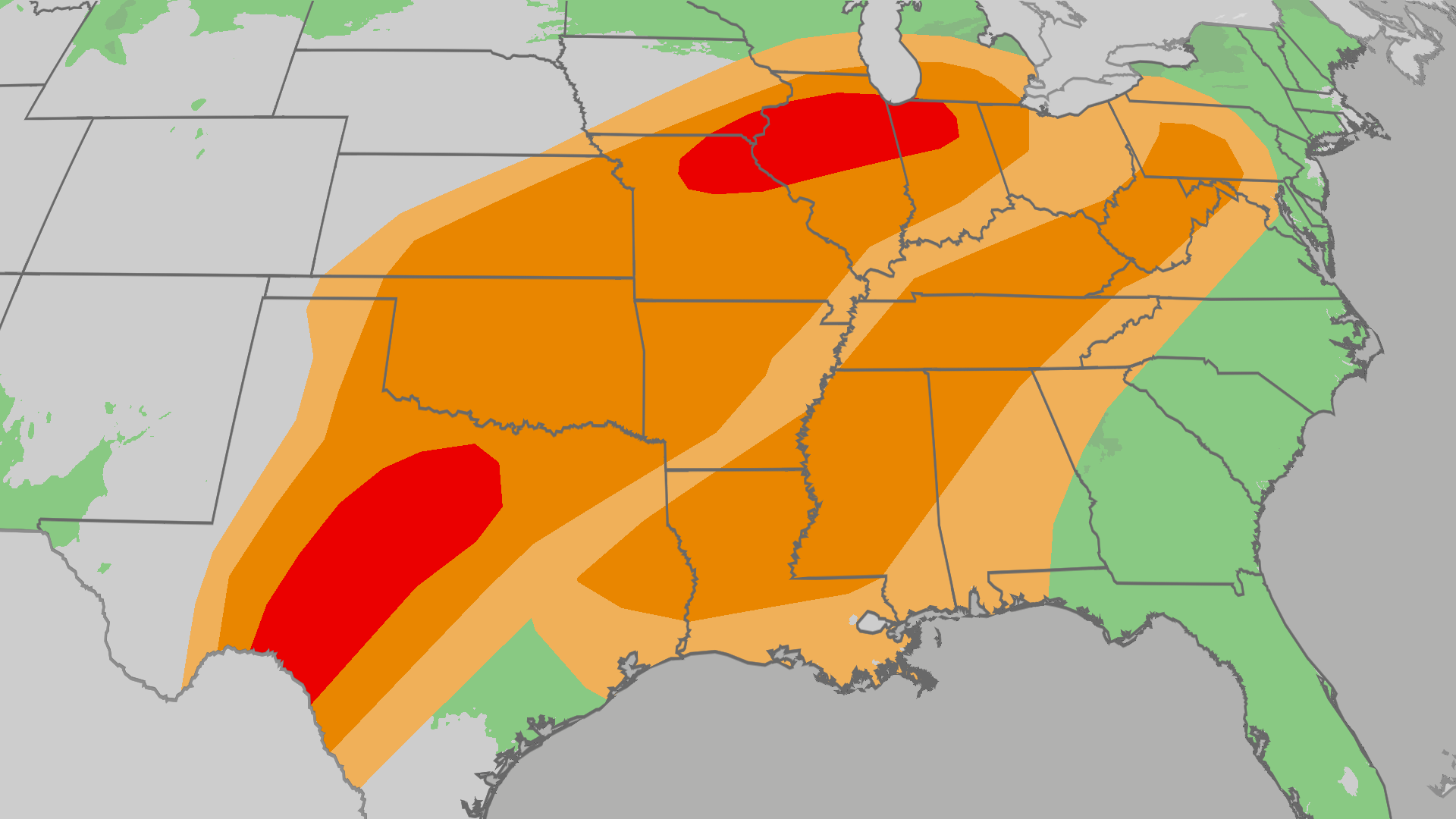

At least 18 tornadoes were confirmed last Thursday–Saturday, including four fatalities, and a new multi-day severe weather outbreak is forecast across the South, Midwest and East beginning Tuesday. The Storm Prediction Center has an enhanced (level 3/5) risk from NW Missouri to N Indiana and central Texas, with hazards including hail >2 inches, wind gusts >74 mph, and EF2+ tornadoes; rainfall of 1–3 inches (higher where storms train) may cause localized flooding. The primary risk window is Tuesday afternoon/evening into Wednesday, with lingering severe storms possible into Thursday near the Southeast coast and Florida.

Expect a cascade of short-window operational shocks (hours–weeks) that markets underprice: localized outages and road/rail slowdowns disproportionately hit just-in-time supply chains — refrigerated freight for food/seed, downstream chemical deliveries for crop protection, and regional fuel distribution. Those disruptions often manifest as sharp but transient P&L swings for processors and midstream logistics; watch weekly freight rates, scratch-off rail car counts, and spot diesel cracks for early signals of tightening.

Insurance and reinsurance are where second-order effects concentrate over months. Loss recognition typically lags events by 1–2 quarters as claims accumulate and adjusters validate damage; that lag creates an earnings window where brokers capture fee tailwinds (renewal activity, higher premiums) before carriers fully price the loss through reserve strengthening or capital raises. Reinsurance capacity tends to reprice at renewal (often double-digit %-points) and can trigger new cat-bond issuance — a visible precursor to margin compression in primary P&C names.

Capital expenditure flows create durable winners: vendors of resilience hardware (backup power, rooftop/roofing services, distribution switchgear, short-duration battery systems) see order books extend 2–12 months, while municipal budgets and small utilities face multi-year fiscal pressure that will re-prioritize maintenance vs new projects. That rotation benefits specialty industrials and systems integrators even if broad utility equities lag.

Tail risks are concentrated and binary: a clustered multi-state catastrophe could force reinsurance aggregate limits, creating liquidity squeezes and fast implied-volatility spikes in insurer equities and cat-bond spreads; conversely rapid improvement (drying, fast repairs, meaningful federal aid) can materially compress the short-term tradeable dislocation. Key catalysts to watch: soil moisture indices, 7–14 day river forecasts, and upcoming Jan/April reinsurance renewal commentary.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.30