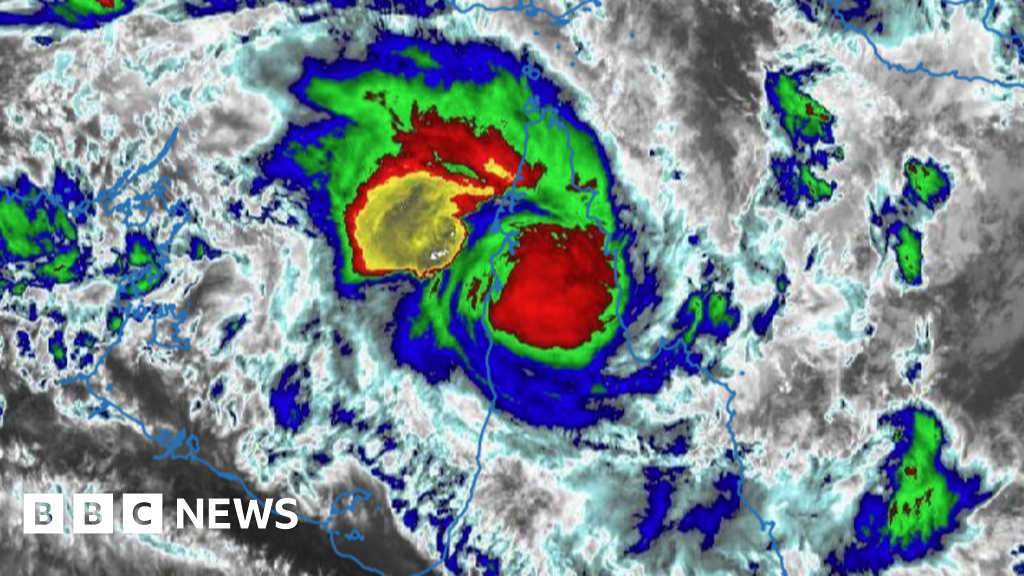

Tropical Cyclone Narelle made landfall on Cape York with peak gusts reported at 220 km/h and has since weakened to a category 3 with gusts around 155 km/h; up to 500 mm of rain is forecast, creating a high flash-flood risk. About 3,500 homes in regional Queensland are without power, small communities (e.g., Coen, pop ~350) report roof losses, and hundreds were evacuated from Numbulwar; Port Douglas and Cairns are experiencing beach erosion. Impacts are concentrated regionally and will pressure local infrastructure, utilities and tourism revenue but are unlikely to move national financial markets.

Immediate market effects will be concentrated in short-term travel demand and localized logistics bottlenecks, but the more durable impact is a 3–12 month uplift in civil works and repair demand that favors contractors and building-materials suppliers with Queensland footprints. Government emergency spending and private rebuilding typically convert into multi-quarter revenue streams for regional contractors; look for municipal and state capital reallocation within 30–90 days that accelerates contractor tender flow.

Insurance bilans are the obvious headline, yet the second-order dynamic is pricing power: repeated small-to-medium events compress capacity and support higher premiums over 12–24 months, benefiting insurers with diversified balance sheets and reinsurer access while pressuring smaller, regionally concentrated underwriters. Conversely, near-term claims administration and loss adjustment will weigh on cash flows for a quarter or two and create volatility around quarterly reporting windows.

Energy and commodity impact is asymmetric and path-dependent: short-lived port or road closures create temporary shipment delays that can spike spot freight and coal/LNG scheduling risk for 1–3 weeks, but sustained intensification over the warm-water Gulf corridor would be the true supply shock that could move Asian spot gas and seaborne coal differentials. Tourism-facing equities will see an immediate demand hit for 1–8 weeks, while coastal real estate and small rental properties endure longer tail risks in valuations if insurance coverage tightens or premiums jump materially.

Catalysts to watch are: state emergency budget announcements (7–21 days), insurer reserve updates (next quarterly filings), contractor tender wins and pipeline awards (1–3 months), and weather-model revisions indicating re-intensification over the Gulf (48–96 hours). Reversals come from rapid government reconstruction funding that outpaces losses, or if reinsurance capital floods back in setting a lower long-term premium trajectory within 6–12 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.35