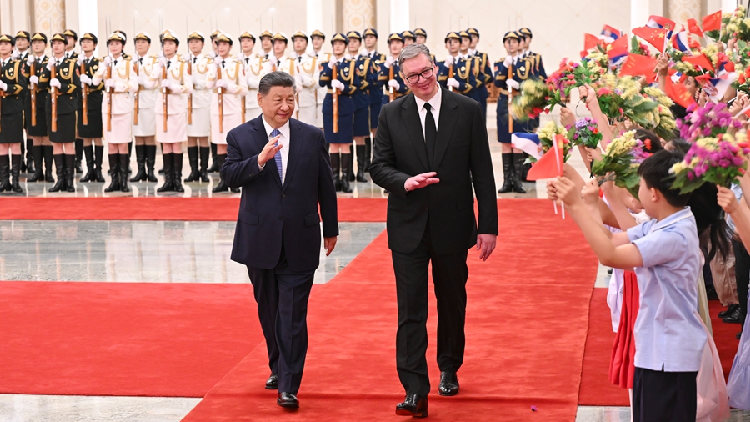

China and Serbia deepened their strategic partnership, highlighting $6.49 billion in bilateral trade in 2025, up 13% year on year. The article cites completed and expanded infrastructure projects, the full inauguration of the Chinese-built Serbian section of the Budapest-Belgrade railway in October 2025, and broadening cooperation into technology, green energy, and AI. Serbia also joined the Group of Friends of China’s GDI and GGI, reinforcing the diplomatic and economic alignment.

This is less about Serbia itself than about Beijing using a small, politically reliable European node to prove the BRI still has deliverable cash-flow assets even as the broader China story faces de-risking pressure. The implication for markets is that China will likely keep funding a narrow set of “showcase corridors” where execution risk is manageable and political optics are high, while softening exposure elsewhere; that favors contractors, rail rolling stock, power equipment, and industrial exporters with already-established local footprints, but not broad EM beta. The second-order effect is on European supply chains and trade routing. A functioning rail/bypass/FTA stack can incrementally divert freight from road and Atlantic maritime routes into China-linked land corridors, which is bullish for inland logistics and customs/warehouse operators, but negative for incumbents reliant on slower, fragmented Balkans logistics. It also reinforces Serbia’s role as a tariff-avoidance and assembly gateway into the EU periphery, which could trigger tighter scrutiny from Brussels and a slower approval process for future Chinese-financed projects across the region. The more interesting read-through is policy optionality: China is pairing infrastructure with trade liberalization and selective tech/AI cooperation, which is a low-capex way to export standards and embed dependence before the West can react. That creates a medium-term opportunity in firms tied to electrification, grid, telecom, and industrial automation where China can win specifications before competitors can re-bid. The risk is that any renewed EU pressure on state-aid, procurement, or security screening could quickly turn these projects into headline risk, especially over the next 6-18 months. Contrarianly, the market may be underestimating how much of this is symbolic rather than scalable. Serbia is not a template for Europe-wide capital deployment; it is a controlled test case. The trade is therefore not a broad long-China trade, but a relative-value expression in names that win on project conversion and lose little if Europe tightens the rules.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.42