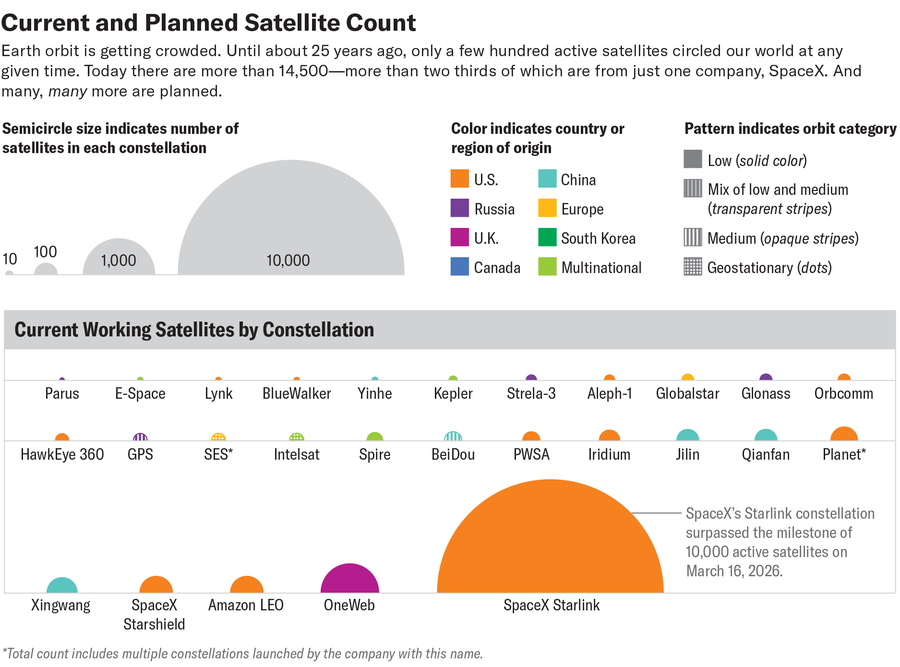

SpaceX reached a milestone of 10,021 active Starlink satellites after a March 16 Falcon 9 launch (11,527 launched since May 2019, with replacements accounting for the gap), representing roughly two-thirds of satellites currently in orbit and serving ~10 million users. The fleet is deployed at ~480–550 km, with Falcon 9 (600+ launches) able to loft up to 60 satellites per mission, while SpaceX reported ~300,000 collision-avoidance maneuvers in 2025 (~40 per satellite); there have been safety incidents (a surviving debris piece in July 2024, a December 2025 explosion and a China near-miss). Competitors and national programs (Amazon Kuiper ~200 launched of >7,500 planned; China planning 13k–15k satellites) plus proposals for hundreds of thousands to 1.7 million total satellites raise regulatory, debris, climate, and astronomy-impact risks that create uncertainty for orbit sustainability and potential future policy action.

The market is mispricing the structural bifurcation between vertically integrated LEO incumbents and the rest of the ecosystem. A dominant operator with captive launch and manufacturing squeezes margins for third-party launch providers, antenna makers and insurers, but it also creates a large, addressable aftermarket for ground terminals, spectrum services and space‑situational‑awareness (SSA) data. Expect winners to be suppliers that can be rapidly integrated into multiple constellations (modular RF front ends, optical inter‑satellite link components, SSA analytics) and losers to be single‑customer contractors or those reliant on premium per‑launch pricing.

Tail risks are concentrated and idiosyncratic: a major fragmentation/collision event, or a politically driven ban on cross‑border user services, would rapidly reprice launch schedules, insurance costs and project economics across years not quarters. Nearer term (weeks–months) watch regulatory filings, high‑visibility debris incidents and insurance rate announcements; medium term (12–36 months) watch spectrum allocations and national security procurement that subsidizes competing constellations. A regulatory pivot toward stricter orbital carrying‑capacity limits would be the single fastest catalyst to compress valuations of launch‑heavy and mass‑production players.

Consensus leans toward “orbit is doomed,” but that underestimates adaptive commercial responses: active debris removal, prioritized orbital lanes, and differential pricing for low‑risk trajectories can expand practical capacity. That implies a multi‑year reallocation of capex from terrestrial fiber expansion into hybrid ground/LEO infrastructure and national security backup systems — an investment theme that is already visible in procurement pipelines but underrepresented in public markets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment