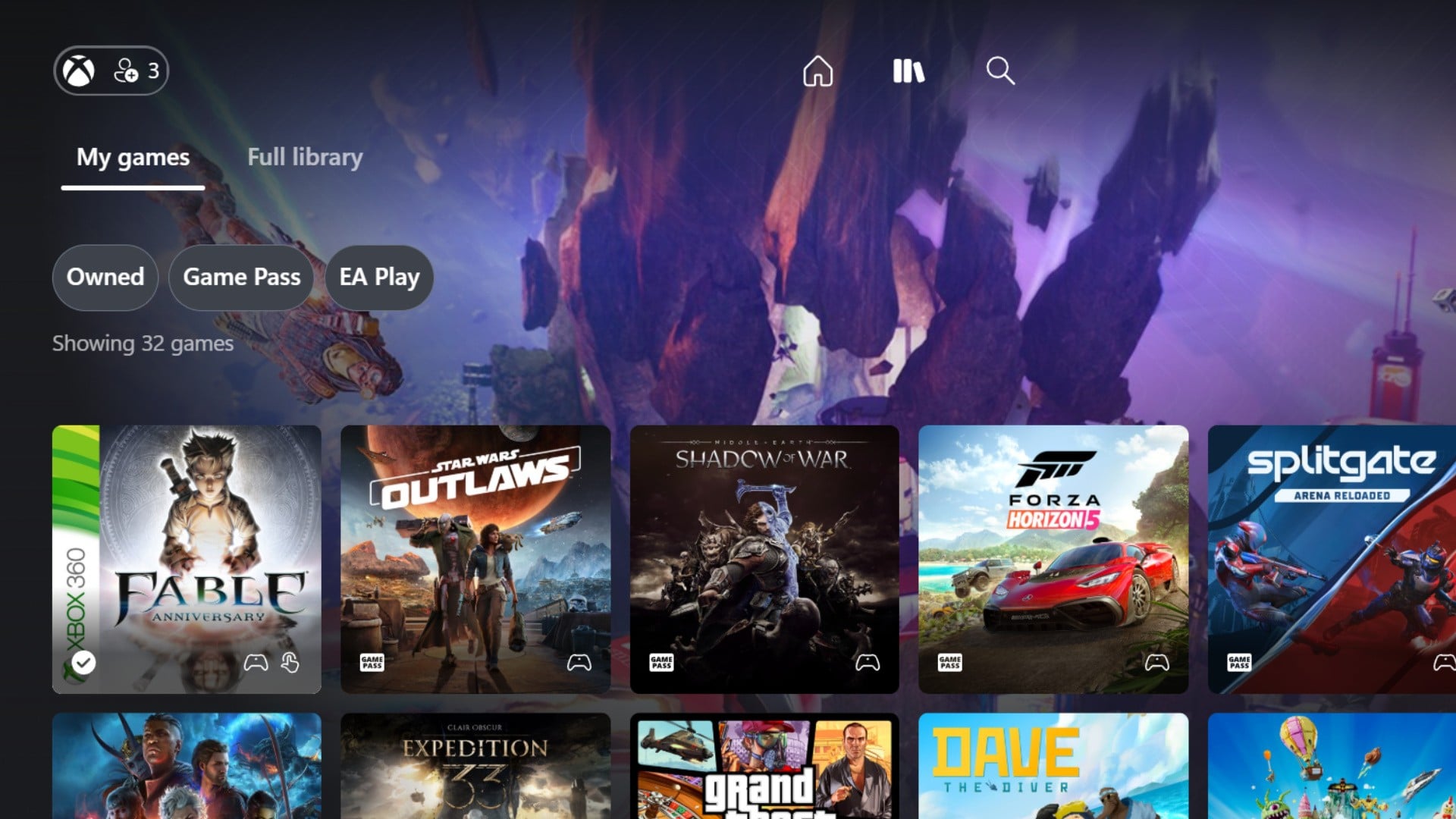

Microsoft has begun a preview rollout of a redesigned Xbox Cloud Gaming web dashboard accessible by opting into Preview Features at xbox.com/play and visiting play.xbox.com. The update refreshes navigation and UI elements and adds a full library for owned games, easing access to "Stream Your Own Game" titles; the preview may lack some functions and will be iterated over time, representing a modest product improvement likely to influence user engagement but with minimal near-term financial impact.

Market-structure: This UX refresh for Xbox Cloud Gaming is a low-cost product improvement that incrementally increases Game Pass stickiness and marginally boosts cloud streaming hours. Winners are Microsoft (MSFT) and Azure (indirectly) via higher usage and monetization; small independent cloud-gaming outfits and legacy console hardware makers see neutral-to-modest downside as marginal consumption shifts to browser streaming. The market impact is measured — expect revenue/engagement lift in the single-digit percent range over 2-8 quarters, not an immediate earnings shock. Risk assessment: Tail risks include operational latency or a high-profile outage that dents trust, and regulatory scrutiny if Microsoft leverages bundling to foreclose rivals (EU/US antitrust within 6–24 months). Immediate risk is execution/UX bugs during preview (days–weeks); meaningful financial risk unfolds over quarters if licensing or streaming costs compress margins. Hidden dependencies: broadband penetration and publisher licensing economics; catalysts include major game releases, Xbox showcase events, and Azure pricing announcements. Trade implications: Tactical long bias to MSFT sized conservatively (1–2% of portfolio) with option structures to cap downside; consider relative longs vs. console/heavy-hardware peers (e.g., long MSFT / short SONY) as a 3–9 month trade to capture cloud-adoption premium. Use 3–6 month call spreads to express upside with capped cost, and avoid large directional exposure until subscriber or Azure usage metrics confirm >3% QoQ improvement. Contrarian angles: Consensus likely understates marginal monetization from improved web discovery but overestimates rapid platform takeover — Stadia/GeForce Now showed UX gains don’t guarantee market share. Mispricings exist in near-term options (IV cheapens around quiet news); unintended consequence: higher streaming hours may raise Azure-capex or licensing, pressuring margins if not offset by ARPU increases.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment