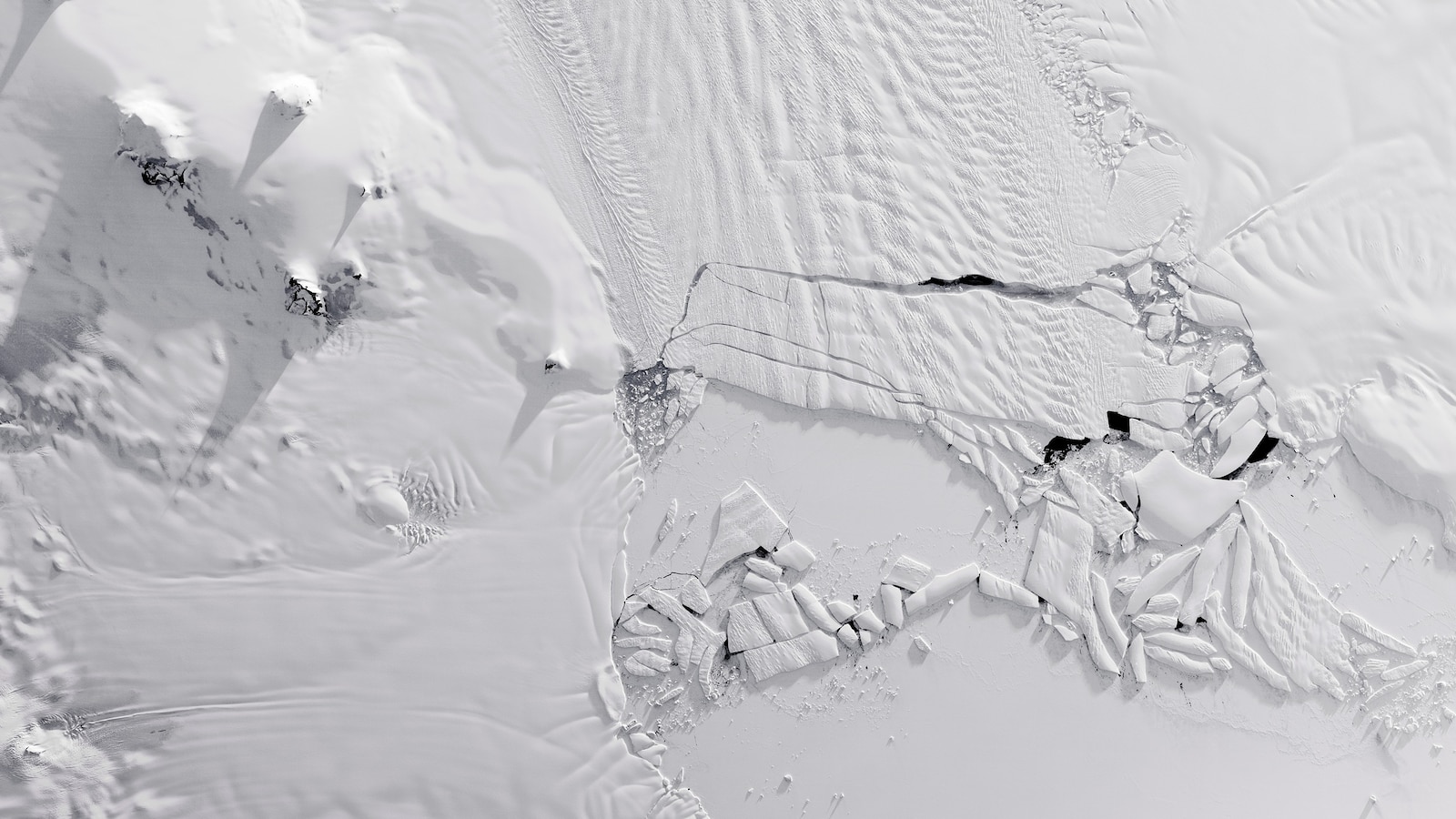

A 30-year satellite study mapped Antarctica’s grounding line and found nearly 5,000 square miles of grounded ice lost since 1996, with vulnerable regions retreating at more than 170 square miles per year and some glaciers (Smith 26 miles, Pine Island >20 miles, Thwaites >16 miles) withdrawing up to 25 miles. While 77% of the coastline shows no grounding-line migration, accelerated melting in West Antarctica, the Antarctic Peninsula and parts of East Antarctica—driven largely by warm ocean intrusions in the west—raises long-term sea-level risk (Thwaites already accounts for ~4% of observed rise; full West Antarctic collapse could add ~9 feet). The findings increase downside tail risk for coastal assets and infrastructure and underscore potential long-horizon liabilities for climate-sensitive portfolios.

Market structure: Rapid Antarctic grounding-line retreat raises structural winners (engineering & infrastructure contractors, water-tech and desalination firms, specialty construction materials, and ports/dredging contractors) and losers (coastal municipal issuers, coastal residential REITs/homebuilders, and primary insurers with concentrated coastal PML). Expect pricing power for specialized engineers (port retrofits, flood defenses) and higher loss-cost assumptions for property & casualty underwriters; reinsurance capacity may tighten, lifting premium rates over 12–36 months.

Risk assessment: Tail risks include accelerated regulatory repricing (FEMA flood-map revisions, stricter building codes) and a hard insurance repricing cycle that could cause localized mortgage-market dislocations and muni-credit stress; these are low-probability in 0–2 years but medium-probability over 2–10 years. Hidden dependencies: mortgage-backed securities (high coastal concentration), municipal pension funds, and bank CRE portfolios are second-order exposures that could amplify stress if insurers retrench or premiums spike.

Trade implications: Near-term (days–months) trade volatility favors protective puts on reinsurers/insurers and shorts in coastal homebuilders; medium-term (6–36 months) favors long positions in Jacobs (J), AECOM (ACM) and Xylem (XYL) for adaptation capex. Cross-asset: expect wider spreads on lower-rated coastal munis, higher cat-bond yields, modestly higher Treasury term premia as governments finance adaptation.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40

Contrarian angles: The market underprices adaptation beneficiaries — engineering/water-tech can see 20–30% revenue uplifts in stressed coastal metros over 3 years as FEMA/municipal capital plans accelerate. Conversely, large diversified reinsurers (BRK.B) may be over-penalized short-term given capital buffers; mispricings will cluster around zip-code-level property risk rather than national indices.