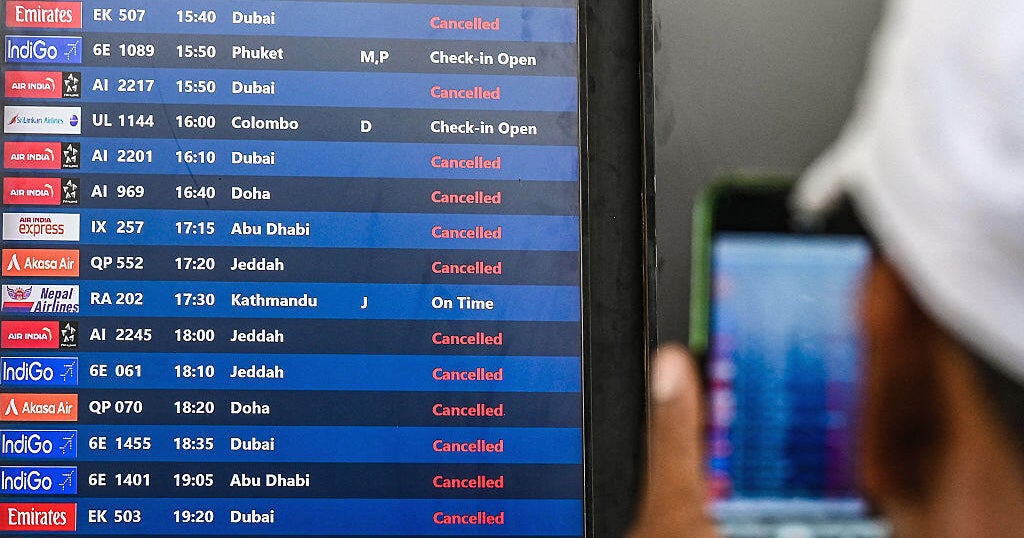

U.S.-Israeli strikes and Iran's retaliatory actions have led to widespread airspace closures across the Middle East, forcing cancellation of more than 2,400 flights and shutting key hubs including Dubai, Abu Dhabi, Doha and Manama. Major carriers have suspended routes (Emirates paused Dubai operations; United canceled U.S.–Tel Aviv flights through March 6 and Dubai flights through March 4) while Cirium estimates the regional hubs normally handle roughly 90,000 passengers per day; rerouting over Saudi airspace will add flight hours and fuel costs, pressuring airline margins and potentially pushing fares higher if the disruption persists. Airlines are issuing waivers and preparing recovery efforts, but the near-term operational and cost impacts create a risk-off environment for travel and regional exposure.

Market structure: Immediate winners are energy producers (higher crude/jet fuel prices), defense primes and airport hubs outside the closed airspace; immediate losers are long‑haul carriers routing through ME (UAL, Emirates, Qatar Airways) facing canceled flights, longer block hours and mid-single‑digit percentage increases in unit fuel burn. Competitive dynamics favor carriers with domestic networks or alternative hubs (LUV, many US majors) and freight operators; pricing power for remaining long‑haul seats should allow fare lifts of 10–25% on affected lanes if closures persist >1 week. Cross‑asset: expect knee‑jerk rallies in Brent/ULSD, safe‑haven bids in gold and USD, higher implied vols and skew in airline equity options, and modest rally in US Treasuries (flight-to-safety) for 48–72 hours.

Risk assessment: Tail risks—protracted multi‑week closure or escalation that hits shipping lanes or Gulf oil infrastructure—could push Brent +15–30% and drive sustained airline margin erosion; regulatory/insurance shocks (airspace bans, insurers denying war exclusions) are low‑prob but high‑impact. Time horizons: immediate (days) = operational chaos and vols spike; short (weeks) = revenue loss and repricing in airline equities; long (quarters) = possible demand erosion (1–3%) and tectonic rerouting cost normalization. Hidden dependencies include airline fuel hedges, reinsurance clauses and sovereign airspace coordination; catalysts: public intel sharing, US/Iran de‑escalation or further strikes.

Trade implications: Direct trade: short troubled long‑haul airlines (UAL) and airline ETF exposure (JETS) with 30–90 day options, long defense primes (LMT, RTX) and energy (XOM, XLE) in equities or ETFs. Pair trades: long domestic carrier LUV vs short UAL to capture relative resilience. Options: buy 30–60 day put spreads on UAL or JETS to cap cost; buy calls on XOM/XLE or Brent futures if Brent moves +10% intraday. Entry: act within 48–72 hours for tactical shorts; add to energy/defense if closures exceed 7 days; exit when cancellations fall to <10% of baseline or after 4–6 weeks.

Contrarian angles: Consensus may overprice structural damage—histor precedents (2019 Gulf flare‑ups) showed 2–6 week price dislocations that reversed; oil services and reinsurers may be oversold if physical infrastructure is intact. Mispricings: well‑capitalized carriers with little ME hub exposure (LUV, DAL domestic) are likely underowned; consider buying credit or short‑dated calls on these names against short UAL exposure. Unintended consequence: fare hikes could accelerate substitution to virtual meetings and permanently shave international leisure/business travel volume by ~1–3% over 12–18 months, so reassess long‑duration travel sector exposure by Q3.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40

Ticker Sentiment