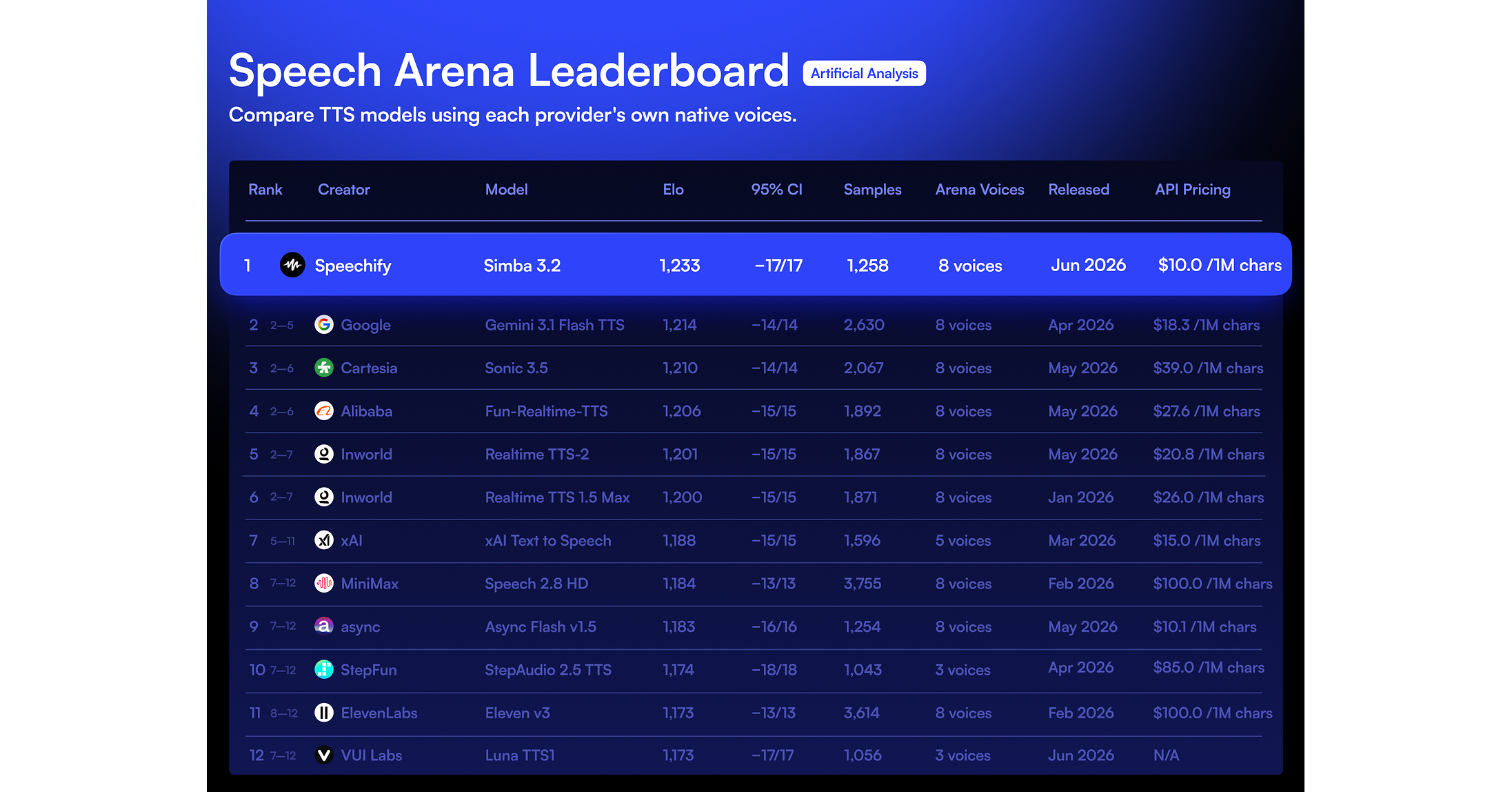

Speechify’s Simba 3.2 streaming TTS model ranks #1 on the Artificial Analysis leaderboard and joint #2 on Voice Arena, with pricing of $10 per 1M characters (dropping to $6 at Scale), making it the least expensive model in the top ten. The benchmarks use blind/independent methodologies and position Simba 3.2 as the top real-time option at its price point. For developers, Speechify also highlights features including lower time-to-first-byte, SSML prosody/emotional control, and instant voice cloning, with availability now via its SpeechifyAI REST API and SDKs.

This is less about a single model win and more about where pricing power migrates in voice AI. If best-in-class real-time TTS is already available at near-commodity rates, the economic moat shifts away from raw model quality and toward distribution, latency guarantees, workflow tooling, and embedded endpoints. That is structurally bearish for standalone voice API vendors whose differentiation was partly benchmark leadership, and it favors platforms that can absorb voice as a feature inside a broader product stack. Near term, the market impact is probably muted for public equities, but the competitive response matters. Over the next 1-3 months, expect more aggressive price compression and marketing spend across the voice stack as peers defend developer mindshare; that can pressure gross-margin assumptions for private benchmarks and reduce the premium investors pay for “SOTA” narratives. Over 6-18 months, the bigger winner is likely downstream application builders in customer support, accessibility, and agentic workflows, where lower inference cost expands usage and raises attach rates. The contrarian point is that benchmark leadership does not equal durable monetization. Real enterprise adoption depends on SLA stability, telephony performance, multilingual consistency, and compliance under load; if those are weaker than the marketing implies, this could be a temporary leaderboard-driven rerating rather than a true share shift. The thesis is falsified if large customers stick with incumbents despite the price gap, or if rival vendors respond with equally good low-latency models and the pricing edge disappears within a quarter. For the named publics, the read-through to AAPL is mildly positive because cheaper, better TTS lowers the cost of richer accessibility and voice UI features without needing Apple to own the frontier model. GOOGL is more of a neutral-to-slight negative on the narrative side: if the market views Google DeepMind as behind in voice quality, it reinforces the idea that Google’s AI advantage is distribution-led rather than model-led. But this is not a high-conviction public-market signal yet; the investable edge is in watching whether voice AI adoption accelerates enough to move endpoint owners and cloud providers, not in chasing benchmark headlines.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.55

Ticker Sentiment