strong underlying demand but also resulted in a lower personal saving rate of 4.4%, raising questions about the sustainability of current spending growth. Critically, the inflation data presents a challenge for the Federal Reserve. While the headline PCE price index rose a modest 0.2% month-over-month, the core PCE index, a key policy input, advanced 0.3% monthly and remains elevated at 2.9% year-over-year. This persistent core inflation, coupled with strong consumer spending, suggests the disinflationary process is facing headwinds and keeps pressure on the central bank to maintain its restrictive stance.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.40