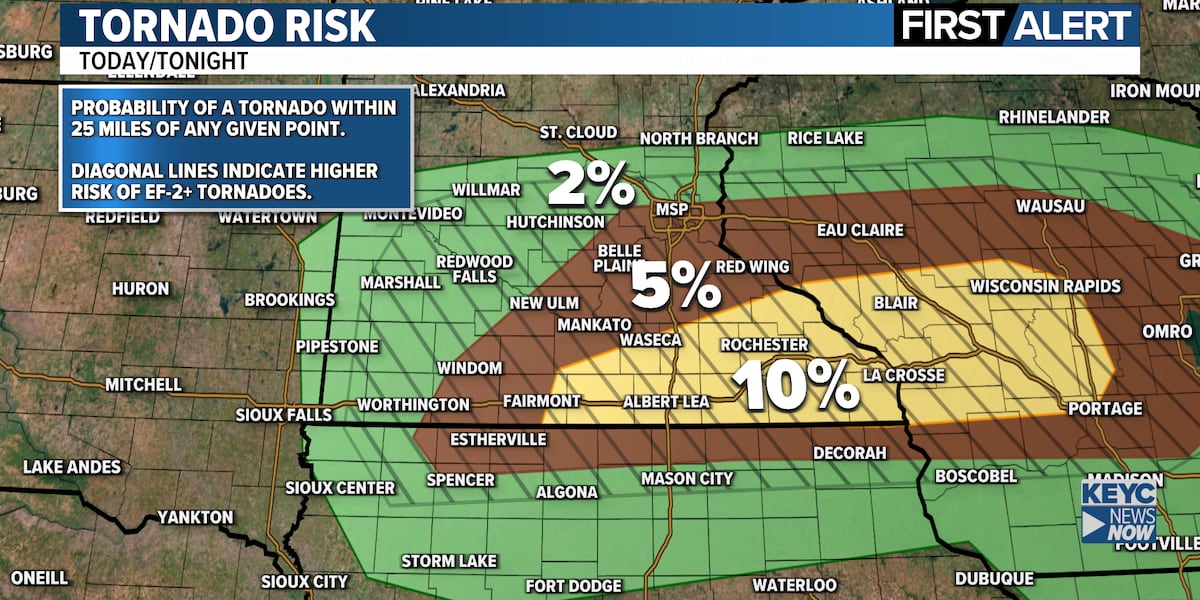

A high-risk severe weather day is expected today, with thunderstorms developing after 3pm and the greatest threat south of a Redwood Falls-to-Twin Cities-to-western Wisconsin line. The main hazards are tornadoes, very large hail potentially reaching tennis-ball size or larger, with damaging wind gusts and heavy rain becoming more likely later this evening. The article is informational and localized, with limited direct market impact.

The immediate market read is not about headline storm risk itself, but about operational fragility in the next 12-36 hours: local outage-prone utilities, retail traffic, and last-mile logistics all face a short, sharp hit if the storm track holds. The bigger second-order effect is in insurance: hail-heavy events drive disproportionate near-term loss ratios because claims are high-frequency, property-dense, and often exceed model assumptions when storm cells train over the same corridor. That typically matters first for regional P&C names and reinsurers with exposure to Midwest cat layers, while broader market impact tends to be muted unless the event escalates into a multi-state outbreak. A less obvious beneficiary set is catastrophe restoration and equipment rental, where revenue can re-rate within days as demand for emergency tree removal, roofing, drying, and temporary power spikes. If the event produces widespread hail rather than tornado damage, the economic footprint can actually be more persistent: auto-body repair backlogs, OEM parts inflation, and rental-car utilization all rise for weeks, creating a small but tradable squeeze in service capacity. Conversely, if winds dominate and hail underwhelms, the insurance loss severity thesis softens quickly and the trade should be unwound fast. The key contrarian point is that severe-weather headlines often overstate GDP impact but understate earnings dispersion. For investors, the edge is not in shorting the whole market; it is in exploiting who has deductible-heavy, reinsurance-sensitive exposure versus who earns incremental revenue from cleanup and claims processing. Timing matters: the best setup is immediately after confirmation of the damage footprint, when sell-side models lag claim severity by several days. Catalyst horizon is very short-term for utilities, insurers, and retailers, but can extend 1-3 quarters for property claims, auto repairs, and replacement demand. If storms cluster east of the warm front or hail swath is narrower than expected, the risk/reward flips quickly against bear positioning in insurers. The highest convexity remains in options around the local severity window rather than outright equity shorts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.10