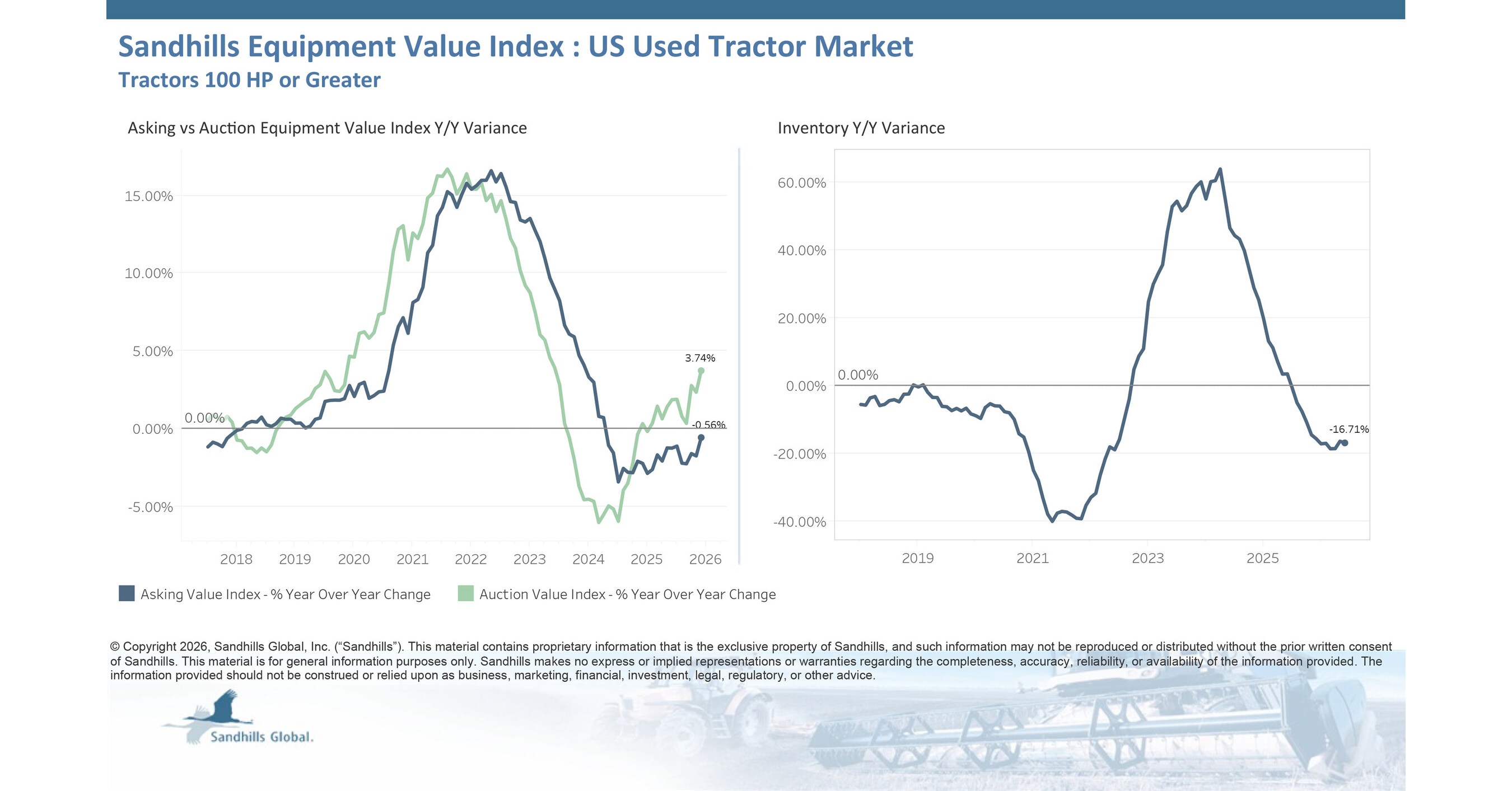

Sandhills’ June used-equipment data show inventories generally declining (e.g., used high-horsepower tractors down 1.26% M/M and 16.71% Y/Y; semi-trailers down 4.03% M/M and 29.28% Y/Y) while prices firm up in key segments (asking values +0.63% M/M for 100+ HP tractors; auction values +0.56% M/M and +3.74% Y/Y). The EVI spread for high-HP tractors rose to 32% (up 1 pp vs May), indicating tighter dealer markups even as prices remain below 2015 peaks. In commercial trucking, a Sandhills manager cited strong freight demand and easing fuel prices, with “aggressively priced units” moving and dealers hopeful prices will soften further.

This reads less like a clean demand boom and more like a market where usable inventory is being worked off faster than replacement supply is arriving. That matters because residual values are the first derivative for dealer economics: firmer resale prices improve trade-in math, reduce floorplan stress, and can pull forward replacement cycles for fleets that were waiting for better bid levels. The best read-through is to residual-value-sensitive names and channels — truck OEMs, auction platforms, and lenders with collateral exposure — not to broad industrials. The second-order loser set is the buyer side: fleets, contractors, and warehouse operators lose negotiating leverage as used supply thins, which can delay purchases if new-equipment pricing does not narrow the gap. That creates a subtle cap on near-term unit growth for OEMs even when values improve; margin support can come before volume recovery. By contrast, categories showing weaker values and rising inventories are a warning that not all capex is rebounding evenly, so construction and material-handling exposure remains more fragile than trucking. Time horizon matters. Over the next 1-3 months, the catalyst is whether freight and fuel keep the truck channel tight enough to sustain auction-price firmness; if not, this becomes a temporary inventory-clearing bounce. Over 6-18 months, the structural question is whether higher used values translate into healthier new-truck order books and lower credit losses, or simply reflect constrained supply. For HPQ, the signal is essentially neutral-to-noise; there is no direct hardware/software read-through large enough to matter absent a broader capex upturn.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.08

Ticker Sentiment