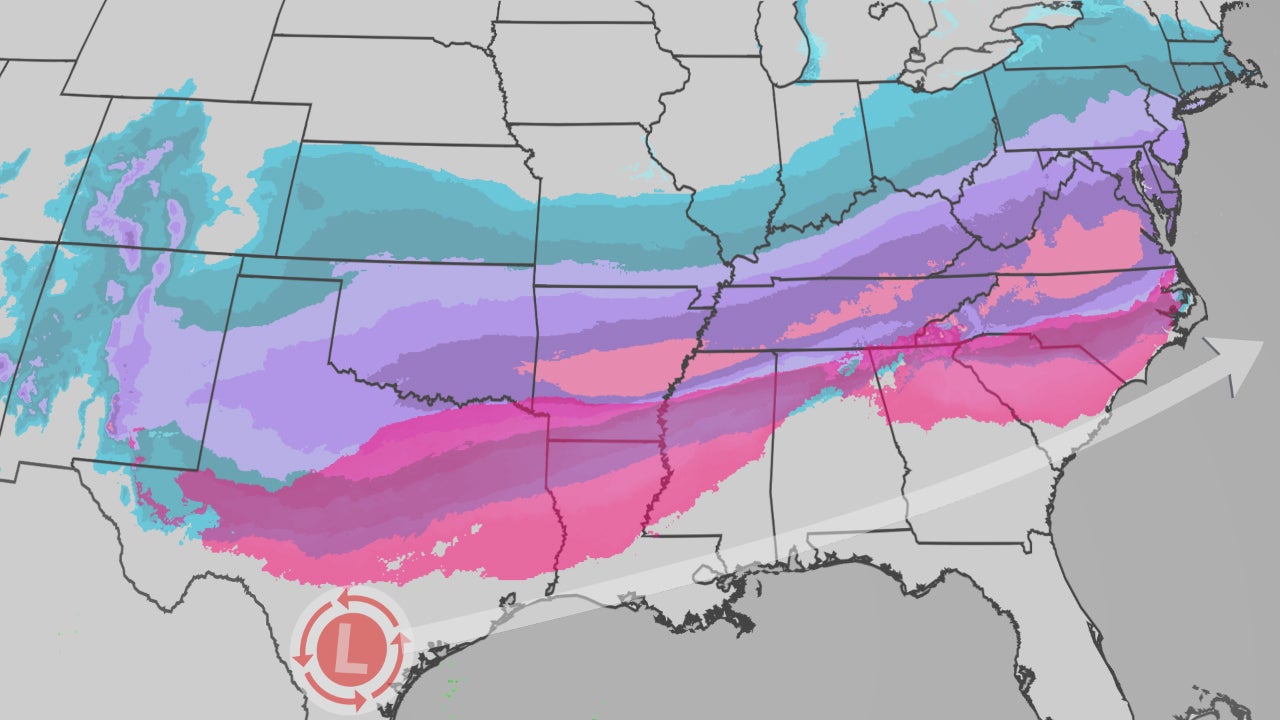

A major winter storm (Winter Storm Fern) is forecast to impact the U.S. Southern Plains and large parts of the East from Friday through the weekend, bringing damaging ice and heavy snow from Texas and Oklahoma into the Carolinas and mid‑Atlantic. Winter storm watches and warnings span dozens of population centers (including Houston, Dallas, Oklahoma City, Nashville, Charlotte, Richmond, Washington D.C., Philadelphia and New York City) with risks of significant ice accumulations, tree damage and multi‑day power outages, as well as hazardous or impassable roads. Investors should monitor potential regional upside in energy demand and volatility in utilities and transportation sectors, and plan for short‑lived supply chain and infrastructure disruptions as forecasts continue to evolve.

Market structure: Near-term winners are natural gas spot sellers and midstream pipeline owners (expect higher throughput +10–25% regional heating demand) and generator/hardware suppliers (Generac GNRC). Losers include regional airlines (DAL, AAL) from cancellations, local retail/distribution/logistics (KR, WMT short-term fulfillment risk), and utilities in the Southeast that may incur repair and vegetation‑management costs, pressuring near-term cash flow and customer satisfaction. Risk assessment: Tail risks include multi-day, widespread outages causing >$500M–$1B in insured losses regionally and multi-week supply-chain disruption (fuel, last‑mile), which would push insurer implied vols and claims. Time horizons: immediate (0–7 days) travel and operational shocks; short (2–8 weeks) commodity/allocation and repair-cost repricing; long (quarters) potential regulatory scrutiny and capex for grid resilience. Hidden dependencies: localized natural gas infrastructure constraints and generator supply shortages can amplify price moves. Trade implications: Expect a jump in NG and electricity forwards and a flight‑to‑quality into Treasuries; options vols for airlines and insurers will spike. Direct plays: short-dated NG exposure (ONG/UNG options) and GNRC equity/call exposure; short short-term airline equity/puts. Use pair trades to capture relative moves (long midstream KMI vs short airlines). Contrarian angles: Consensus may overstate permanent utility credit damage—regulated utilities (NEE, D) often recover costs via rates; a sell-off could present buying windows. Historical parallels (Feb 2021 cold snap) show ~20–30% NG spikes then mean reversion in 2–6 weeks; therefore scale out at +15–25%. Watch outage counts and regional gas flow data as early triggers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.25