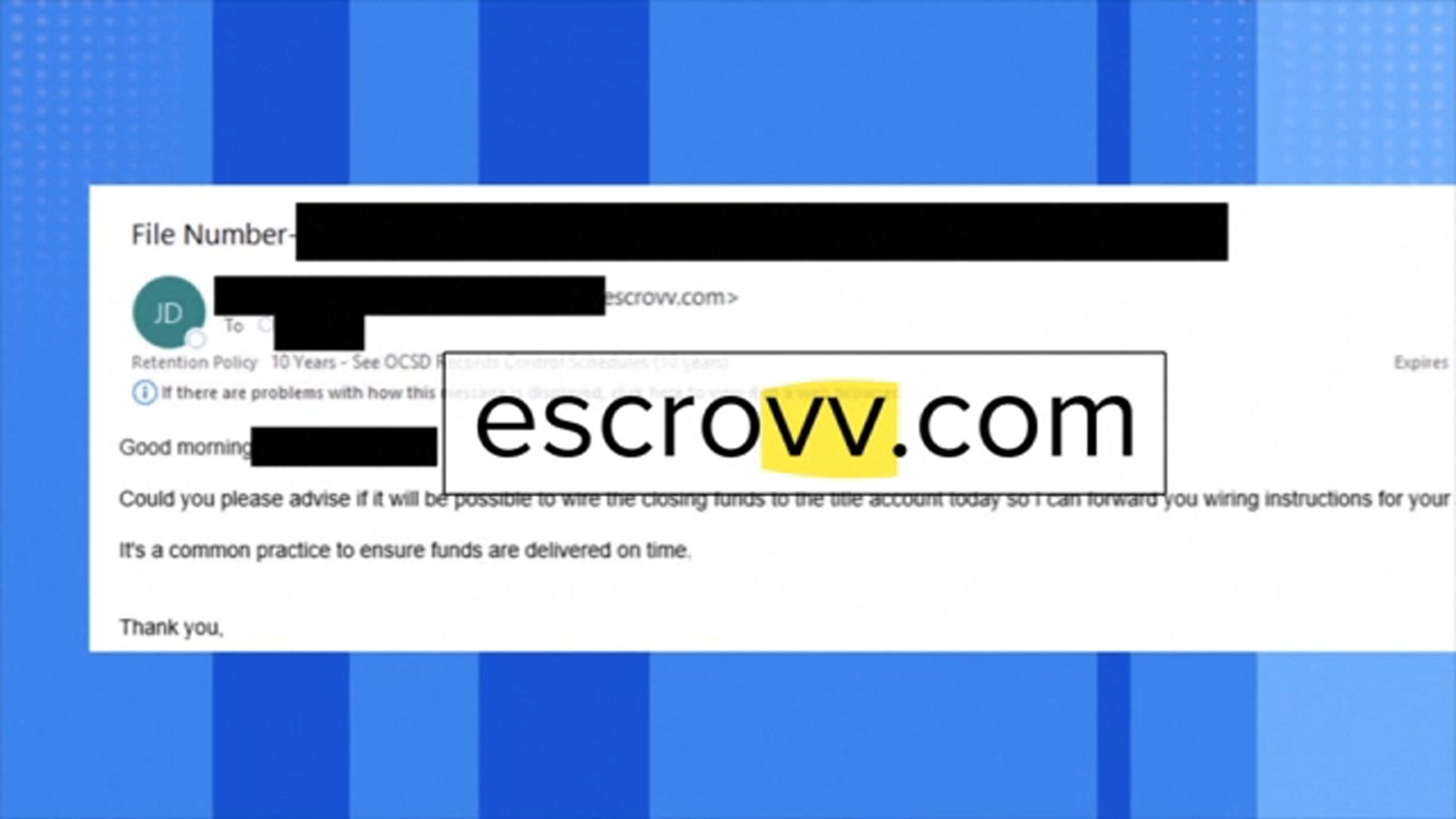

A Southern California couple said they nearly lost hundreds of thousands of dollars in a mortgage-related business email compromise scam, with about 10% of the stolen funds reportedly converted into Bitcoin and gone. Investigators ultimately recovered close to 90% of the money after tracing the transfers, highlighting the importance of rapid reporting and phone verification before wiring funds. The article underscores ongoing cyberfraud risk in home financing rather than any broader market-moving development.

This is not a one-off consumer scare; it reinforces that the weakest link in housing transactions is the final-mile payment instruction, where operational trust is concentrated and controls are often informal. The economic winner is not the criminal ecosystem alone — it is every vendor that can monetize verification, authentication, and escrow workflow hardening: identity verification, secure messaging, callback validation, and insurance products tied to closing-stage fraud. For lenders and title/escrow platforms, the real margin opportunity is bundling these controls into the workflow so they become default rather than optional. The second-order effect is reputational and regulatory pressure on mortgage originators and title agents, especially smaller independents that rely on email-heavy manual processes. A single high-profile BEC event can push brokers and escrow firms toward more expensive payment rails, which increases friction but also lowers fraud rates; over time that shifts share toward larger platforms with integrated security stacks. Cyber-insurance carriers may also reprice this segment because home purchase wires are large, time-sensitive, and often unrecoverable within days, creating a claims profile that is both frequent and severe. The market is likely underestimating how quickly this turns into procurement spend rather than just consumer education. In the near term, the catalyst is headline-driven and episodic; over months, the more durable driver is mandated process change by lenders, title companies, and state regulators after enough losses accumulate. The contrarian view is that the incident does not imply rising fraud incidence so much as rising reporting and better detection, but that still supports vendors with low-friction verification tools because buyers will pay to reduce the tail risk even if actual attack volume is stable.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45