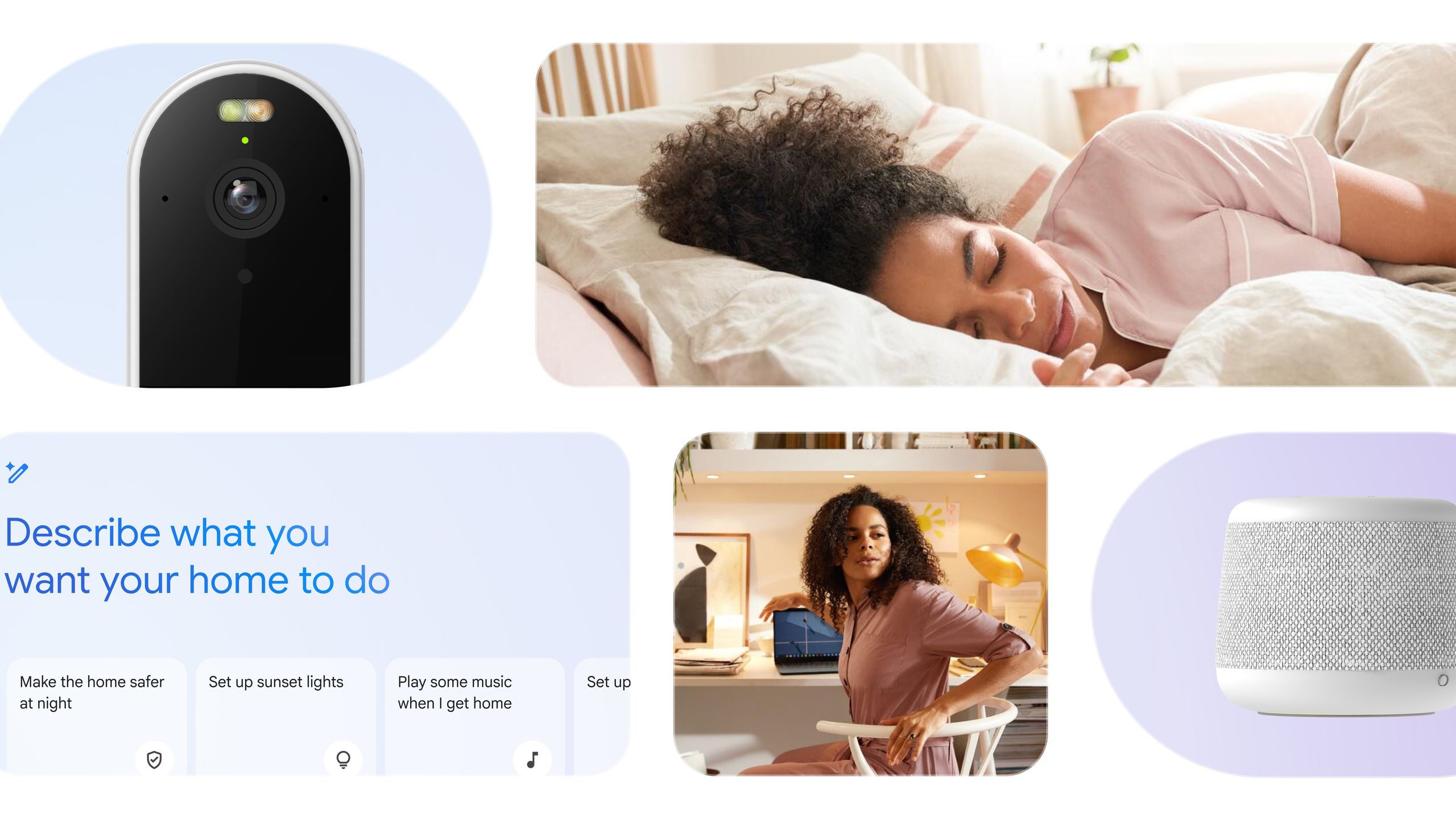

Google is expanding Gemini for Home into a full-stack AI offering, opening access to third-party hardware makers, service providers, carriers, ISPs, and security companies. The new Gemini built-in program will let partners launch Gemini-capable smart cameras now and smart speakers in 2026, while Home Premium is being integrated with firms like AT&T. The update is strategically positive for Google’s smart home ecosystem, but near-term market impact is likely limited.

Google is doing something more important than a feature launch: it is turning smart-home AI into a distribution layer that third parties can bundle, resell, and normalize. That shifts the value proposition from one-off consumer hardware sales toward recurring subscription economics, which is structurally better for Google because it increases platform stickiness and lowers customer acquisition costs through partners like carriers and security installers. The first-order winner is clearly GOOGL, but the second-order winner may be the ecosystem of peripherals that become “good enough” once Gemini is the intelligence layer, which compresses differentiation for standalone smart-speaker and camera vendors. The competitive pressure is asymmetric. Amazon and Apple have consumer-installed bases, but Google’s move is more monetization-friendly because it can be embedded into carrier billing, ISP bundles, and security-service contracts, which are much harder to churn than app subscriptions. That means the real risk to competitors is not feature parity in 2026, but loss of the most durable customer cohorts: households that already pay for broadband/security and are easiest to upsell into AI monitoring. For telecom partners, this is margin-accretive if it reduces churn by even low single digits, but it also creates a dependency on Google’s roadmap and support economics. The contrarian angle is that the market may overestimate near-term revenue and underestimate deployment friction. Smart-home AI still faces install-base fragmentation, privacy scrutiny, and low consumer willingness to pay for incremental AI features unless bundled into a broader utility bill or security plan. The monetization curve is likely back-end loaded: modest contribution in the next 2-4 quarters, larger impact over 12-24 months if partner integrations actually convert households at scale. The key tail risk is that the product remains a nice demo but fails to become a habit, in which case partner enthusiasm fades and the subscription uplift disappoints.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment