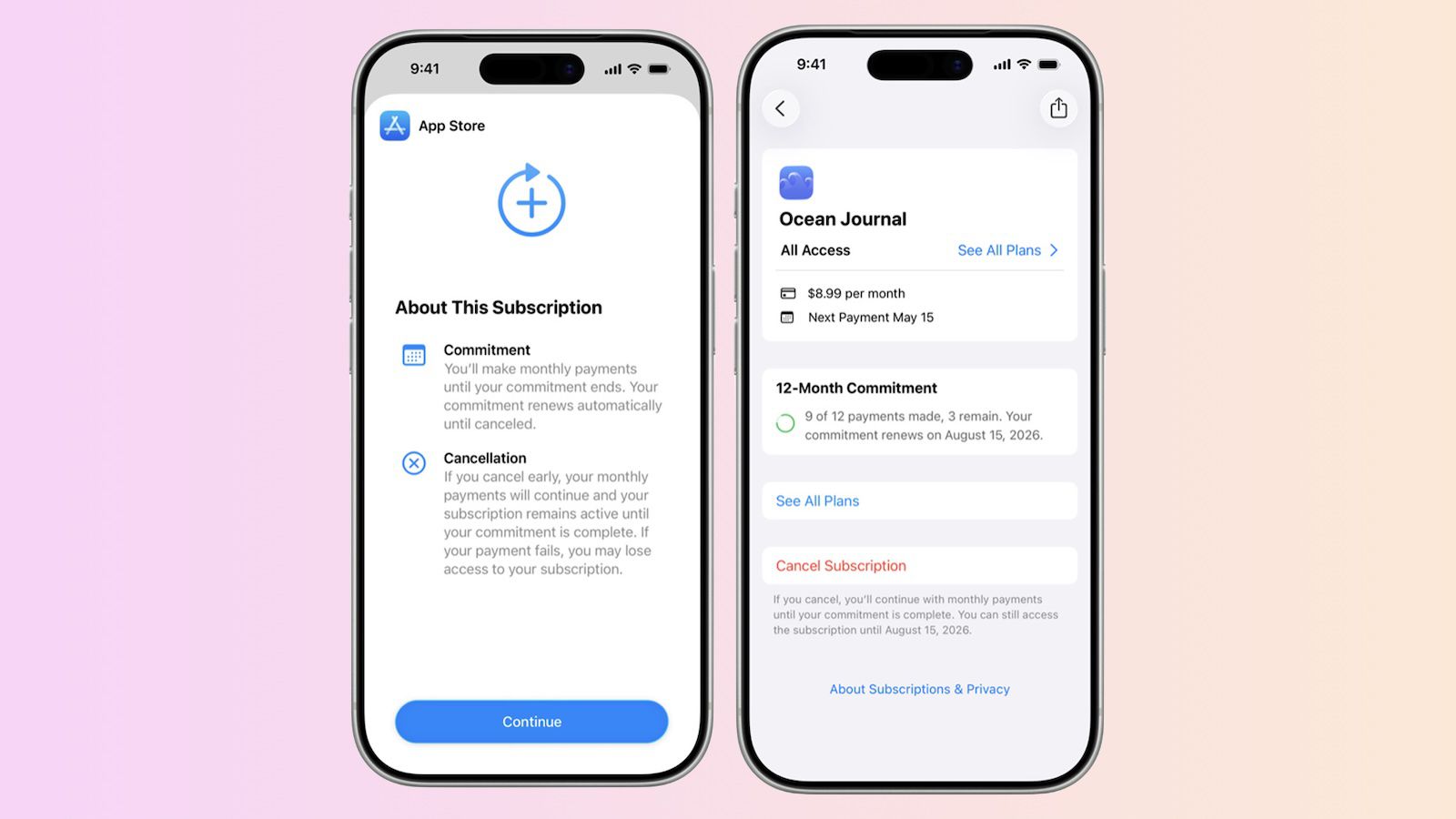

Apple launched a new App Store subscription option for developers: monthly payments with a 12-month commitment, enabling annual-style discounted pricing in smaller installments. The feature is designed to improve affordability and transparency, with payment-progress tracking plus email and optional push notifications before renewals. Developers can start testing today, with rollout planned for iOS 26.4 and equivalent platform updates next month; the U.S. and Singapore appear excluded for now.

This is less about near-term Apple revenue and more about tightening the App Store’s monetization flywheel. By lowering the sticker shock of annual plans while preserving annual economics, Apple is nudging subscription adoption higher among price-sensitive users and improving retention for developers that can’t support a true annual upfront ask. The second-order winner is Apple’s services ecosystem: more successful developer monetization tends to increase App Store take rate durability and reduce churn to off-platform billing alternatives.

The more interesting dynamic is competitive pressure on subscription-heavy software and media companies. Bundling the annual commitment into monthly payments should improve conversion for consumer apps with high first-month drop-off, but it may also cannibalize some annual-prepay cash flow, which matters for smaller developers financing acquisition spend. Over the next 1-2 quarters, this could show up as modestly better gross adds but flatter or even weaker cash collections for app publishers, especially those with ad-driven acquisition and thin working capital.

The exclusion of the U.S. and Singapore is a meaningful tell: Apple is likely testing regulatory, payments, or consumer-protection friction before broader rollout. That lowers immediate impact and suggests this is a gradual policy lever rather than a step-function catalyst for AAPL earnings. If adoption is strong in the initial markets, the real upside is not a direct revenue beat but a higher attach rate across subscriptions, which would incrementally support services growth and App Store resilience into next year.

Consensus may be overestimating the headline positivity for Apple and underestimating the stress on indie developers. This is bullish for the platform owner, but selective for the ecosystem: companies with strong brand, low churn, and flexible billing infrastructure should benefit, while weaker apps may see little improvement if users treat the commitment as a quasi-installment plan rather than true annual lock-in. The tradeable signal is more about relative winners in subscription software and payments than a direct AAPL re-rating.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.15

Ticker Sentiment