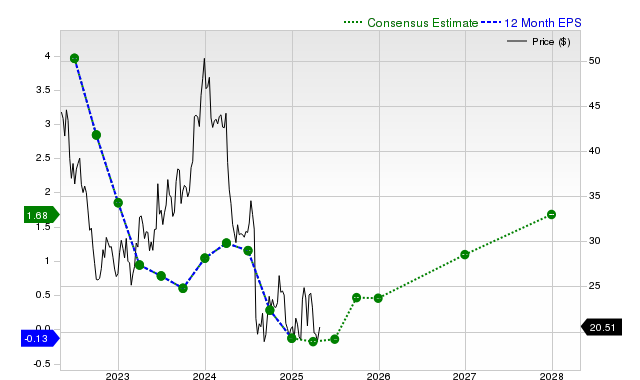

Intel (INTC) shares have significantly outperformed, returning +20.5% over the past month, well above the S&P 500's +3.1%. While analysts project substantial year-over-year EPS growth for the current (+215.4%) and next (+357.9%) fiscal years, with estimates remaining unchanged over the last 30 days, consensus revenue forecasts indicate slight near-term declines before a modest rebound. Despite consistently topping revenue estimates in recent quarters, Intel carries a Zacks Rank #3 (Hold), implying expected in-line market performance, and a 'D' Zacks Value Style Score, suggesting it trades at a premium to its peers.

Intel's recent stock performance, a gain of 20.5% over the past month, has significantly outpaced both the S&P 500 composite (+3.1%) and its own semiconductor industry group (+0.2%). This strong momentum, however, contrasts with a more mixed fundamental outlook. While consensus earnings estimates project substantial year-over-year growth for the current fiscal year (+215.4%) and the next (+357.9%), these forecasts have remained unchanged over the last 30 days, suggesting the recent rally is not driven by upward analyst revisions. Furthermore, the top-line forecast is weak, with consensus sales estimates indicating a year-over-year decline of 1.3% for the current quarter and 1.7% for the current fiscal year, before a modest 3.8% recovery next year. This implies that projected earnings growth is predicated on margin improvement rather than revenue expansion. The stock's valuation is also a point of concern, as its Zacks Value Style Score of 'D' indicates it is trading at a premium to its peers. The neutral Zacks Rank of #3 (Hold) reinforces this cautious view, suggesting the stock is likely to perform in line with the broader market in the near term, despite the recent surge in price.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment